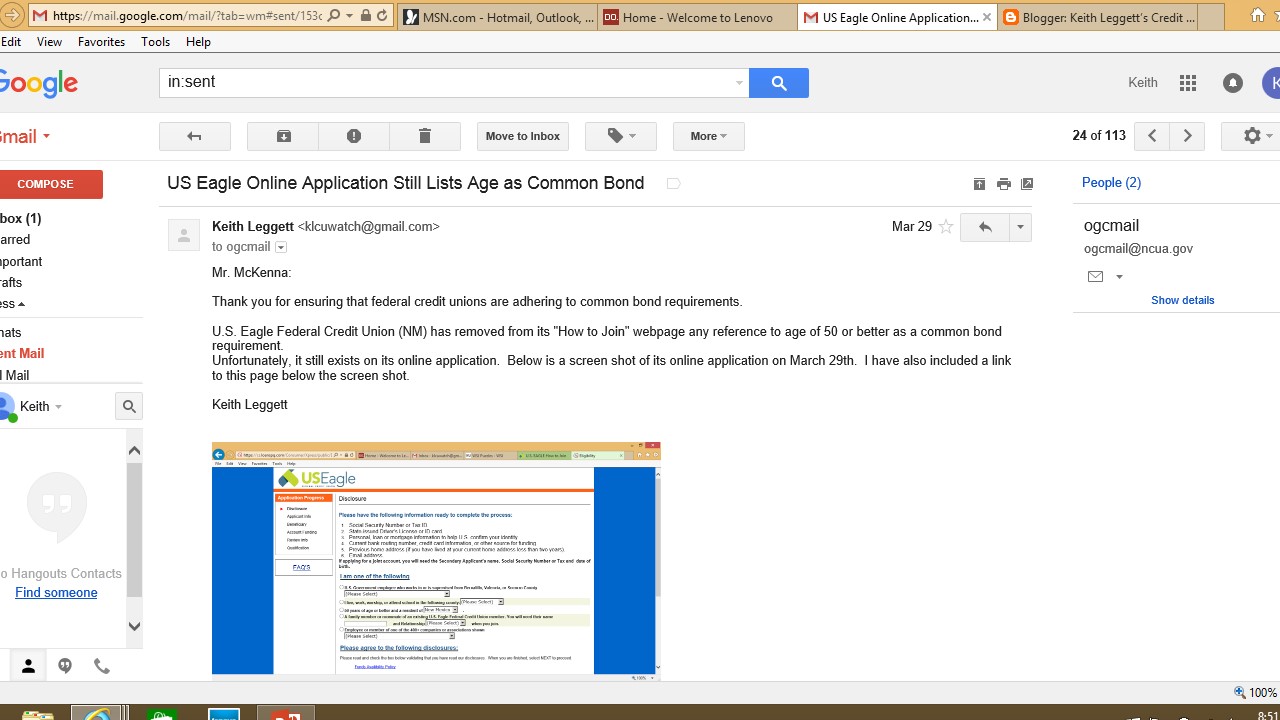

I can report that as of this morning the credit union has removed this impermissible common bond.

Below is a screen shot of this page.

Recently, market disruption has occurred in the taxi industry due to new competition. This competition has negatively impacted the taxi industry, its revenues and has caused the value of taxi medallions to depreciate over the past year. Further or prolonged market disruption in the taxi industry may increase our delinquencies and non-accrual loans collateralized by taxi medallions. It is at least reasonably possible that our losses on these loans could increase in the near term due to further or prolonged market disruption impacting the value of taxi medallions.

"In my travels during my two terms on the NCUA Board, I have seen businesses operating successfully in mixed-use buildings, where street-level space is used for retail operations and an upper floor is used for commercial rentals or private residences. These types of mixed-use zoning are especially popular in urban areas."

Part 741.208 applies NCUA’s restrictive charter conversion and termination of share insurance rules to FISCU. NASCUS concedes that the Federal Credit Union Act gives NCUA authority for rulemaking with respect to credit union to non-credit union charter conversions. However, Congress’s grant of authority in this arena was intended as limiting. NCUA should show deference to state laws addressing conversions or mergers into non-credit unions. With respect to FISCUs, NCUA is only the share insurer, not the chartering authority. NCUA’s only concern in the conversion of a FISCU to non-credit union or non-NCUSIF [National Credit Union Share Insurance Fund] charter is preventing regulatory arbitrage, or any safety and soundness risk posed by reputational concerns. However, in the case of conversion to bank charter, the entity would remain federally insured, mitigating reputational risk. Vindication of the members’ rights and other governance issues are properly left to the chartering regulator – in these cases, the states.I totally agree with Brian Knight that Congress intended to limit NCUA's authority dealing with charter conversions. The Credit Union Membership Access Act of 1998 instructed NCUA to pass regulations that are no stricter than similar regulations promulgated by the other federal banking agencies.

Linda Armyn, Bethpage senior vice president of corporate affairs, said the merger gives others around the nation access to the credit union, ending any geographic limits.

“Our territory has expanded beyond Long Island and we now have a branch in New York City,” Armyn said. “Our charter is not limited by geography at this time.”

While she said Bethpage can now serve people around the nation, the credit union at least in the short-term doesn’t plan to seek to expand across the country.

The content is provided for educational purposes only, with the understanding that neither the authors, contributors, nor the publishers of this site are engaged in rendering legal, accounting or other expert or professional services. If legal or other expert assistance is required, the services of a competent professional should be sought.

Comments appearing in response to articles appearing on this site do not necessarily reflect the views of the ABA. ABA makes no representations regarding the truth or accuracy of commentary or opinions that may be posted in response to the articles that appear on this website.

The inclusion herein of any link to a website, either in the text of an article or in a comment, does not denote any approval, sponsorship, or endorsement by the ABA, and ABA is not responsible for the content or opinions expressed on those linked websites or related commentary. This content is not licensed to third parties sites and is not affiliated with any third party site. Any reference to the author or this content on any third party site on the Internet is not authorized by the ABA.

It is the policy of the American Bankers Association to comply fully with all antitrust laws. Certain discussions should be considered off-limits, including those that contain competitively sensitive data such as price and cost information, or statements that could be construed as reflecting an attempt or desire to control or influence a particular market or markets. Future pricing or other prospective competitive information should never be shared.