The National Credit Union Administration today liquidated First Hawaiian Homes Federal Credit Union of Hoolehua, Hawaii.

Molokai Community Federal Credit Union of Kaunakakai, Hawaii, immediately assumed First Hawaiian Homes’ assets, member shares and most loans.

NCUA made the decision to liquidate First Hawaiian Homes Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operations.

According to the credit union's third quarter call report (most recent available), the credit union was well-capitalized, reported no problem loans, and was making a small profit.

At the time of liquidation and subsequent assumption by Molokai Community, First Hawaiian Homes served 1,379 members and had assets of nearly $3.2 million, according to the credit union’s most recent Call Report.

First Hawaiian Homes Federal Credit Union is the eleventh federally insured credit union liquidation in 2015.

Read the press release.

Wednesday, December 30, 2015

Large Georgia CU to Defect from Federal Charter

Warner Robins-based Robins Federal Credit Union will change to a state charter on New Year's Day, becoming Robins Financial Credit Union.

The credit union cited that the state charter would give it greater flexibility to expand.

Robins has almost $2.1 billion in assets.

Read the story.

The credit union cited that the state charter would give it greater flexibility to expand.

Robins has almost $2.1 billion in assets.

Read the story.

Tuesday, December 29, 2015

$2 Million Gift Gives USU Credit Union Prime Advertising Space at Utah State University's Stadium

The USU Credit Union, a division of Goldenwest Credit Union, received prime advertising space at Utah State University's stadium for donation.

The credit union has committed $2 million to the football stadium renovation.

As part of the agreement, the south and west concourses of the stadium will carry the USU Credit Union name.

Read more.

The credit union has committed $2 million to the football stadium renovation.

As part of the agreement, the south and west concourses of the stadium will carry the USU Credit Union name.

Read more.

Wednesday, December 23, 2015

Paying CU Directors -- More Acceptable; But Controversial

While credit unions paying their directors is becoming more acceptable, the controversy of paying credit union directors persists, according to a December 23 story in The American Banker.

While federal credit unions cannot pay their directors, state chartered credit unions in a dozen states have the authority to pay their directors and that number should grow over time.

Ben Rogers, research director at Filene Research Institute in Madison, Wisconsin and author of the study on compensating credit union directors, told the American Banker: "I think if we had done the study 10 years ago people would have said compensating directors was absolutely against the ethos of credit unions, but today it is much more acceptable."

According to research by the Filene Research Institute (Filene), 145 credit unions in 12 states pay their board members with directors earning between $60 and $37,597 per year. The study said that in 2012 large credit unions paid four times more than smaller credit unions.

Click on this link to view average director pay by state.

The Filene study pointed out that there is a growing evidence of credit unions using compensation to attract and retain qualified board members given the heighten demands on credit union directors.

However, the article noted that paying directors may have policy implications with regard to the credit union industry's preferential tax treatment, as paying directors further erode the distinction between banks and credit unions.

Read the story (subscription required).

While federal credit unions cannot pay their directors, state chartered credit unions in a dozen states have the authority to pay their directors and that number should grow over time.

Ben Rogers, research director at Filene Research Institute in Madison, Wisconsin and author of the study on compensating credit union directors, told the American Banker: "I think if we had done the study 10 years ago people would have said compensating directors was absolutely against the ethos of credit unions, but today it is much more acceptable."

According to research by the Filene Research Institute (Filene), 145 credit unions in 12 states pay their board members with directors earning between $60 and $37,597 per year. The study said that in 2012 large credit unions paid four times more than smaller credit unions.

Click on this link to view average director pay by state.

The Filene study pointed out that there is a growing evidence of credit unions using compensation to attract and retain qualified board members given the heighten demands on credit union directors.

However, the article noted that paying directors may have policy implications with regard to the credit union industry's preferential tax treatment, as paying directors further erode the distinction between banks and credit unions.

Read the story (subscription required).

Tuesday, December 22, 2015

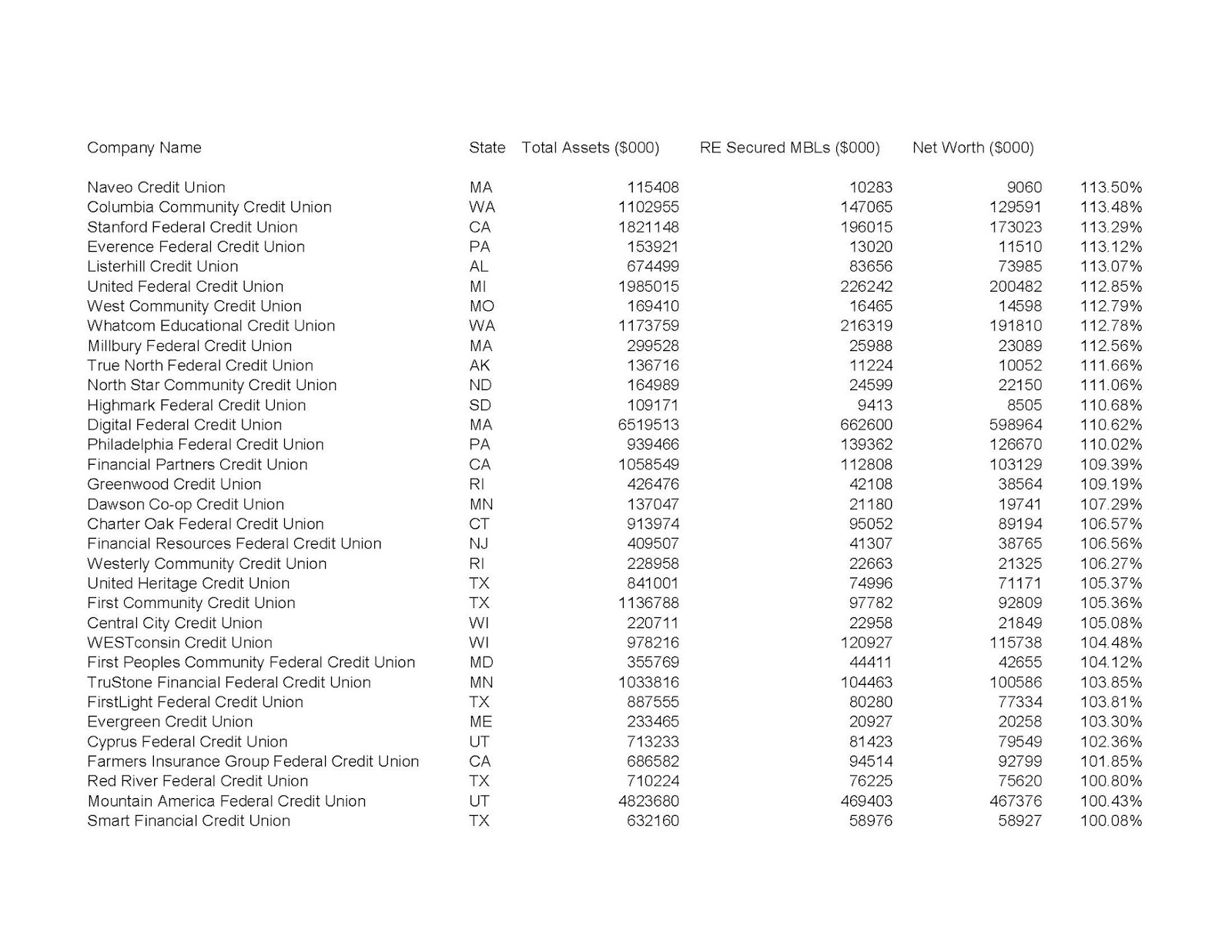

Large CUs' Real Estate Secured Business Loan Exposures

On December 18, the federal banking agencies -- the Federal Deposit Insurance Corporation, the Federal Reserve, and the Office of the Comptroller of the Currency -- issued a statement warning about eased commercial real estate (CRE) loan underwriting and CRE risk management practices that cause “concern.” The federal banking regulators added that supervisors will “continue to pay special attention” to CRE lending in exams in 2016 and reiterated existing interagency guidance on CRE concentration risk.

The National Credit Union Administration did not sign on to this statement; but NCUA may want to sign on to the interagency guidance on CRE concentration risk as real estate secured business loans continue to expand.

There are 105 credit unions with assets of at least $100 million that have an aggregate exposure to real estate secured business loans that exceeds their net worth at the end of the third quarter.

[Editorial note: I know the 105 credit unions include credit unions that have exposure to farmland loans; but the recent weakness in farm commodity prices will likely have a negative impact on farmland values. So, those credit unions making farmland loans also warrant careful monitoring.]

Thirteen credit unions have a real estate secured business loan to net worth ratio above 200 percent and 5 credit unions -- all state charters -- have a real estate secured business loan to net worth ratio in excess of 300 percent.

The two credit unions with the greatest net worth exposure to real estate secured business loans are involved in church financing. Evangelical Christian Credit Union (Brea, CA) has the greatest percentage of its net worth exposed to real estate secured business loans at 907.24 percent. America's Christian Credit Union (Glendora, CA) has the next largest exposure at 532.4 percent.

The following tables provides info on credit unions with real estate secured business loan exposures of at least 100 percent of net worth.

Read the statement.

The National Credit Union Administration did not sign on to this statement; but NCUA may want to sign on to the interagency guidance on CRE concentration risk as real estate secured business loans continue to expand.

There are 105 credit unions with assets of at least $100 million that have an aggregate exposure to real estate secured business loans that exceeds their net worth at the end of the third quarter.

[Editorial note: I know the 105 credit unions include credit unions that have exposure to farmland loans; but the recent weakness in farm commodity prices will likely have a negative impact on farmland values. So, those credit unions making farmland loans also warrant careful monitoring.]

Thirteen credit unions have a real estate secured business loan to net worth ratio above 200 percent and 5 credit unions -- all state charters -- have a real estate secured business loan to net worth ratio in excess of 300 percent.

The two credit unions with the greatest net worth exposure to real estate secured business loans are involved in church financing. Evangelical Christian Credit Union (Brea, CA) has the greatest percentage of its net worth exposed to real estate secured business loans at 907.24 percent. America's Christian Credit Union (Glendora, CA) has the next largest exposure at 532.4 percent.

The following tables provides info on credit unions with real estate secured business loan exposures of at least 100 percent of net worth.

Read the statement.

Friday, December 18, 2015

Bethex FCU Liquidated

The National Credit Union Administration today liquidated Bethex Federal Credit Union of Bronx, New York.

USAlliance Federal Credit Union of Rye, New York, immediately assumed Bethex Federal Credit Union’s assets, member shares and most loans. USAlliance is a federally chartered credit union with a low-income credit union designation that has 83,102 members and assets of $1.07 billion, according to the credit union’s most recent Call Report.

NCUA placed Bethex Federal Credit Union into conservatorship on September 18, 2015. NCUA made the decision to liquidate Bethex and discontinue its operations after determining the credit union was insolvent with no prospect for restoring viable operations on its own.

The credit union reported a loss of $851,367 for the first three quarters of 2015. As of September 30, 13.53 percent of the credit union's loans were 60 days or more past due. On November 18, 2015, the credit union repurchased $502,000 it owed in subordinated debt from the TARP Community Development Capital Initiative.

At the time of liquidation and subsequent purchase by USAlliance, Bethex served 5,824 members and had assets of $12.2 million, according to the credit union’s most recent Call Report.

Bethex Federal Credit Union is the tenth federally insured credit union liquidation in 2015.

Read the press release.

USAlliance Federal Credit Union of Rye, New York, immediately assumed Bethex Federal Credit Union’s assets, member shares and most loans. USAlliance is a federally chartered credit union with a low-income credit union designation that has 83,102 members and assets of $1.07 billion, according to the credit union’s most recent Call Report.

NCUA placed Bethex Federal Credit Union into conservatorship on September 18, 2015. NCUA made the decision to liquidate Bethex and discontinue its operations after determining the credit union was insolvent with no prospect for restoring viable operations on its own.

The credit union reported a loss of $851,367 for the first three quarters of 2015. As of September 30, 13.53 percent of the credit union's loans were 60 days or more past due. On November 18, 2015, the credit union repurchased $502,000 it owed in subordinated debt from the TARP Community Development Capital Initiative.

At the time of liquidation and subsequent purchase by USAlliance, Bethex served 5,824 members and had assets of $12.2 million, according to the credit union’s most recent Call Report.

Bethex Federal Credit Union is the tenth federally insured credit union liquidation in 2015.

Read the press release.

A.E.A. FCU Returned to Its Members

Five years after placing A.E.A. Federal Credit Union of Yuma, Arizona into conservatorship, the National Credit Union Administration returned control of A.E.A. Federal Credit Union to its members.

According to its September 2015 call report, credit union was counting $12.8 million in subordinated debt as net worth, which is highly likely Section 208 assistance from the National Credit Union Share Insurance Fund. Without this section 208 assistance the credit union would be critically undercapitalized.

A.E.A. FCU is the second credit union to emerge from conservatorship this year. The other credit union was Keys FCU (Key West, FL).

Read the story.

According to its September 2015 call report, credit union was counting $12.8 million in subordinated debt as net worth, which is highly likely Section 208 assistance from the National Credit Union Share Insurance Fund. Without this section 208 assistance the credit union would be critically undercapitalized.

A.E.A. FCU is the second credit union to emerge from conservatorship this year. The other credit union was Keys FCU (Key West, FL).

Read the story.

Monterey CU Withdraws Application to Become a Mutual Savings Bank

Silicon Valley Business Journal is reporting that Monterey Credit Union has withdrawn its application to switch to a mutual savings bank charter.

According to Silicon Valley Business Journal, the credit union pulled its application on November 19. This action came 16 months after the credit union's members voted to switch to a bank charter.

The story did not elaborate on why the credit union pulled its application.

Read the story.

According to Silicon Valley Business Journal, the credit union pulled its application on November 19. This action came 16 months after the credit union's members voted to switch to a bank charter.

The story did not elaborate on why the credit union pulled its application.

Read the story.

Wednesday, December 16, 2015

Proposal Would Allow 19.3 Million Vets to Join CUs Serving the Armed Forces

The National Credit Union Administration (NCUA) Board is proposing to include within a credit union’s common bond the honorably discharged veterans of any branch of the United States Armed Forces that is listed in a credit union's charter.

This provision would allow veterans to be eligible for credit union membership beyond their active duty status.

So, this means 19.3 million veterans will have continued access to credit unions that serve various branches of the military.

In justifying its position, the NCUA Board wrote that "[a]ctive duty and discharged military personnel and their families share a similar affinity, typically maintaining a close relationship with their active duty branch of service, largely through Armed Forces associations, publications and continued access to military bases, such as Veterans Administration facilities, base commissaries, post exchanges, and morale, welfare and recreation sponsored programs."

It appears that Navy Federal Credit Union and Pentagon Federal Credit Union wrote this provision, as they will be the beneficiaries of this proposed change to NCUA's field of membership rule.

This provision would allow veterans to be eligible for credit union membership beyond their active duty status.

So, this means 19.3 million veterans will have continued access to credit unions that serve various branches of the military.

In justifying its position, the NCUA Board wrote that "[a]ctive duty and discharged military personnel and their families share a similar affinity, typically maintaining a close relationship with their active duty branch of service, largely through Armed Forces associations, publications and continued access to military bases, such as Veterans Administration facilities, base commissaries, post exchanges, and morale, welfare and recreation sponsored programs."

It appears that Navy Federal Credit Union and Pentagon Federal Credit Union wrote this provision, as they will be the beneficiaries of this proposed change to NCUA's field of membership rule.

Tuesday, December 15, 2015

Credit Union Journal: NCUA Had One 'Whopper Year' On Regulatory Front in 2015

Credit Union Journal wrote that 2015 was a noteworthy year on the regulatory front for the National Credit Union Administration (NCUA).

With the exception of NCUA' controversial risk-based capital rule, which the credit union industry opposed, the agency was active in easing the regulatory burden on credit unions.

NCUA provided regulatory relief to a number of credit unions by doubling the asset threshold size for a small credit union designation to $100 million.

Also, NCUA eliminated its fixed asset rule.

Furthermore, NCUA proposed sweeping changes to its member business lending rule and field of membership regulation, which the agency will likely finalize in 2016.

As I told Credit Union Journal, "Debbie Matz said she was going to [provide relief], and she delivered."

Read the story (subscription required).

With the exception of NCUA' controversial risk-based capital rule, which the credit union industry opposed, the agency was active in easing the regulatory burden on credit unions.

NCUA provided regulatory relief to a number of credit unions by doubling the asset threshold size for a small credit union designation to $100 million.

Also, NCUA eliminated its fixed asset rule.

Furthermore, NCUA proposed sweeping changes to its member business lending rule and field of membership regulation, which the agency will likely finalize in 2016.

As I told Credit Union Journal, "Debbie Matz said she was going to [provide relief], and she delivered."

Read the story (subscription required).

Monday, December 14, 2015

A Majority of CUs Have Fewer Members Compared to a Year Ago

While overall credit union membership continued to grow, more than half of all credit unions have fewer members as of September 30, 2015 compared to a year ago, according to the National Credit Union Administration (NCUA).

Fifty-two percent of federally insured credit unions experienced a year-over-year decline in membership as of the end of the third quarter 2015.

The median rate of growth for credit unions was negative 0.2 percent.

Twenty-three states reported negative median membership growth rate for federally insured credit unions. Federally insured credit unions in Pennsylvania had the lowest median membership growth rate at -2.2 percent.

NCUA noted that membership growth is concentrated in the larger credit unions.

On the other hand, credit unions with falling membership tend to be small. Approximately 75 percent of the credit unions with negative membership growth had less than $50 million in assets.

Read the press release.

Fifty-two percent of federally insured credit unions experienced a year-over-year decline in membership as of the end of the third quarter 2015.

The median rate of growth for credit unions was negative 0.2 percent.

Twenty-three states reported negative median membership growth rate for federally insured credit unions. Federally insured credit unions in Pennsylvania had the lowest median membership growth rate at -2.2 percent.

NCUA noted that membership growth is concentrated in the larger credit unions.

On the other hand, credit unions with falling membership tend to be small. Approximately 75 percent of the credit unions with negative membership growth had less than $50 million in assets.

Read the press release.

Friday, December 11, 2015

Self-Help CU Funds $18 Million Construction Loan for Miami Charter School

The Sports Leadership and Management Academy charter school obtained a $17.97 million construction loan from a North Carolina-based credit union to build its complex in Miami’s Little Havana.

Self-Help Credit Union granted the mortgage to Miami School Group for an 80,552-square-foot school.

The school was co-founded by Christian Perez, also known as recording artist Pitbull.

However, how can a credit union based in Durham, N.C. provide a $18 million construction loan for school in Miami, Florida co-founded by Pitbull?

What is the common bond?

The best guess is a $5 one-time donation to the Center for Community Self Help.

Read the story.

Self-Help Credit Union granted the mortgage to Miami School Group for an 80,552-square-foot school.

The school was co-founded by Christian Perez, also known as recording artist Pitbull.

However, how can a credit union based in Durham, N.C. provide a $18 million construction loan for school in Miami, Florida co-founded by Pitbull?

What is the common bond?

The best guess is a $5 one-time donation to the Center for Community Self Help.

Read the story.

Thursday, December 10, 2015

Morgan Stanley Settles Lawsuit with NCUA over Failed Corporate CUs

The National Credit Union Administration (NCUA) announced a settlement with Morgan Stanley for $225 million to resolve claims arising from losses related to corporate credit unions’ purchases of faulty residential mortgage-backed securities.

The settlement covers claims asserted in 2013 by the NCUA Board on behalf of U.S. Central Federal Credit Union, Western Corporate Federal Credit Union, Members United Corporate Federal Credit Union and Southwest Corporate Federal Credit Union.

NCUA will dismiss pending lawsuits against Morgan Stanley in federal district courts in New York and Kansas. Morgan Stanley does not admit fault in the settlement.

Read the press release.

The settlement covers claims asserted in 2013 by the NCUA Board on behalf of U.S. Central Federal Credit Union, Western Corporate Federal Credit Union, Members United Corporate Federal Credit Union and Southwest Corporate Federal Credit Union.

NCUA will dismiss pending lawsuits against Morgan Stanley in federal district courts in New York and Kansas. Morgan Stanley does not admit fault in the settlement.

Read the press release.

NCUA: Community Charter Can Be a Combined Statistical Area

The National Credit Union Administration (NCUA) Board is proposing to allow a Combined Statistical Area with a population limit of 2.5 million to be treated as a de facto well-defined local community.

According to the Office of Management and Budget (OMB), there are currently 169 Combined Statistical Areas. These Combined Statistical Areas are comprised of 524 Core-based Statistical Areas. A Core-based Statistical Area is either a Metropolitan or Micropolitan Statistical Area.

According to 2013 Census Bureau estimates, only 20 Combined Statistical Areas exceeded the population threshold of 2.5 million.

OMB introduced the concept of Combined Statistical Area in 2000. OMB stated that Combined Statistical Areas can be characterized as representing larger regions that reflect broader social and economic interactions, such as wholesaling, commodity distribution, and weekend recreation activities.

However, two Federal Courts ruled against NCUA in Utah and Pennsylvania, when the agency approved community charters comprised of multiple core-based statistical areas. The Federal Courts wrote that the areas did not meet the requirement of being well-defined local community.

So, how can a larger region represented by a Combined Statistical Area meet the requirement of being a local community?

NCUA is clearly trying to accomplish through the regulatory process what it has not been able to do legislatively.

According to the Office of Management and Budget (OMB), there are currently 169 Combined Statistical Areas. These Combined Statistical Areas are comprised of 524 Core-based Statistical Areas. A Core-based Statistical Area is either a Metropolitan or Micropolitan Statistical Area.

According to 2013 Census Bureau estimates, only 20 Combined Statistical Areas exceeded the population threshold of 2.5 million.

OMB introduced the concept of Combined Statistical Area in 2000. OMB stated that Combined Statistical Areas can be characterized as representing larger regions that reflect broader social and economic interactions, such as wholesaling, commodity distribution, and weekend recreation activities.

However, two Federal Courts ruled against NCUA in Utah and Pennsylvania, when the agency approved community charters comprised of multiple core-based statistical areas. The Federal Courts wrote that the areas did not meet the requirement of being well-defined local community.

So, how can a larger region represented by a Combined Statistical Area meet the requirement of being a local community?

NCUA is clearly trying to accomplish through the regulatory process what it has not been able to do legislatively.

Wednesday, December 9, 2015

San Francisco FCU Unveils 100 Percent LTV Jumbo Mortgages

Citing skyrocketing housing costs, San Francisco Federal Credit Union announced a new loan program that will allow San Francisco-area borrowers to finance up to 100 percent of their mortgage – with no requirement for private mortgage insurance – on loans up to $2 million.

The new loan program is called POPPYLOAN, which stands for Proud Ownership Purchase Program for You.

According to the credit union, POPPYLOAN is available to anyone who works in San Francisco or San Mateo Counties and can be used to purchase a home in the nine Bay Area Counties: San Francisco, San Mateo, Marin, Napa, Sonoma, Santa Clara, Alameda, Contra Costa, or Solano.

To qualify for POPPYLOAN, borrowers must be 18 years or older and purchasing a single family home, townhouse, condominium, or 2-to-4 unit multi-family dwelling as their primary residence. Eligibility for the loan also depends on a number of additional factors, such as credit scores, income, employment status, and property value.

POPPYLOAN is structured as a 5/5 adjustable rate, 30-year mortgage. The interest rate on the mortgage cannot increase by more than 2 percent every five years and no more than 6 percent over the life of the loan.

However, the loan is not available to refinance an existing mortgage.

Read the article.

The new loan program is called POPPYLOAN, which stands for Proud Ownership Purchase Program for You.

According to the credit union, POPPYLOAN is available to anyone who works in San Francisco or San Mateo Counties and can be used to purchase a home in the nine Bay Area Counties: San Francisco, San Mateo, Marin, Napa, Sonoma, Santa Clara, Alameda, Contra Costa, or Solano.

To qualify for POPPYLOAN, borrowers must be 18 years or older and purchasing a single family home, townhouse, condominium, or 2-to-4 unit multi-family dwelling as their primary residence. Eligibility for the loan also depends on a number of additional factors, such as credit scores, income, employment status, and property value.

POPPYLOAN is structured as a 5/5 adjustable rate, 30-year mortgage. The interest rate on the mortgage cannot increase by more than 2 percent every five years and no more than 6 percent over the life of the loan.

However, the loan is not available to refinance an existing mortgage.

Read the article.

Tuesday, December 8, 2015

CUs Received More Than $120 Billion in Emergency Liquidity and Guarantees During Financial Crisis

Testifying before the House Financial Services Committee on December 8, National Credit Union Administration (NCUA) Chairman Debbie Matz provided information about the extraordinary measures that were taken by NCUA to support the credit union system during the financial crisis and Great Recession.

Chairman Matz noted consumer-oriented, member-owned credit union system suffered sizable losses, as a result of the financial crisis. Ninety retail credit unions failed because they were not holding sufficient capital to cover their risks.

Chairman Matz went on to state that the failure of five corporate credit unions had near-catastrophic consequences for all surviving credit unions, causing Congress to create the Temporary Corporate Credit Union Stabilization Fund.

Furthermore, she stated NCUA injected more than $120 billion of emergency liquidity and guarantees to stabilize the credit union system - more than $20 billion in liquidity assistance through the Central Liquidity Facility and over $100 billion in guarantees.

She also pointed out that NCUA borrowed $5 billion from the U.S. Treasury to support the credit union system.

Read the testimony.

Chairman Matz noted consumer-oriented, member-owned credit union system suffered sizable losses, as a result of the financial crisis. Ninety retail credit unions failed because they were not holding sufficient capital to cover their risks.

Chairman Matz went on to state that the failure of five corporate credit unions had near-catastrophic consequences for all surviving credit unions, causing Congress to create the Temporary Corporate Credit Union Stabilization Fund.

Furthermore, she stated NCUA injected more than $120 billion of emergency liquidity and guarantees to stabilize the credit union system - more than $20 billion in liquidity assistance through the Central Liquidity Facility and over $100 billion in guarantees.

She also pointed out that NCUA borrowed $5 billion from the U.S. Treasury to support the credit union system.

Read the testimony.

Monday, December 7, 2015

U.S. Eagle FCU Secures Signage Rights to New Mexico's Tallest Building

The Albuquerque Journal is reporting that U.S. Eagle Federal Credit Union has secured signage rights to New Mexico’s tallest building, the 22-story Albuquerque Plaza in Downtown Albuquerque.

The credit union will also open a branch on the first floor of the building.

The credit union has $855 million in assets as of the end of the third quarter.

The price and terms for the signage rights were not disclosed.

Read the story.

The credit union will also open a branch on the first floor of the building.

The credit union has $855 million in assets as of the end of the third quarter.

The price and terms for the signage rights were not disclosed.

Read the story.

Redlining Minority and Low-Income Communities?

One provision in the National Credit Union Administration (NCUA) Board proposal to amend its field of membership rules could result in the redlining of low-income, minority, and underserved communities.

The NCUA Board is proposing to repeal the "core area" requirement when a federal credit union (FCU) applies for a community charter consisting of a portion of a Core Based Statistical Area.

A Core Based Statistical Area is either a metropolitan statistical area or a micropolitan statistical area.

As background, NCUA's FOM regulation since 20101 requires that when a FCU applies to serve a community consisting of a portion of a Core Based Statistical Area, that portion must include the Core Based Statistical Area’s “core area.” NCUA defines a "core area" as the most populated county or named municipality in the Core Based Statistical Area.

NCUA noted that the primary purpose of this requirement was to acknowledge the core area of a Core Based Statistical Area as the typical focal point for common interests and interaction among residents. An additional purpose was to extend FCU services to low-income persons and underserved areas, both typically located in the "core area" of a Core Based Statistical Area.

NCUA is proposing to repeal this "core area" requirement; because the agency's review of FCU’s business and marketing plans over the last five years show FCUs are adequately serving low-income persons and underserved areas. In place of the "core area" requirement, NCUA proposes to annually review for three years a FCU's progress in implementing its marketing and business plan.

Unfortunately, the repeal of the "core area" requirement could allow FCUs to design community charters that resemble donuts by serving wealthier suburban counties and excluding markets containing low-income and minority communities that reside in the core area.

NCUA should ensure that community charters do not redline low-income, minority, and underserved communities.

The NCUA Board is proposing to repeal the "core area" requirement when a federal credit union (FCU) applies for a community charter consisting of a portion of a Core Based Statistical Area.

A Core Based Statistical Area is either a metropolitan statistical area or a micropolitan statistical area.

As background, NCUA's FOM regulation since 20101 requires that when a FCU applies to serve a community consisting of a portion of a Core Based Statistical Area, that portion must include the Core Based Statistical Area’s “core area.” NCUA defines a "core area" as the most populated county or named municipality in the Core Based Statistical Area.

NCUA noted that the primary purpose of this requirement was to acknowledge the core area of a Core Based Statistical Area as the typical focal point for common interests and interaction among residents. An additional purpose was to extend FCU services to low-income persons and underserved areas, both typically located in the "core area" of a Core Based Statistical Area.

NCUA is proposing to repeal this "core area" requirement; because the agency's review of FCU’s business and marketing plans over the last five years show FCUs are adequately serving low-income persons and underserved areas. In place of the "core area" requirement, NCUA proposes to annually review for three years a FCU's progress in implementing its marketing and business plan.

Unfortunately, the repeal of the "core area" requirement could allow FCUs to design community charters that resemble donuts by serving wealthier suburban counties and excluding markets containing low-income and minority communities that reside in the core area.

NCUA should ensure that community charters do not redline low-income, minority, and underserved communities.

Sunday, December 6, 2015

Privately Insured CUs Can Become Members of FHLBs

Privately insured credit unions can now become members of the Federal Home Loan Banks (FHLBs).

President Obama on December 4 signed into law the Highway Bill (H.R. 22).

Section 82001 of the bill allows privately insured credit unions to join the Federal Home Loan Banks "only if the appropriate supervisor of the State in which the credit union is chartered has determined that the credit union meets all the eligibility requirements for Federal deposit insurance as of the date of the application for membership."

Also, the bill protects FHLB advances from loss by giving FHLBs priority to collateral backing FHLB advances.

This section of the bill also authorizes the GAO to conduct an audit on the adequacy of insurance reserves held by a private

deposit insurer and on the level of compliance with Federal regulations relating to the disclosure of a lack of Federal deposit insurance.

American Share Insurance is the only private insurer of credit unions.

Read the bill.

President Obama on December 4 signed into law the Highway Bill (H.R. 22).

Section 82001 of the bill allows privately insured credit unions to join the Federal Home Loan Banks "only if the appropriate supervisor of the State in which the credit union is chartered has determined that the credit union meets all the eligibility requirements for Federal deposit insurance as of the date of the application for membership."

Also, the bill protects FHLB advances from loss by giving FHLBs priority to collateral backing FHLB advances.

This section of the bill also authorizes the GAO to conduct an audit on the adequacy of insurance reserves held by a private

deposit insurer and on the level of compliance with Federal regulations relating to the disclosure of a lack of Federal deposit insurance.

American Share Insurance is the only private insurer of credit unions.

Read the bill.

Bank and CU Trade Groups File Brief regarding Recent FCC Order

The American Bankers Association, the Credit Union National Association, and the Independent Community Bankers Association filed a friend of the court brief on Wednesday in an appeal of a recent order by the Federal Communications Commission (FCC) regarding the Telephone Consumer Protection Act (FCC).

In that order, the FCC granted four exemptions from the TCPA for data breach and fraud-related calls. However, the FCC also interpreted certain provisions in the TCPA in ways that will make it more difficult for banks and credit unions to send other valuable communications to their customers.

The brief argues that the order “severely restricts the ability of financial institutions and other callers to engage in useful, and often urgent, communications with their customers and members.”

The brief supported the petitions filed by nine industry members seeking a review of the FCC’s order by the D.C. Circuit Court of Appeals.

The brief described the types of messages financial institutions send to their customers and how the FCC’s order will prevent many of these communications from occurring.

Read the brief.

In that order, the FCC granted four exemptions from the TCPA for data breach and fraud-related calls. However, the FCC also interpreted certain provisions in the TCPA in ways that will make it more difficult for banks and credit unions to send other valuable communications to their customers.

The brief argues that the order “severely restricts the ability of financial institutions and other callers to engage in useful, and often urgent, communications with their customers and members.”

The brief supported the petitions filed by nine industry members seeking a review of the FCC’s order by the D.C. Circuit Court of Appeals.

The brief described the types of messages financial institutions send to their customers and how the FCC’s order will prevent many of these communications from occurring.

Read the brief.

Saturday, December 5, 2015

Hiway Federal Credit Union Renews Sponsorship of NHL Team

Hiway Federal Credit Union (St. Paul, MN) has renewed its sponsorship of National Hockey League's Minnesota Wild for two more years.

Hiway Federal Credit Union will be the hockey team's official credit union through the Wild's 2016-2017 season, the St. Paul-based lender said.

The deal, which started last season, includes advertising at St. Paul's Xcel Energy Center, ATMs in the arena, team-branded accounts and cards, and prize drawings and discounts at Hockey Lodge retail locations.

The price of the deal was not disclosed.

Read the story.

Hiway Federal Credit Union will be the hockey team's official credit union through the Wild's 2016-2017 season, the St. Paul-based lender said.

The deal, which started last season, includes advertising at St. Paul's Xcel Energy Center, ATMs in the arena, team-branded accounts and cards, and prize drawings and discounts at Hockey Lodge retail locations.

The price of the deal was not disclosed.

Read the story.

Friday, December 4, 2015

Credit Unions Post Strong Loan Growthn Q3, Delinquencies Up for Second Consecutive Quarter

The National Credit Union Administration (NCUA) is reporting that federally insured credit unions posted strong loan growth during the third quarter.

Total loans at federally insured credit unions reached $769.5 billion in the third quarter of 2015, an increase of 3.3 percent from the previous quarter and 10.7 percent from a year earlier. All major loan categories posted growth during the third quarter -- non-federally guaranteed student loans grew by 5.1 percent; new auto loans were up 4.4 percent; used auto loans rose by 3.7 percent; first mortgage loans and member business loans increased by 3 percent.

The NCUA reported a surge in indirect lending at federally insured credit unions. Indirect loans were $131.5 billion at the end of the third quarter of 2015 and represented 17.09 percent of total industry loans. This is up from approximately $108 billion a year earlier, which accounted for 15.53 percent of all credit union loans.

Overall, share and deposit accounts at federally insured credit unions increased $5.6 billion from the second quarter 2015 and $53.3 billion from the end of the third quarter of 2014 to $992.5 billion.

Because loans grew at a faster rate than shares and deposits, the loan-to-share ratio rose from 75.52 percent at the end of the second quarter to 77.53 percent as of September 30, 2015.

Credit Unions Earned $2.3 Billion in Q3

Federally insured credit unions continued to report positive net income in the third quarter, $2.3 billion, a decline of $82 million, or 3.5 percent, from the third quarter of 2014. As a whole, federally insured credit unions have recorded positive net income for 23 straight quarters.

Year-to-date federally-insured credit union profits were almost $6.9 billion -- up from slightly below $6.8 billion for the same time period of 2014.

Federally insured credit unions’ year-to-date return on average assets ratio stood at an annualized 80 basis points at the end of the third quarter, slightly below the level in the third quarter of 2014. Overall, 78 percent of federally insured credit unions reported positive returns on average assets for the first three quarters of 2015, compared to 76 percent in the first three quarters of 2014.

98 Percent of Credit Unions Were Well-Capitalized

The credit union industry continued to build its net worth during the quarter. The credit union industry's net worth ratio increased by 7 basis points during the third quarter to 10.99 percent.

The percentage of federally insured credit unions that were well-capitalized rose in the third quarter, with 98.0 percent reporting a net worth ratio at or above the statutorily required 7.0 percent. A year earlier, 97.5 percent of credit unions were well-capitalized. As of September 30, 2015, 34 federally insured credit unions were undercapitalized.

Delinquencies Rose for Second Consecutive Quarter

It appears that the credit cycle is turning. Delinquent loans are up for the second consecutive quarter. Loans 60 days or more past due rose by approximately $450 million during the quarter to almost $6 billion and is up by more than $1 billion since March 31, 2015.

In addition, early delinquencies were $6.1 billion at the end of the third quarter, an increase of $456 million from the end of the second quarter.

According to NCUA, delinquency rates edged higher during the quarter, while net charge-off rates unchanged. The delinquency rate at federally insured credit unions rose in the third quarter to 78 basis points, up from 74 basis points the previous quarter, but still below the 85 basis-point level in the third quarter of 2014. The net charge-off ratio was an annualized 46 basis points year-to-date -- the same as in the second quarter of 2015 and down from 48 basis points through the end of the third quarter of 2014.

Read the press release.

Total loans at federally insured credit unions reached $769.5 billion in the third quarter of 2015, an increase of 3.3 percent from the previous quarter and 10.7 percent from a year earlier. All major loan categories posted growth during the third quarter -- non-federally guaranteed student loans grew by 5.1 percent; new auto loans were up 4.4 percent; used auto loans rose by 3.7 percent; first mortgage loans and member business loans increased by 3 percent.

The NCUA reported a surge in indirect lending at federally insured credit unions. Indirect loans were $131.5 billion at the end of the third quarter of 2015 and represented 17.09 percent of total industry loans. This is up from approximately $108 billion a year earlier, which accounted for 15.53 percent of all credit union loans.

Overall, share and deposit accounts at federally insured credit unions increased $5.6 billion from the second quarter 2015 and $53.3 billion from the end of the third quarter of 2014 to $992.5 billion.

Because loans grew at a faster rate than shares and deposits, the loan-to-share ratio rose from 75.52 percent at the end of the second quarter to 77.53 percent as of September 30, 2015.

Credit Unions Earned $2.3 Billion in Q3

Federally insured credit unions continued to report positive net income in the third quarter, $2.3 billion, a decline of $82 million, or 3.5 percent, from the third quarter of 2014. As a whole, federally insured credit unions have recorded positive net income for 23 straight quarters.

Year-to-date federally-insured credit union profits were almost $6.9 billion -- up from slightly below $6.8 billion for the same time period of 2014.

Federally insured credit unions’ year-to-date return on average assets ratio stood at an annualized 80 basis points at the end of the third quarter, slightly below the level in the third quarter of 2014. Overall, 78 percent of federally insured credit unions reported positive returns on average assets for the first three quarters of 2015, compared to 76 percent in the first three quarters of 2014.

98 Percent of Credit Unions Were Well-Capitalized

The credit union industry continued to build its net worth during the quarter. The credit union industry's net worth ratio increased by 7 basis points during the third quarter to 10.99 percent.

The percentage of federally insured credit unions that were well-capitalized rose in the third quarter, with 98.0 percent reporting a net worth ratio at or above the statutorily required 7.0 percent. A year earlier, 97.5 percent of credit unions were well-capitalized. As of September 30, 2015, 34 federally insured credit unions were undercapitalized.

Delinquencies Rose for Second Consecutive Quarter

It appears that the credit cycle is turning. Delinquent loans are up for the second consecutive quarter. Loans 60 days or more past due rose by approximately $450 million during the quarter to almost $6 billion and is up by more than $1 billion since March 31, 2015.

In addition, early delinquencies were $6.1 billion at the end of the third quarter, an increase of $456 million from the end of the second quarter.

According to NCUA, delinquency rates edged higher during the quarter, while net charge-off rates unchanged. The delinquency rate at federally insured credit unions rose in the third quarter to 78 basis points, up from 74 basis points the previous quarter, but still below the 85 basis-point level in the third quarter of 2014. The net charge-off ratio was an annualized 46 basis points year-to-date -- the same as in the second quarter of 2015 and down from 48 basis points through the end of the third quarter of 2014.

Read the press release.

Thursday, December 3, 2015

Alaska USA Adds Underserved Area in Arizona

The National Credit Union Administration (NCUA) in October approved Alaska USA Federal Credit Union's addition of 413 underserved census tracts in Maricopa County, Arizona.

This underserved area expansion will allow Alaska USA to serve almost 1.7 million residents in Maricopa County -- further growing the credit union's presence in Arizona.

Alaska USA currently operates in four Western states -- Alaska, Arizona, California, and Washington.

This underserved area expansion will allow Alaska USA to serve almost 1.7 million residents in Maricopa County -- further growing the credit union's presence in Arizona.

Alaska USA currently operates in four Western states -- Alaska, Arizona, California, and Washington.

Wednesday, December 2, 2015

California Coast CU Forging Sponsorship Deal with City of San Diego

The San Diego Union Tribune is reporting that California Coast Credit Union is forging a deal with the City of San Diego to become a city sponsor.

The deal is valued at approximately $3 million over 5 years and awaits final approval by full city council.

The deal with California Coast would provide $650,000 cash over the next five years plus services for employees and the community with an estimated valued of nearly $2.5 million.

In exchange, California Coast would become the official financial partner of the city, get exclusive rights to market its services to city employees and retirees, and be included in publicity for city-sponsored community programs.

The five-year deal would allow the city or the $1.9 billion credit union to opt out after three years.

Read the story.

The deal is valued at approximately $3 million over 5 years and awaits final approval by full city council.

The deal with California Coast would provide $650,000 cash over the next five years plus services for employees and the community with an estimated valued of nearly $2.5 million.

In exchange, California Coast would become the official financial partner of the city, get exclusive rights to market its services to city employees and retirees, and be included in publicity for city-sponsored community programs.

The five-year deal would allow the city or the $1.9 billion credit union to opt out after three years.

Read the story.

MidFlorida CU Is Sued over Misleading Overdraft Practices

Reuters is reporting that MidFlorida Credit Union (Lakeland, FL) was hit with a proposed class action lawsuit accusing the credit union of violating federal law by charging customers overdraft fees when members had enough money in their checking accounts to cover any debits.

Filed last week, the lawsuit said MidFlorida Credit Union used an artificial "available balance" to decide whether to charge an overdraft, instead of the actual balance in a customer's account.

Read the story.

Filed last week, the lawsuit said MidFlorida Credit Union used an artificial "available balance" to decide whether to charge an overdraft, instead of the actual balance in a customer's account.

Read the story.

Tuesday, December 1, 2015

Greater Abyssinia Federal Credit Union Closed

The National Credit Union Administration (NCUA) closed Greater Abyssinia Federal Credit Union of Cleveland, Ohio.

NCUA made the decision to liquidate Greater Abyssinia Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operation.

The credit union reported that 28.46 percent of its loans and 10.76 percent of its assets were 60 days or more past due. The credit union also reported a 2015 year-to-date loss of almost $20 thousand and a full year loss for 2014 of almost $34 thousand.

Greater Abyssinia Federal Credit Union served 425 members and had assets of $412,775, according to the credit union’s most recent Call Report.

Greater Abyssinia Federal Credit Union is the ninth federally insured credit union liquidation in 2015.

Read the press release.

NCUA made the decision to liquidate Greater Abyssinia Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operation.

The credit union reported that 28.46 percent of its loans and 10.76 percent of its assets were 60 days or more past due. The credit union also reported a 2015 year-to-date loss of almost $20 thousand and a full year loss for 2014 of almost $34 thousand.

Greater Abyssinia Federal Credit Union served 425 members and had assets of $412,775, according to the credit union’s most recent Call Report.

Greater Abyssinia Federal Credit Union is the ninth federally insured credit union liquidation in 2015.

Read the press release.

Small Business Data Collection on Bureau's Rulemaking Agenda

On the Consumer Financial Protection Bureau's regulatory agenda for the next year is the collection of information on financial institutions' lending to women-owned, minority-owned, and small businesses.

This data collection is mandated by the Section 1071 of Dodd-Frank Act.

According to the Dodd-Frank Act, the purpose of this data collection is to facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority- owned, and small businesses.

According to the Dodd-Frank Act, the following information will be collected by the Consumer Financial Protection Bureau (Bureau):

(A) the number of the application and the date on which the application was received;

(B) the type and purpose of the loan or other credit being applied for;

(C) the amount of the credit or credit limit applied for, and the amount of the credit transaction or the credit limit approved for such applicant;

(D) the type of action taken with respect to such application, and the date of such action;

(E) the census tract in which is located the principal place of business of the women-owned, minority-owned, or small business loan applicant;

(F) the gross annual revenue of the business in the last fiscal year of the women-owned, minority-owned, or small business loan applicant preceding the date of the application; ‘‘(G) the race, sex, and ethnicity of the principal owners of the business; and

(H) any additional data that the Bureau determines would aid in fulfilling the purposes of this section.

The Bureau indicated that its data collection efforts will build off a similar rule it finalized regarding the collection of home mortgage lending data.

This data collection mandate will impose a new regulatory burden on banks and credit unions.

Read the Bureau's Fall Rulemaking Agenda.

This data collection is mandated by the Section 1071 of Dodd-Frank Act.

According to the Dodd-Frank Act, the purpose of this data collection is to facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority- owned, and small businesses.

According to the Dodd-Frank Act, the following information will be collected by the Consumer Financial Protection Bureau (Bureau):

(A) the number of the application and the date on which the application was received;

(B) the type and purpose of the loan or other credit being applied for;

(C) the amount of the credit or credit limit applied for, and the amount of the credit transaction or the credit limit approved for such applicant;

(D) the type of action taken with respect to such application, and the date of such action;

(E) the census tract in which is located the principal place of business of the women-owned, minority-owned, or small business loan applicant;

(F) the gross annual revenue of the business in the last fiscal year of the women-owned, minority-owned, or small business loan applicant preceding the date of the application; ‘‘(G) the race, sex, and ethnicity of the principal owners of the business; and

(H) any additional data that the Bureau determines would aid in fulfilling the purposes of this section.

The Bureau indicated that its data collection efforts will build off a similar rule it finalized regarding the collection of home mortgage lending data.

This data collection mandate will impose a new regulatory burden on banks and credit unions.

Read the Bureau's Fall Rulemaking Agenda.

Monday, November 30, 2015

CCTV-America on CU Taxi Medallion Lenders

CCTV-America examined the impact of Uber on the taxi medallion industry and its credit union lenders.

CCTV-America interviewed me for its story.

Here is a link to the story.

CCTV-America interviewed me for its story.

Here is a link to the story.

Friday, November 27, 2015

TDECU Commissioned Mural for TDECU Stadium Suite

TDECU commissioned artist Suzanne Sellers to create a mural for its suite at TDECU Stadium at the University of Houston.

The piece entitled: Victory, Character and Strength captures the driving spirit behind the University of Houston’s storied football program.

TDECU did not disclose the cost for the artwork.

Is commissioning artwork for a suite at a football stadium part of a credit union's tax exempt mission?

I also wonder if the members of the credit union think this is a good use of their money.

Read the press release.

The piece entitled: Victory, Character and Strength captures the driving spirit behind the University of Houston’s storied football program.

TDECU did not disclose the cost for the artwork.

Is commissioning artwork for a suite at a football stadium part of a credit union's tax exempt mission?

I also wonder if the members of the credit union think this is a good use of their money.

Read the press release.

Wednesday, November 25, 2015

NY Times: CU Start-Up Frustrated with Bureaucracy

The New York Times reported on the problem one credit union start-up had with the National Credit Union Administration (NCUA).

The credit union -- Internet Archive Federal Credit Union (New Brunswick, NJ) -- opened its door in 2012.

Credit union officials stated that they were frustrated by "a barrage of regulatory audits and limitations on its operations."

However, the article pointed out that this de novo credit union sought on several occasions to alter its business plans, including serving Bitcoin companies and providing international remittances for immigrant workers.

In my opinion, these changes in business plans at this start-up raised red flags with regulators and warranted increased oversight.

Read the story.

The credit union -- Internet Archive Federal Credit Union (New Brunswick, NJ) -- opened its door in 2012.

Credit union officials stated that they were frustrated by "a barrage of regulatory audits and limitations on its operations."

However, the article pointed out that this de novo credit union sought on several occasions to alter its business plans, including serving Bitcoin companies and providing international remittances for immigrant workers.

In my opinion, these changes in business plans at this start-up raised red flags with regulators and warranted increased oversight.

Read the story.

IG Report Recommends NCUA Add S to CAMEL Rating

The National Credit Union Administration (NCUA) Office of Inspector General (IG) recommended that NCUA add sensitivity to market risk (S) to its CAMEL rating.

Almost two decades earlier (January 1, 1997), the federal bank regulators -- The Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency -- added S to their CAMELS rating.

The IG report noted that NCUA may not be effectively capturing interest rate risk (IRR) under "L" in its CAMEL rating.

The IG wrote:

Read the report.

Almost two decades earlier (January 1, 1997), the federal bank regulators -- The Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency -- added S to their CAMELS rating.

The IG report noted that NCUA may not be effectively capturing interest rate risk (IRR) under "L" in its CAMEL rating.

The IG wrote:

[w]e determined that NCUA may not be effectively capturing IRR when assigning a composite CAMEL rating to a credit union. NCUA currently assesses sensitivity to market risk under the "L" in its CAMEL rating. However, combining sensitivity to market risk with liquidity may understate or obscure instances of high IRR exposure in a credit union. The addition of an “S” rating to its CAMEL Rating System to capture and separately assess a credit union’s sensitivity to market risk should improve NCUA’s ability to accurately measure and monitor interest rate risk. To better reflect the risk that changes in market rates will adversely affect a credit union’s capital and earnings, and in conjunction with a stated goal of NCUA’s IRR working group, we are making two recommendations in this report. We recommend NCUA management modify the current CAMEL Rating System by adding an “S” for market risk [S]ensitivity, and revising the “L” rating to reflect only liquidity factors.

Read the report.

Tuesday, November 24, 2015

NCUA Proposal Could Permit Seven State-wide FOMs

The National Credit Union Administration (NCUA) Board on November 19 issued a proposed rule for comment that would permit state-wide fields of membership (FOM) for seven states.

First, the NCUA Board is proposing that a Congressional District can constitute a well-defined local community. This represents a reversal of NCUA's previous position that a Congressional District did not meet the requirement of being a well-defined local community.

There are seven states represented by a single at large Congressional District. The seven states with a single at large Congressional District are: Alaska, Delaware, Montana, North Dakota, South Dakota, Vermont, and Wyoming. In addition, the District of Columbia and several U.S. territories would qualify as a well-defined local community.

However, I don't see how an at large state-wide Congressional District is local and demonstrates a commonality of interest or interaction among members. In fact, NCUA's FOM and Chartering Manual notes that a state does not meet the requirement of being local.

Second, the NCUA Board is proposing to expand the population size of a rural district. The Board is raising the population threshold from 250,000 to 1 million. The other requirement is that a rural district is sparsely populated -- no more than 100 people per square mile.

Currently, the states of Alaska, North Dakota, South Dakota, Vermont, and Wyoming have low population densities and are under the 1 million population threshold requirement. However, more than half of the residents in the states of Alaska, North Dakota, South Dakota, and Wyoming live in urban areas.

So, how can a whole state be treated as a rural district when more than half of the state's population lives in urban areas?

I will provide additional comments on other areas of this proposed rule over the next month.

Read the proposed rule.

First, the NCUA Board is proposing that a Congressional District can constitute a well-defined local community. This represents a reversal of NCUA's previous position that a Congressional District did not meet the requirement of being a well-defined local community.

There are seven states represented by a single at large Congressional District. The seven states with a single at large Congressional District are: Alaska, Delaware, Montana, North Dakota, South Dakota, Vermont, and Wyoming. In addition, the District of Columbia and several U.S. territories would qualify as a well-defined local community.

However, I don't see how an at large state-wide Congressional District is local and demonstrates a commonality of interest or interaction among members. In fact, NCUA's FOM and Chartering Manual notes that a state does not meet the requirement of being local.

Second, the NCUA Board is proposing to expand the population size of a rural district. The Board is raising the population threshold from 250,000 to 1 million. The other requirement is that a rural district is sparsely populated -- no more than 100 people per square mile.

Currently, the states of Alaska, North Dakota, South Dakota, Vermont, and Wyoming have low population densities and are under the 1 million population threshold requirement. However, more than half of the residents in the states of Alaska, North Dakota, South Dakota, and Wyoming live in urban areas.

So, how can a whole state be treated as a rural district when more than half of the state's population lives in urban areas?

I will provide additional comments on other areas of this proposed rule over the next month.

Read the proposed rule.

Monday, November 23, 2015

New Lawsuit Highlights Dire Financial Condition of Melrose

Owners of New York City's taxi "medallions" and three credit unions that finance taxi medallions filed on November 17 a lawsuit in U.S. District Court against the City of New York and the Taxi and Limousine Commission.

The complaint alleges disparate regulatory treatment of the taxi medallion industry compared to Uber and other e-hail providers. This disparate treatment according to the complaint violates the equal protection clause under the Fourteenth Amendment of the U.S. Constitution.

Moreover, the complaint outlines the worsening financial condition of one credit union -- Melrose Credit Union (Briarwood, NY).

Starting in paragraph 28 of the complaint, Melrose Credit Union states that it had aggregate taxicab medallion loan delinquencies of approximately $32,000 and no troubled debt restructurings as of January 2014. As of August 31, 2015, Melrose’s medallion loan delinquencies totaled $226,552,719––an increase of approximately 10 percent in a one month period. Likewise, as of August 31, 2015, troubled debt restructurings totaled approximately $195,529,000. Thus, Melrose reached approximately $422,081,719 in delinquencies and troubled debt restructurings––an increase of approximately 7 percent in a single month, and a staggering 34 percent increase since May 31, 2015.

Also in paragraph 31, Melrose Credit Union stated that it has hundreds of medallion loans maturing between now and February 2016, which will worsen the problem. In fact, Melrose has 190 medallion loans maturing in December with almost $83,000,000 in balloon payments becoming due. However, many of these loans are probably underwater due to falling taxi medallion prices.

Furthermore in paragraph 54, Melrose alleges that the Taxi and Limousine Commission overstated the average value of taxi medallions that the credit union used to underwrite the purchase of medallions until October 2013. Elsewhere in the complaint, it states that the Taxi and Limousine Commission, when calculating the average value for taxi medallions, tossed out medallion purchases the Commission believed were below the fair value for medallions. This might suggest that Melrose may have advanced more funds than would have been prudent based upon overinflated valuation of taxi medallions.

In paragraph 187, the complaint states that Melrose financed approximately 128 of the roughly 200 accessible medallions sold at the November 2013 auction. Today, 108 of the approximately 128 (or 84 percent) of the medallions sold in the November 2013 auction and financed by Plaintiff Melrose are now classified as either delinquent or troubled debt. This would suggest recent vintage taxi medallion loans could account for the bulk of the delinquencies and trouble debt restructurings.

For example, Melrose's Call Reports state that the credit union made almost 2,000 member business loans worth almost $878 million in 2013 and approximately 1302 member business loans worth almost $600 million in 2014. Presumably, most of these loans were for taxi medallions.

This information would suggest delinquencies and troubled debt restructurings are only going to go higher.

The following link to an article about the lawsuit has a link to the complaint. Read the article.

The complaint alleges disparate regulatory treatment of the taxi medallion industry compared to Uber and other e-hail providers. This disparate treatment according to the complaint violates the equal protection clause under the Fourteenth Amendment of the U.S. Constitution.

Moreover, the complaint outlines the worsening financial condition of one credit union -- Melrose Credit Union (Briarwood, NY).

Starting in paragraph 28 of the complaint, Melrose Credit Union states that it had aggregate taxicab medallion loan delinquencies of approximately $32,000 and no troubled debt restructurings as of January 2014. As of August 31, 2015, Melrose’s medallion loan delinquencies totaled $226,552,719––an increase of approximately 10 percent in a one month period. Likewise, as of August 31, 2015, troubled debt restructurings totaled approximately $195,529,000. Thus, Melrose reached approximately $422,081,719 in delinquencies and troubled debt restructurings––an increase of approximately 7 percent in a single month, and a staggering 34 percent increase since May 31, 2015.

Also in paragraph 31, Melrose Credit Union stated that it has hundreds of medallion loans maturing between now and February 2016, which will worsen the problem. In fact, Melrose has 190 medallion loans maturing in December with almost $83,000,000 in balloon payments becoming due. However, many of these loans are probably underwater due to falling taxi medallion prices.

Furthermore in paragraph 54, Melrose alleges that the Taxi and Limousine Commission overstated the average value of taxi medallions that the credit union used to underwrite the purchase of medallions until October 2013. Elsewhere in the complaint, it states that the Taxi and Limousine Commission, when calculating the average value for taxi medallions, tossed out medallion purchases the Commission believed were below the fair value for medallions. This might suggest that Melrose may have advanced more funds than would have been prudent based upon overinflated valuation of taxi medallions.

In paragraph 187, the complaint states that Melrose financed approximately 128 of the roughly 200 accessible medallions sold at the November 2013 auction. Today, 108 of the approximately 128 (or 84 percent) of the medallions sold in the November 2013 auction and financed by Plaintiff Melrose are now classified as either delinquent or troubled debt. This would suggest recent vintage taxi medallion loans could account for the bulk of the delinquencies and trouble debt restructurings.

For example, Melrose's Call Reports state that the credit union made almost 2,000 member business loans worth almost $878 million in 2013 and approximately 1302 member business loans worth almost $600 million in 2014. Presumably, most of these loans were for taxi medallions.

This information would suggest delinquencies and troubled debt restructurings are only going to go higher.

The following link to an article about the lawsuit has a link to the complaint. Read the article.

Friday, November 20, 2015

Helping Other People Excel FCU Closed

The National Credit Union Administration liquidated Helping Other People Excel Federal Credit Union of Jackson, New Jersey.

NCUA placed Helping Other People Excel Federal Credit Union into conservatorship on Oct. 16. The agency made the decision to liquidate the credit union and discontinue operations after determining it was insolvent and had no prospect for restoring viable operations.

Helping Other People Excel Federal Credit Union served 110 members and had assets of $626,529, according to the credit union’s most recent Call Report.

Helping Other People Excel Federal Credit Union is the 8th federally insured credit union liquidation in 2015.

Read the press release.

NCUA placed Helping Other People Excel Federal Credit Union into conservatorship on Oct. 16. The agency made the decision to liquidate the credit union and discontinue operations after determining it was insolvent and had no prospect for restoring viable operations.

Helping Other People Excel Federal Credit Union served 110 members and had assets of $626,529, according to the credit union’s most recent Call Report.

Helping Other People Excel Federal Credit Union is the 8th federally insured credit union liquidation in 2015.

Read the press release.

Thursday, November 19, 2015

CUs, Albeit Small Players in SBA Lending, Will See More SBA Lending in the Future

An article in The American Banker (subscription required) pointed out that although credit unions are originating a small percentage of Small Business Administration (SBA) 7(a) loans today, credit unions are expected to step up their 7(a) lending efforts in the future.

According to the article, "the volume of SBA loans originated by credit unions reached a record $369 million in the fiscal year that ended Sept. 30, credit unions' share of the overall 7(a) market remained stuck at 1.6%."

However, the article noted that 7(a) lending by credit unions was up 23% in fiscal year 2015 from the previous year and 38% from two years earlier.

Moreover, 7(a) lending by credit unions should grow going forward. Earlier this year, the SBA signed a memorandum of agreement with the National Credit Union Administration promising guidance and support for credit unions interested in the 7(a) program.

In addition, there is a strong incentive for credit unions to make SBA loans, as these loans do not count against the aggregate member business loan cap of 12.25 percent.

According to the article, "the volume of SBA loans originated by credit unions reached a record $369 million in the fiscal year that ended Sept. 30, credit unions' share of the overall 7(a) market remained stuck at 1.6%."

However, the article noted that 7(a) lending by credit unions was up 23% in fiscal year 2015 from the previous year and 38% from two years earlier.

Moreover, 7(a) lending by credit unions should grow going forward. Earlier this year, the SBA signed a memorandum of agreement with the National Credit Union Administration promising guidance and support for credit unions interested in the 7(a) program.

In addition, there is a strong incentive for credit unions to make SBA loans, as these loans do not count against the aggregate member business loan cap of 12.25 percent.

NCUA Board Approves Bank Merger into a Credit Unionr

The National Credit Union Administration (NCUA) Board yesterday in a closed door meeting approved a bank merger into a credit union.

According to a reliable source, the NCUA Board approved the merger of Calusa Bank (Punta Gorda, FL) into Achieva Credit Union (Dunedin, FL).

According to a reliable source, the NCUA Board approved the merger of Calusa Bank (Punta Gorda, FL) into Achieva Credit Union (Dunedin, FL).

Wednesday, November 18, 2015

Customer Satisfaction with CUs Tumbles, As Membership Grows

The American Customer Satisfaction Index reported that consumer satisfaction with credit unions tumbled in 2015 compared to a year ago as the growth in new members strained credit union resources.

Customer satisfaction with credit unions declined by 4.7 percent to 81, and their edge over smaller banks (80) shrinks to a virtual tie.

Compared to 2014, credit unions scored lower in all customer experience categories except for the number of ATM locations.

Credit unions receive their best marks for staff courtesy (90) and transaction speed (89), although both are down from very high scores of 93 in 2014.

Credit union call centers are showing signs of strain as satisfaction fell from 90 in 2014 to 85 in 2015.

Satisfaction with credit union websites slipped from 89 to 86.

Credit union members assigned a lower scores to the variety of financial services available (down from 87 to 84), ease of adding or making changes to accounts (down from 87 to 83), and ease of understanding information about accounts (down from 86 to 82).

Members continue to believe that their credit union offers competitive interest rates (80), although not quite as competitive as in 2014 (84).

The report found that despite a general deterioration in service over the past year, credit unions go nearly head-to-head with smaller regional and community banks for most customer experience elements. While the two are deadlocked for website satisfaction, credit unions receive a higher mark for call centers. The report found that regional and community banks edge past credit unions in four areas: service variety, account changes, account information, and ATM locations.

Compared with national banks and super regional banks, credit unions earn superior satisfaction scores in all but two areas -- the number and location of branches and ATMs.

The report noted that the influx of new members had put pressure on credit unions with regard to customer service and credit unions are struggling to maintain their historically high satisfaction levels.

Read the press release.

Customer satisfaction with credit unions declined by 4.7 percent to 81, and their edge over smaller banks (80) shrinks to a virtual tie.

Compared to 2014, credit unions scored lower in all customer experience categories except for the number of ATM locations.

Credit unions receive their best marks for staff courtesy (90) and transaction speed (89), although both are down from very high scores of 93 in 2014.

Credit union call centers are showing signs of strain as satisfaction fell from 90 in 2014 to 85 in 2015.

Satisfaction with credit union websites slipped from 89 to 86.

Credit union members assigned a lower scores to the variety of financial services available (down from 87 to 84), ease of adding or making changes to accounts (down from 87 to 83), and ease of understanding information about accounts (down from 86 to 82).

Members continue to believe that their credit union offers competitive interest rates (80), although not quite as competitive as in 2014 (84).

The report found that despite a general deterioration in service over the past year, credit unions go nearly head-to-head with smaller regional and community banks for most customer experience elements. While the two are deadlocked for website satisfaction, credit unions receive a higher mark for call centers. The report found that regional and community banks edge past credit unions in four areas: service variety, account changes, account information, and ATM locations.

Compared with national banks and super regional banks, credit unions earn superior satisfaction scores in all but two areas -- the number and location of branches and ATMs.

The report noted that the influx of new members had put pressure on credit unions with regard to customer service and credit unions are struggling to maintain their historically high satisfaction levels.

Read the press release.

Tuesday, November 17, 2015

NCUA and ECOA

The National Credit Union Administration (NCUA) has recently chartered credit unions to serve people that belong to certain religious groups and native American tribes.

For example, on August 28, 2015, NCUA's Office of Consumer Protection chartered a federal credit union to serve members and employees of the Redeemed Christian Church of God North America, Inc. NCUA also chartered a federal credit union on July 7 of this year to serve employees, members, synods and member congregations of the Evangelical Lutheran Church in America.

While these two credit unions have a common bond, it is unclear to me how these institutions' common bonds are in compliance with the Equal Credit Opportunity Act (ECOA).