The NCUA Board approved a 2011 Temporary Corporate Credit Union Stabilization Fund (TCCUSF) assessment of 25 basis points of insured shares (deposits) -- at the top of the range estimated last November by the agency. NCUA estimates the assessment will raise $1.956 billion.

The assessment is based upon June 30, 2011 insured shares and is due by September 27.

NCUA acknowledged during the Board meeting that it tapped its $6 billion line of credit from Treasury -- borrowing $3.5 billion in July.

According to analysis by NCUA staff, the 25 basis point assessment will reduce annualized return on assets for credit unions by 21 basis points. NCUA estimates that 811 credit unions that had reported a profit may now experience negative net income for the year with the impact falling disproportionately on smaller credit unions.

Additionally, the assessment will cause 81 credit unions to slip from being well capitalized. Twenty-four credit unions will become undercapitalized and 3 credit unions will become critically undercapitalized with a net worth ratio under 2 percent.

NCUA, also, reported that 2012 assessments for the TCCUSF will be 9 basis points based upon June 2011 insured shares. This will raise approximately $700 million.

NCUA revealed that projected assessments over the remaining life of the TCCUSF are between $1.9 billion and $6.2 billion, based upon projections from Blackrock's model. Credit unions prior to this assessment had already made payments of $1.3 billion to cover TCCUSF expenses.

Furthermore, NCUA does not anticipate a National Credit Union Share Insurance Fund (NCUSIF) premium assessment for this year; but given the more uncertain economic outlook for 2012, NCUA stated that NCUSIF premiums could range from zero to 7 basis points next year.

Read the Board Action memo.

Monday, August 29, 2011

Friday, August 26, 2011

Violating Confidentiality Provisions

On May 27th, I wrote about Visions FCU publishing in its newsletter the names of members, who caused Visions a financial loss, that the credit union was going to expel at a special meeting.

I've obtained a copy of a NCUA letter (see below), not from the person that filed the complaint, that states this practice by Visions does not appear to comply with Part 716 of the Gramm-Leach-Bliley Act and the disclosure of this information in its newsletter appears to represent a violation of the confidentiality provision of the FCU Bylaws.

NCUA stated in its letter that "this is a regulatory compliance violation that will be addressed and corrected in the upcoming 2011 examination."

It seems to me that since this practice has been going on for some time (I wrote about this practice in a 2005 ABA Bankers News column), NCUA should hit Visions with a cease and desist order, which is published on NCUA's website, and a civil money penalty.

Click on images to enlarge.

I've obtained a copy of a NCUA letter (see below), not from the person that filed the complaint, that states this practice by Visions does not appear to comply with Part 716 of the Gramm-Leach-Bliley Act and the disclosure of this information in its newsletter appears to represent a violation of the confidentiality provision of the FCU Bylaws.

NCUA stated in its letter that "this is a regulatory compliance violation that will be addressed and corrected in the upcoming 2011 examination."

It seems to me that since this practice has been going on for some time (I wrote about this practice in a 2005 ABA Bankers News column), NCUA should hit Visions with a cease and desist order, which is published on NCUA's website, and a civil money penalty.

Click on images to enlarge.

Thursday, August 25, 2011

Common Bond and Equal Credit Opportunity Act

The Equal Credit Opportunity Act (ECOA), which became law on March 23, 1976, says that it is illegal to discriminate in any credit transaction on the the basis of race, color, national origin, religion, sex, marital status, or age.

Congress was very specific that it viewed race, color, national origin, religion, sex, marital status, or age as protected classes in our society.

So, this raises an interesting policy question -- should credit union regulators charter a credit union with field of membership which is based solely upon a protected class, such as religion or national origin?

Congress was very specific that it viewed race, color, national origin, religion, sex, marital status, or age as protected classes in our society.

So, this raises an interesting policy question -- should credit union regulators charter a credit union with field of membership which is based solely upon a protected class, such as religion or national origin?

Tuesday, August 23, 2011

CUNA Would Like Former Director Threshold Raised to $100,000

In a letter to the Internal Revenue Service (IRS) regarding the redesign of the Form 990, the Credit Union National Association (CUNA) requested that $10,000 reporting threshold for former directors be increased to $100,000.

Part VII of the Form 990 requires the reporting organization to list any former director who had served in such capacity in the prior five years and received over $10,000 for services provided as a director.

CUNA justifies increasing the reporting threshold because of the recordkeeping burcden on small credit unions. Additionally, CUNA notes that this would create a uniform reporting threshold among all individuals for compensation reporting purposes.

However, raising the threshold to $100,000 would reduce transparency and accountability.

I can understand why CUNA took this position. It is difficult to maintain the fiction that credit union directors are volunteers, especially when some credit unions are providing generous director compensation.

Part VII of the Form 990 requires the reporting organization to list any former director who had served in such capacity in the prior five years and received over $10,000 for services provided as a director.

CUNA justifies increasing the reporting threshold because of the recordkeeping burcden on small credit unions. Additionally, CUNA notes that this would create a uniform reporting threshold among all individuals for compensation reporting purposes.

However, raising the threshold to $100,000 would reduce transparency and accountability.

I can understand why CUNA took this position. It is difficult to maintain the fiction that credit union directors are volunteers, especially when some credit unions are providing generous director compensation.

Thursday, August 18, 2011

Kansas CU Regulator Assumes Control of CU

The Salina Journal is reporting that the board of directors of the Enterprise Credit Union voted earlier this week to transfer control of the credit union to the Kansas Department of Credit Unions.

John Smith, the administrator of the Kansas Department of Credit Unions, said that during the Department’s examination of the credit union, it uncovered some accounting irregularities. The Department decided to engage a public accounting firm to conduct an audit of the credit union’s books.

Enterprise Credit Union has 577 members and $1.8 million in assets.

Read the article.

John Smith, the administrator of the Kansas Department of Credit Unions, said that during the Department’s examination of the credit union, it uncovered some accounting irregularities. The Department decided to engage a public accounting firm to conduct an audit of the credit union’s books.

Enterprise Credit Union has 577 members and $1.8 million in assets.

Read the article.

NCUA Should Let Banks Bid on Problem CUs

Isn't it time that NCUA permit banks to purchase the assets and assume the liabilites of financially troubled or failing credit unions?

The announcement of United Federal Credit Union to purchase substantially all of the assets and assume the deposits of Griffith Savings Bank or last year's purchase of Anchor Bank's branches by Royal Credit Union are examples of this outside of the box thinking.

Both Anchor Bank and Griffith Savings Bank were in financial difficulty and these transactions appear to be in the best interests of their institutions and their communities.

NCUA may want to take a page out of this playbook as the best way for NCUA to handle some problem credit unions, such as A.E.A. FCU and Texans CU, which are currently in conservatorship.

Let's face it -- there are only a couple credit unions that could digest Texans CU.

Allowing banks to bid for failing credit unions would increase the pool of potential merger partners. With more bidders, this could lower the cost to the NCUSIF in resolving these institutions.

As for the rights of the members, I don't think that is an issue.

The equity interest of the members in these financially troubled credit unions have been wiped out. As for the members' voting rights, they no longer exist as NCUA's emergency merger powers can force a merger without a memebership vote and in many cases, NCUA is running the credit union, which includes removing the credit union's board of directors.

I suspect that for such a transaction to take place NCUA will need to amend its thinking that a suitable merger partner is a continuing credit union.

The announcement of United Federal Credit Union to purchase substantially all of the assets and assume the deposits of Griffith Savings Bank or last year's purchase of Anchor Bank's branches by Royal Credit Union are examples of this outside of the box thinking.

Both Anchor Bank and Griffith Savings Bank were in financial difficulty and these transactions appear to be in the best interests of their institutions and their communities.

NCUA may want to take a page out of this playbook as the best way for NCUA to handle some problem credit unions, such as A.E.A. FCU and Texans CU, which are currently in conservatorship.

Let's face it -- there are only a couple credit unions that could digest Texans CU.

Allowing banks to bid for failing credit unions would increase the pool of potential merger partners. With more bidders, this could lower the cost to the NCUSIF in resolving these institutions.

As for the rights of the members, I don't think that is an issue.

The equity interest of the members in these financially troubled credit unions have been wiped out. As for the members' voting rights, they no longer exist as NCUA's emergency merger powers can force a merger without a memebership vote and in many cases, NCUA is running the credit union, which includes removing the credit union's board of directors.

I suspect that for such a transaction to take place NCUA will need to amend its thinking that a suitable merger partner is a continuing credit union.

Tuesday, August 16, 2011

Proposed CUSO Rule Comment

The American Bankers Association today filed a comment letter with NCUA with respect to its proposed credit union service organization (CUSO) regulation.

ABA believes that the proposed rule is an appropriate step given the fact that NCUA does not have the authority to examine third party vendors like other federal banking regulators; but does not go far enough to mitigate the risk to the National Credit Union Share Insurance Fund (NCUSIF).

ABA has concerns about the section of the proposed rule, which allows undercapitalized federally-insured state chartered credit unions (FISCU) to invest in a CUSO to the permissible state limit, does not adequately address safety and soundness concerns and the potential risk to the NCUSIF.

ABA made several points in its letter with regard to the investment limits.

First, some state laws have very high CUSO investments limits. For states with more permissive investment limits, such an investment by a FISCU could represent a significant contingent claim on the net worth of the credit union if the CUSO fails; and thus could pose a significant risk to the credit union and the NCUSIF.

Second, the degree of risk to a FISCU depends on the nature of the services provided by the CUSO. Rather than following a one-size-fits-all state CUSO investment limit for a specific state where the FISCU is chartered, NCUA should set different CUSO investment limits for all undercapitalized credit unions, both federal charters and state charters, based upon the activities of the CUSO.

Third, under NCUA’s prompt corrective action regulations, restricting transactions with and ownership of a CUSO is a discretionary supervisory action, not a mandatory action, with respect to a credit union that is undercapitalized with a net worth ratio below 5 percent. ABA believes that discretionary supervisory action is not sufficient. ABA recommended that NCUA should amend its PCA regulations so that once a credit union becomes significantly undercapitalized there is a presumption of a restriction on investments with CUSOs. And a critically undercapitalized credit union should not be able to engage in any transaction with a CUSO without first receiving an approval from the NCUA.

Read the letter.

ABA believes that the proposed rule is an appropriate step given the fact that NCUA does not have the authority to examine third party vendors like other federal banking regulators; but does not go far enough to mitigate the risk to the National Credit Union Share Insurance Fund (NCUSIF).

ABA has concerns about the section of the proposed rule, which allows undercapitalized federally-insured state chartered credit unions (FISCU) to invest in a CUSO to the permissible state limit, does not adequately address safety and soundness concerns and the potential risk to the NCUSIF.

ABA made several points in its letter with regard to the investment limits.

First, some state laws have very high CUSO investments limits. For states with more permissive investment limits, such an investment by a FISCU could represent a significant contingent claim on the net worth of the credit union if the CUSO fails; and thus could pose a significant risk to the credit union and the NCUSIF.

Second, the degree of risk to a FISCU depends on the nature of the services provided by the CUSO. Rather than following a one-size-fits-all state CUSO investment limit for a specific state where the FISCU is chartered, NCUA should set different CUSO investment limits for all undercapitalized credit unions, both federal charters and state charters, based upon the activities of the CUSO.

Third, under NCUA’s prompt corrective action regulations, restricting transactions with and ownership of a CUSO is a discretionary supervisory action, not a mandatory action, with respect to a credit union that is undercapitalized with a net worth ratio below 5 percent. ABA believes that discretionary supervisory action is not sufficient. ABA recommended that NCUA should amend its PCA regulations so that once a credit union becomes significantly undercapitalized there is a presumption of a restriction on investments with CUSOs. And a critically undercapitalized credit union should not be able to engage in any transaction with a CUSO without first receiving an approval from the NCUA.

Read the letter.

Sunday, August 14, 2011

Privately Insured CU Closed

The California Department of Financial Institutions (DFI) announced that Sacramento District Postal Employees Credit Union (SDPECU) was closed and ordered to be liquidated, citing inadequate capital.

SDPECU was a privately insured, state-chartered credit union based in Sacramento.

According to its June financial report, SDPECU had a net worth ratio of 2.79 percent. The credit union reported a loss of almost $482,000 through the first six months of 2011. In addition, the credit union lost money in calendar years 2008, 2009, and 2010.

The credit union reported $20.5 million in assets and almost $19.9 million in deposits.

American Share Insurance (ASI) was appointed the liquidating agent of SDPECU by the DFI. ASI has arranged the transfer of SDPECU’s member share accounts to Southern California Postal Credit Union.

Read the press release.

SDPECU was a privately insured, state-chartered credit union based in Sacramento.

According to its June financial report, SDPECU had a net worth ratio of 2.79 percent. The credit union reported a loss of almost $482,000 through the first six months of 2011. In addition, the credit union lost money in calendar years 2008, 2009, and 2010.

The credit union reported $20.5 million in assets and almost $19.9 million in deposits.

American Share Insurance (ASI) was appointed the liquidating agent of SDPECU by the DFI. ASI has arranged the transfer of SDPECU’s member share accounts to Southern California Postal Credit Union.

Read the press release.

Thursday, August 11, 2011

Age by Itself Is Not a Common Bond

The American Bankers Association wrote NCUA Chairman Debbie Matz on August 11 about four credit unions that are using a person’s age to qualify the person for credit union membership.

ABA stated in its letter that it is “concerned that, in some cases, membership organizations are being created for the sole purpose of manufacturing an artificial associational bond that will provide cover for an illegal expansion of a credit union’s membership base. That is not consistent with law or precedent.”

ABA pointed out that “age by itself … does not create an affiliation or common interest that is sufficient to support a field of membership at a credit union.”

ABA requested that “NCUA take all appropriate steps … to ensure that organizations or clubs … actually reflect a substantial and genuine affiliation between their members, and are not simply shell organizations designed to facilitate credit union membership.” ABA also asked the agency to explain its rationale for approving such associational bonds based upon age.

The four credit unions identified in the letter are: CP Federal Credit Union, Ascend Federal Credit Union, Security Service Federal Credit Union, and Suncoast Schools Federal Credit Union.

Read the letter.

ABA stated in its letter that it is “concerned that, in some cases, membership organizations are being created for the sole purpose of manufacturing an artificial associational bond that will provide cover for an illegal expansion of a credit union’s membership base. That is not consistent with law or precedent.”

ABA pointed out that “age by itself … does not create an affiliation or common interest that is sufficient to support a field of membership at a credit union.”

ABA requested that “NCUA take all appropriate steps … to ensure that organizations or clubs … actually reflect a substantial and genuine affiliation between their members, and are not simply shell organizations designed to facilitate credit union membership.” ABA also asked the agency to explain its rationale for approving such associational bonds based upon age.

The four credit unions identified in the letter are: CP Federal Credit Union, Ascend Federal Credit Union, Security Service Federal Credit Union, and Suncoast Schools Federal Credit Union.

Read the letter.

Wednesday, August 10, 2011

Oregon CU Is 5 Days Early in Removing Items from Foreclosed Home

Clackamas Community FCU hired a moving company to remove items from a foreclosed home. The problem is that the credit union was five days early.

Some items were put into storage, while others were taken to the dump.

A notice said that the former homeowner had until Friday, August 12 to clear out of the property.

The credit union's attorney denied that any items were taken from the home, despite the evidence to the contrary.

Read the story.

Some items were put into storage, while others were taken to the dump.

A notice said that the former homeowner had until Friday, August 12 to clear out of the property.

The credit union's attorney denied that any items were taken from the home, despite the evidence to the contrary.

Read the story.

Tuesday, August 9, 2011

Bank and CU Trade Groups Urge Senators to Block IRS Nonresident Rule

Bank and credit union trade groups last week urged senators to support legislation (S. 1506) that would prevent the Internal Revenue Service from issuing a proposed rule requiring the annual reporting of deposit interest paid to any nonresident alien individual.

The groups noted that the proposal would provide no financial benefit to the United States, since such interest paid to nonresident aliens is not subject to tax here, but that it could drive away deposits that support economic growth.

“[T]he list of countries with which the U.S. has [income tax] agreements includes a number of decidedly non-democratic regimes with poor records of protecting human rights that cannot be relied upon to observe confidentiality agreements or to limit their use of data to taxation purposes,” the trade groups said in a letter. “Depositors who reside in these regimes may have legitimate reasons for the confidentiality they have come to expect from the U.S. financial system. Disclosure of their foreign financial holdings could put their families and them at risk of political persecution or criminal harm.”

The groups also noted that deposit interest data is already available to other countries on an as-requested basis, and that the IRS proposal, which provides for automatic exchange of the data, “goes further than needed for the purposes of international cooperation.”

The groups signing the letter were the American Bankers Association, Credit Union National Association, Financial Services Roundtable, Independent Community Bankers of America, and National Association of Federal Credit Unions.

The groups noted that the proposal would provide no financial benefit to the United States, since such interest paid to nonresident aliens is not subject to tax here, but that it could drive away deposits that support economic growth.

“[T]he list of countries with which the U.S. has [income tax] agreements includes a number of decidedly non-democratic regimes with poor records of protecting human rights that cannot be relied upon to observe confidentiality agreements or to limit their use of data to taxation purposes,” the trade groups said in a letter. “Depositors who reside in these regimes may have legitimate reasons for the confidentiality they have come to expect from the U.S. financial system. Disclosure of their foreign financial holdings could put their families and them at risk of political persecution or criminal harm.”

The groups also noted that deposit interest data is already available to other countries on an as-requested basis, and that the IRS proposal, which provides for automatic exchange of the data, “goes further than needed for the purposes of international cooperation.”

The groups signing the letter were the American Bankers Association, Credit Union National Association, Financial Services Roundtable, Independent Community Bankers of America, and National Association of Federal Credit Unions.

Monday, August 8, 2011

Goodwill Hunting

A couple weeks ago, there was a good discussion on this blog about capital standards and goodwill (see comments).

Goodwill is an intangible asset, which can arise from a strong brand name, good customer relations, good employee relations and any patents or proprietary technology. In case of business combinations, goodwill is the difference between the market value and book value of the target firm.

However, intangible assets such as goodwill are particularly difficult to turn into cash and can lose value if a financial institution’s overall franchise deteriorates.

When calculating tier-1 capital for a bank, goodwill net of deferred tax liabilities arising from a business combination is subtracted from a bank's equity capital.

But a similar adjustment is not made when calculating the net worth of a credit union. The Federal Credit Union Act defines net worth as "the retained earnings balance of the credit union, as determined under generally accepted accounting principles, together with any amounts that were previously retained earnings of any other credit union with which the credit union has combined."

According to NCUA, federally-insured credit unions reported almost $496 million in goodwill as of the end of the first quarter of 2011. Between March of 2010 and March of 2011, goodwill reported on the books of credit unions grew by 53 percent.

Chartway FCU of Virginia Beach has seen a large increase in its goodwill, which presumably arose from its acquisition of two failed Utah credit unions. At the end of 2009, it did not report any goodwill. As of March 2011, goodwill was almost $49.8 million.

For some credit unions, if you netted out goodwill, there would be a material drop in their level of net worth.

For example, Texans Credit Union, which is in conservatorship, is reporting goodwill of $18.4 million as of March 2011. Goodwill is equal to 56.67 percent of Texans Credit Union's net worth.

There are 14 credit unions where goodwill is at least 10 percent of the credit union's net worth. Five credit unions report goodwill is at least 25 percent of their net worth.

Goodwill is an intangible asset, which can arise from a strong brand name, good customer relations, good employee relations and any patents or proprietary technology. In case of business combinations, goodwill is the difference between the market value and book value of the target firm.

However, intangible assets such as goodwill are particularly difficult to turn into cash and can lose value if a financial institution’s overall franchise deteriorates.

When calculating tier-1 capital for a bank, goodwill net of deferred tax liabilities arising from a business combination is subtracted from a bank's equity capital.

But a similar adjustment is not made when calculating the net worth of a credit union. The Federal Credit Union Act defines net worth as "the retained earnings balance of the credit union, as determined under generally accepted accounting principles, together with any amounts that were previously retained earnings of any other credit union with which the credit union has combined."

According to NCUA, federally-insured credit unions reported almost $496 million in goodwill as of the end of the first quarter of 2011. Between March of 2010 and March of 2011, goodwill reported on the books of credit unions grew by 53 percent.

Chartway FCU of Virginia Beach has seen a large increase in its goodwill, which presumably arose from its acquisition of two failed Utah credit unions. At the end of 2009, it did not report any goodwill. As of March 2011, goodwill was almost $49.8 million.

For some credit unions, if you netted out goodwill, there would be a material drop in their level of net worth.

For example, Texans Credit Union, which is in conservatorship, is reporting goodwill of $18.4 million as of March 2011. Goodwill is equal to 56.67 percent of Texans Credit Union's net worth.

There are 14 credit unions where goodwill is at least 10 percent of the credit union's net worth. Five credit unions report goodwill is at least 25 percent of their net worth.

Saturday, August 6, 2011

Guidance Issued on Debt Downgrade

Federal banking regulators issued joint guidance on S&P's downgrade of U.S debt from AAA to AA+ (see below).

"Earlier today, Standard & Poor’s rating agency lowered the long-term rating of the U.S. government and federal agencies from AAA to AA+. With regard to this action, the federal banking agencies are providing the following guidance to banks, savings associations, credit unions, and bank and savings and loan holding companies (collectively, banking organizations)

For risk-based capital purposes, the risk weights for Treasury securities and other securities issued or guaranteed by the U.S. government, government agencies, and government-sponsored entities will not change. The treatment of Treasury securities and other securities issued or guaranteed by the U.S. government, government agencies, and government-sponsored entities under other federal banking agency regulations, including, for example, the Federal Reserve Board’s Regulation W, will also be unaffected."

Link to press release.

"Earlier today, Standard & Poor’s rating agency lowered the long-term rating of the U.S. government and federal agencies from AAA to AA+. With regard to this action, the federal banking agencies are providing the following guidance to banks, savings associations, credit unions, and bank and savings and loan holding companies (collectively, banking organizations)

For risk-based capital purposes, the risk weights for Treasury securities and other securities issued or guaranteed by the U.S. government, government agencies, and government-sponsored entities will not change. The treatment of Treasury securities and other securities issued or guaranteed by the U.S. government, government agencies, and government-sponsored entities under other federal banking agency regulations, including, for example, the Federal Reserve Board’s Regulation W, will also be unaffected."

Link to press release.

Thursday, August 4, 2011

Greater Norwalk Area CU Under Enforcement Action

Greater Norwalk Area CU (Norwalk, CT) has entered into a consent order with the Connecticut Department of Banking on July 26 for engaging in unsafe and unsound practices.

The order specifies numerous corrective actions that the credit union should undertake.

The consent order states that the credit union will retain qualified management.

The credit union will immediately establish a supervisory committee that meets the requirements specified by law and the supervisory committee is expected to meet at least quarterly while this enforcement action is in effect.

The credit union shall develop a plan to reduce the level of delinquent loans and eliminate from its books, by charge-off or collection, all assets or portions of assets classified “Loss” that have not been previously collected or charged off.

The credit union will put in place a net worth restoration plan that will return the net worth ratio to 7 percent and keep the net worth ratio above 7 percent thereafter.

The consent order also noted that the Board would ensure all credit union employees and Board members underwent Bank Secrecy Act (BSA) training and that a comprehensive and independent review of the BSA program will be conducted.

Read the consent order.

The order specifies numerous corrective actions that the credit union should undertake.

The consent order states that the credit union will retain qualified management.

The credit union will immediately establish a supervisory committee that meets the requirements specified by law and the supervisory committee is expected to meet at least quarterly while this enforcement action is in effect.

The credit union shall develop a plan to reduce the level of delinquent loans and eliminate from its books, by charge-off or collection, all assets or portions of assets classified “Loss” that have not been previously collected or charged off.

The credit union will put in place a net worth restoration plan that will return the net worth ratio to 7 percent and keep the net worth ratio above 7 percent thereafter.

The consent order also noted that the Board would ensure all credit union employees and Board members underwent Bank Secrecy Act (BSA) training and that a comprehensive and independent review of the BSA program will be conducted.

Read the consent order.

Tuesday, August 2, 2011

Voluntary Prepayment Program Scuttled (Updated)

NCUA announced today that it will not move forward with its Voluntary Prepayment of Corporate Stabilization Fund Assessment program.

The agency stated that it needed to receive pledges of $500 million, if it was going to move forward with the program. However, NCUA reported that it received pledges of $369.9 million from 799 credit unions.

On June 29, NCUA raised the minimum pledge threshold from $300 million to $500 million for the program to be implemented.

Read the press release.

The agency stated that it needed to receive pledges of $500 million, if it was going to move forward with the program. However, NCUA reported that it received pledges of $369.9 million from 799 credit unions.

On June 29, NCUA raised the minimum pledge threshold from $300 million to $500 million for the program to be implemented.

Read the press release.

Cowlitz Credit Union Under an Enforcement Order

Cowlitz Credit Union of Longview, Washington is under a consent order with the Washington Department of Financial Institutions. The order became effective on June 6, 2011.

The order seems to target issues related to governance at the credit union.

The order specifies that the credit union board will recruit and appoint qualified members to its Supervisory Committee and will bring the total membership of the Supervisory Committee to at least 3 members.

The board is expected to develop and retain qualified management with 60 days of the signing of the consent order.

The consent order also states that the board needs to increase its participation in the credit union's affairs. This includes meeting at least monthly to assess corrective actions taken to comply with various documents (which have been blacked out).

Read the consent order.

The order seems to target issues related to governance at the credit union.

The order specifies that the credit union board will recruit and appoint qualified members to its Supervisory Committee and will bring the total membership of the Supervisory Committee to at least 3 members.

The board is expected to develop and retain qualified management with 60 days of the signing of the consent order.

The consent order also states that the board needs to increase its participation in the credit union's affairs. This includes meeting at least monthly to assess corrective actions taken to comply with various documents (which have been blacked out).

Read the consent order.

Monday, August 1, 2011

Non-member Deposits and Credit Union Failures

On July 14, I wrote that the NCUA Inspector General's report on the failure of Beehive CU mentioned that high cost non-member deposits may have played a role in its failure.

There are several other credit union failures, where non-member deposits were present, which suggests some linkage between non-member deposits and risk.

For example, HeritageWest FCU reported that non-member deposits went from zero in March 2007 to $52.1 million in March 2009. This expansion in non-member deposits supported rapid asset growth at the credit union with almost half of the credit union's asset growth funded by non-member deposits. At the time HeritageWest was closed, it reported $48 million in non-member deposits, which comprised over 17 percent of its total deposit base.

Norlarco Credit Union had the same pattern as non-member deposits went from zero as of September 2004 and peaked at $37.8 million as of March 2006. Once again, non-member deposits accounted for almost half of the credit union's growth during those 18 months.

At Cal State 9 Credit Union, non-member deposits grew to $48.9 million by June 2007 from zero at the end of 2004. Non-member deposits financed about a quarter of the the credit union's rapid asset growth.

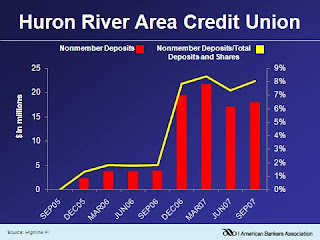

Huron River Area Credit Union also ramped up its holdings of non-member deposits going from zero to $21.7 million in less than 18 months.

This does raise the policy question about whether non-member deposits are a form of hot money fueling rapid asset growth.

If yes, then non-member deposits pose a safety and soundness concern, as rapid growth in non-member deposits can be associated with higher levels of credit risk and liquidity risk.

There are several other credit union failures, where non-member deposits were present, which suggests some linkage between non-member deposits and risk.

For example, HeritageWest FCU reported that non-member deposits went from zero in March 2007 to $52.1 million in March 2009. This expansion in non-member deposits supported rapid asset growth at the credit union with almost half of the credit union's asset growth funded by non-member deposits. At the time HeritageWest was closed, it reported $48 million in non-member deposits, which comprised over 17 percent of its total deposit base.

Norlarco Credit Union had the same pattern as non-member deposits went from zero as of September 2004 and peaked at $37.8 million as of March 2006. Once again, non-member deposits accounted for almost half of the credit union's growth during those 18 months.

At Cal State 9 Credit Union, non-member deposits grew to $48.9 million by June 2007 from zero at the end of 2004. Non-member deposits financed about a quarter of the the credit union's rapid asset growth.

Huron River Area Credit Union also ramped up its holdings of non-member deposits going from zero to $21.7 million in less than 18 months.

This does raise the policy question about whether non-member deposits are a form of hot money fueling rapid asset growth.

If yes, then non-member deposits pose a safety and soundness concern, as rapid growth in non-member deposits can be associated with higher levels of credit risk and liquidity risk.

Subscribe to:

Comments (Atom)