As an economist, I am opposed to price regulation.

I came across an April 4th decision by the Massachusetts Division of Banks setting the maximum allowable fee that state chartered banks and credit unions may charge consumer deposit accounts for processing dishonored checks or deposit returned items for the next year.

Massachusetts State Law authorizes the commissioner of banks to annually establish a reasonable fee that compensates a bank or credit union for the direct cost incurred in processing deposit return items.

To determine the maximum allowable fee, the Division of Banks surveyed 53 banks and credit unionsd regarding the cost of processing deposit returned items. The cost per item ranged from $1.83 to $20.67. The average cost to process a returned item was $6.87 for banks and credit unions (banks had a lower average cost than credit unions), while the median cost of processing a returned item was $5.67.

The Massachusetts Banking Commissioner made the decision to keep the maximum allowable fee unchanged at $5.71 per item for between April 30, 2014 and April 30, 2015.

This decision means that some institutions are going to lose money processing dishonored checks. That is just wrong.

Banks and credit unions should have the freedom to set their prices, not have them dictated by the state.

Read the decision.

Wednesday, April 30, 2014

Monday, April 28, 2014

NCUA Will Not Disclose Stress Test Results

The National Credit Union Administration (NCUA) Board decided on April 24 to not publicize the stress test results for credit unions with $10 billion or more in assets; but stated that they may revisit its decision in three years.

The NCUA Board set forth several arguments against publishing the stress test results.

First, the Board noted that credit unions are cooperatives and not publicly held institutions. So, "the public policy goals of providing information to market participants and facilitating market discipline are of reduced importance in the case of credit unions."

Second, the Board believes that if the stress test results are published, these "results could be taken out of context or misreported in public media. This could lead members to faulty conclusions about their credit union’s current health, and cause a run on deposits."

I believe this concern by the Board is overblown. The Federal Reserve publishes the stress test results for large banks and there have not been any runs. In fact, the evidence would suggest that the disclosure of these results reduced market uncertainty and increased market confidence in these institutions.

Third, NCUA views the stress test as a supervisory tool akin to CAMEL Ratings, which are not published.

Fourth, NCUA is concerned that disclosing the results will put greater pressure on credit unions to always show positive outcomes. The agency worries that credit unions approved by NCUA to conduct their own stress tests after three years would alter their assumptions instead of raise additional capital, which subverts the purpose of the rule.

But shouldn't NCUA review the assumptions and models of these large credit unions to ensure that their assumptions and models are realistic?

In addition, the Board believes that the member and the public have adequate information about the the credit union's performance with the posting of current and past Call Reports on its website. Therefore, there is not need to disclose this stress test results.

However, the Call Report does not tell you the adequacy of the credit union's capital (net worth) under financial stress. I recognize that the stress test is a "what if" analysis; but it can be used by members and future members to assess the financial resiliency of these large credit unions.

I believe NCUA's decision to not publish the stress test results will in the long-run create more uncertainty. People will wonder what is NCUA hiding.

The NCUA Board set forth several arguments against publishing the stress test results.

First, the Board noted that credit unions are cooperatives and not publicly held institutions. So, "the public policy goals of providing information to market participants and facilitating market discipline are of reduced importance in the case of credit unions."

Second, the Board believes that if the stress test results are published, these "results could be taken out of context or misreported in public media. This could lead members to faulty conclusions about their credit union’s current health, and cause a run on deposits."

I believe this concern by the Board is overblown. The Federal Reserve publishes the stress test results for large banks and there have not been any runs. In fact, the evidence would suggest that the disclosure of these results reduced market uncertainty and increased market confidence in these institutions.

Third, NCUA views the stress test as a supervisory tool akin to CAMEL Ratings, which are not published.

Fourth, NCUA is concerned that disclosing the results will put greater pressure on credit unions to always show positive outcomes. The agency worries that credit unions approved by NCUA to conduct their own stress tests after three years would alter their assumptions instead of raise additional capital, which subverts the purpose of the rule.

But shouldn't NCUA review the assumptions and models of these large credit unions to ensure that their assumptions and models are realistic?

In addition, the Board believes that the member and the public have adequate information about the the credit union's performance with the posting of current and past Call Reports on its website. Therefore, there is not need to disclose this stress test results.

However, the Call Report does not tell you the adequacy of the credit union's capital (net worth) under financial stress. I recognize that the stress test is a "what if" analysis; but it can be used by members and future members to assess the financial resiliency of these large credit unions.

I believe NCUA's decision to not publish the stress test results will in the long-run create more uncertainty. People will wonder what is NCUA hiding.

Friday, April 25, 2014

NCUA Proposes to Curb Abusive Associational Common Bond Practices

The National Credit Union Administration (NCUA) Board has issued a proposed rule to amend its associational common bond after aggressive ABA advocacy alerting the agency to numerous associational common bond violations at federal credit unions (FCUs).

NCUA wrote: "In an attempt to expand their potential FOMs beyond appropriate limits, however, a few FCUs have begun forming their own associations and adding independent associations to their FOMs that may not fully satisfy the intent of the associational common bond rules."

The NCUA board has proposed to clamp down on associations formed for the primary purpose of expanding FCU membership. The proposed rule states that "if the association has been formed primarily for the purpose of expanding credit union membership..., then the analysis ends and the association is denied inclusion in the FCU’s FOM."

Also, NCUA is concerned that the current totality of the circumstances test may not be sufficiently filtering out those groups that do not meet the associational common bond requirements. NCUA is expanding the totality of the circumstances test by adding an additional criterion regarding corporate separateness between the associational group and the FCU.

The factors NCUA will consider to establish corporate separateness include:

However, the rule will allow an FCU to pay a member’s associational dues if the member has given consent.

Furthermore, NCUA noted that it is currently reviewing several associations. NCUA stated that "[i]f any of these associations no longer meet the totality of the circumstances test or an association is not operating according to their official bylaws in a way that impermissibly affects credit union membership, NCUA will remove the association from the FCU's FOM."

Read the proposed rule.

NCUA wrote: "In an attempt to expand their potential FOMs beyond appropriate limits, however, a few FCUs have begun forming their own associations and adding independent associations to their FOMs that may not fully satisfy the intent of the associational common bond rules."

The NCUA board has proposed to clamp down on associations formed for the primary purpose of expanding FCU membership. The proposed rule states that "if the association has been formed primarily for the purpose of expanding credit union membership..., then the analysis ends and the association is denied inclusion in the FCU’s FOM."

Also, NCUA is concerned that the current totality of the circumstances test may not be sufficiently filtering out those groups that do not meet the associational common bond requirements. NCUA is expanding the totality of the circumstances test by adding an additional criterion regarding corporate separateness between the associational group and the FCU.

The factors NCUA will consider to establish corporate separateness include:

- Their respective business transactions, accounts, and records are not intermingled;

- Each observes the formalities of its separate corporate procedures;

- Each is adequately financed as a separate entity in light of normal obligations reasonably foreseeable in a business of its size and character;

- Each is held out to the public as a separate enterprise; and

- The group maintains a separate physical location, which does not include a P.O. Box or other mail drop or on premises owned or leased by the FCU.

However, the rule will allow an FCU to pay a member’s associational dues if the member has given consent.

Furthermore, NCUA noted that it is currently reviewing several associations. NCUA stated that "[i]f any of these associations no longer meet the totality of the circumstances test or an association is not operating according to their official bylaws in a way that impermissibly affects credit union membership, NCUA will remove the association from the FCU's FOM."

Read the proposed rule.

Thursday, April 24, 2014

Number of Problem CUs Edges Lower by One to 306

The National Credit Union Administration reported that the number of problem credit unions was largely unchanged during the first quarter of 2014.

The number of problem credit unions fell by one during the quarter to 306 credit unions at the end of the first quarter and is down by 33 credit unions from one year ago.

A problem credit union has a CAMEL rating of 4 or 5.

Problem credit unions held $11.9 billion in deposits (shares), which equals 1.37 percent of the industry’s insured shares.

Assets at problem credit unions at the end of the first quarter were $13.6 billion, which is 1.3 percent of the industry's assets.

The following slide shows the number of problem credit unions and deposits by asset size.

Six credit unions failed during the first quarter of 2014 -- three involuntary mergers and three assisted mergers.

The number of problem credit unions fell by one during the quarter to 306 credit unions at the end of the first quarter and is down by 33 credit unions from one year ago.

A problem credit union has a CAMEL rating of 4 or 5.

Problem credit unions held $11.9 billion in deposits (shares), which equals 1.37 percent of the industry’s insured shares.

Assets at problem credit unions at the end of the first quarter were $13.6 billion, which is 1.3 percent of the industry's assets.

The following slide shows the number of problem credit unions and deposits by asset size.

Six credit unions failed during the first quarter of 2014 -- three involuntary mergers and three assisted mergers.

Wednesday, April 23, 2014

NCUA Offering Consulting Services to Small CUs

NCUA's Office of Small Credit Union Initiatives (OSCUI) provides free consulting services to small credit unions.

OSCUI's website states that consulting services range from operational to strategic management.

In addition, a recent issue of NCUA Report promoted these services in an interview with Bill Myers, Director of OSCUI.

However, I have a real problem with a federal government agency offering free consulting services. I don't believe this is a role for government. Consulting services should be left to the private sector.

Go to the OSCUI website.

OSCUI's website states that consulting services range from operational to strategic management.

"OSCUI’s Consulting Program for operational jobs include budgeting, internal controls, policy development, regulatory compliance, and training of officials and staff. Strategic jobs include developing new products and services, marketing plans, strategic and business plans, field of membership expansion, funding opportunities, and succession planning. Additionally, assistance with Net Worth Restoration Plan (NWRP) or Revised Business Plan (RBP) is offered to small credit unions; plus consulting services to groups wishing to organize a credit union."

In addition, a recent issue of NCUA Report promoted these services in an interview with Bill Myers, Director of OSCUI.

However, I have a real problem with a federal government agency offering free consulting services. I don't believe this is a role for government. Consulting services should be left to the private sector.

Go to the OSCUI website.

Monday, April 21, 2014

Florida CUs Have Highest Complaint Incidence

A report by K. H. Thomas Associates found that two Florida credit unions -- Space Coast and Brightstar -- had the highest Bank Complaint Index (BCI) in Florida.

The report noted that it found it surprising that a growing number of credit unions were in the BCI Top Ten list in recent years, considering that credit unions have a reputation of providing good customer service.

The report found that "[t]wo of the highest BCIs in 2013, both over 6.0, were from credit unions and three of the four highest BCIs in 2013, all over 1.5, were from credit unions."

The BCI is calculated by dividing the complaint market share by deposit market share.

The report noted that it found it surprising that a growing number of credit unions were in the BCI Top Ten list in recent years, considering that credit unions have a reputation of providing good customer service.

The report found that "[t]wo of the highest BCIs in 2013, both over 6.0, were from credit unions and three of the four highest BCIs in 2013, all over 1.5, were from credit unions."

The BCI is calculated by dividing the complaint market share by deposit market share.

Friday, April 18, 2014

Vystar Credit Union

Vystar Credit Union is a $4.9 billion in assets credit union headquartered in Jacksonville, Florida. The credit union reported net income (profits) of almost $50.2 million and paid NO corporate income taxes.

Wednesday, April 16, 2014

A Disappointing CLF Membership Rate

The National Credit Union Administration (NCUA) is putting its best face on a disappointing Central Liquidity Facility (CLF) report.

NCUA reported that credit union membership in the CLF increased by 69 percent between March 31, 2013 and March 31, 2014 to 218 credit unions and the maximum borrowing base had increased by almost 58 percent to $3.8 billion.

In an April 11 press release NCUA Chairman Debbie Matz said: "It’s most encouraging to see the CLF performing well."

As background, NCUA is requiring all federally-insured credit unions with at least $250 million in assets to establish access to at least one contingent federal liquidity source, either the CLF or the Federal Reserve’s Discount Window, or both by March 31, 2014.

According to year-end data (the most recent available), there were 770 credit unions with at least $250 million in assets. Assuming that all 218 credit unions that are CLF members are $250 million or larger in asset size, this translates into a CLF membership participation rate of credit unions with at least $250 million or more in assets of approximately 28 percent.

However, I suspect the CLF membership rate is even lower among the credit unions with at least $250 million in assets.

Among all credit unions, the CLF membership rate is a paltry 3.33 percent.

This would explain the decision by the NCUA to increase the CLF stock dividend rate from 10 basis points to 25 basis points. A higher stock dividend rate could make CLF membership a little more attractive.

Read the press release.

NCUA reported that credit union membership in the CLF increased by 69 percent between March 31, 2013 and March 31, 2014 to 218 credit unions and the maximum borrowing base had increased by almost 58 percent to $3.8 billion.

In an April 11 press release NCUA Chairman Debbie Matz said: "It’s most encouraging to see the CLF performing well."

As background, NCUA is requiring all federally-insured credit unions with at least $250 million in assets to establish access to at least one contingent federal liquidity source, either the CLF or the Federal Reserve’s Discount Window, or both by March 31, 2014.

According to year-end data (the most recent available), there were 770 credit unions with at least $250 million in assets. Assuming that all 218 credit unions that are CLF members are $250 million or larger in asset size, this translates into a CLF membership participation rate of credit unions with at least $250 million or more in assets of approximately 28 percent.

However, I suspect the CLF membership rate is even lower among the credit unions with at least $250 million in assets.

Among all credit unions, the CLF membership rate is a paltry 3.33 percent.

This would explain the decision by the NCUA to increase the CLF stock dividend rate from 10 basis points to 25 basis points. A higher stock dividend rate could make CLF membership a little more attractive.

Read the press release.

Tuesday, April 15, 2014

Why is NCUA a Voting Member on FSOC?

The Dodd-Frank Act created the Financial Stability Oversight Council (FSOC). FSOC is made up of ten voting members and five nonvoting members.

But should the National Credit Union Administration (NCUA) be a voting member?

A report by the Bipartisan Policy Center to create a more effective regulatory architecture recommended making NCUA a non-voting member on the FSOC.

The report noted that "while it is useful to have representation on the FSOC from the NCUA, it makes little sense for the NCUA to have a vote equal to the Federal Reserve on all matters before the Council, particularly when the NCUA does not oversee a single institution that meets the criteria established by Congress or the FSOC as requiring enhanced supervision due to systemic importance."

The report recommends that "[t]he chair of the NCUA should become a non-voting member. Credit unions are an important part of the U.S. financial system, but they generally are small and do not figure into macro-prudential discussions. To the extent they do, a credit union voice will still be represented on the FSOC, but without a vote."

This recommendation really irked one credit union blogger, who wrote "[t]his is bureaucratese for patting credit unions on the head and sending them to the corner with crayons while the adults do all the important work."

Read the report.

But should the National Credit Union Administration (NCUA) be a voting member?

A report by the Bipartisan Policy Center to create a more effective regulatory architecture recommended making NCUA a non-voting member on the FSOC.

The report noted that "while it is useful to have representation on the FSOC from the NCUA, it makes little sense for the NCUA to have a vote equal to the Federal Reserve on all matters before the Council, particularly when the NCUA does not oversee a single institution that meets the criteria established by Congress or the FSOC as requiring enhanced supervision due to systemic importance."

The report recommends that "[t]he chair of the NCUA should become a non-voting member. Credit unions are an important part of the U.S. financial system, but they generally are small and do not figure into macro-prudential discussions. To the extent they do, a credit union voice will still be represented on the FSOC, but without a vote."

This recommendation really irked one credit union blogger, who wrote "[t]his is bureaucratese for patting credit unions on the head and sending them to the corner with crayons while the adults do all the important work."

Read the report.

Monday, April 14, 2014

Quorum FCU and Select Savers Club

Quorum Federal Credit Union (Purchase, NY) is allowing anyone to join the credit union by simultaneously joining an association, Select Savers Club.

Quorum’s online membership application has the following option “I would like to join the Select Savers Club and become a member of Quorum.”

So, what do we know about Select Savers Club and its relationship to Quorum FCU?

Select Savers Club, Inc. was founded in 2006. To become a member of Select Saver Club, you paid a one-time lifetime fee of $5. Starting in November 2007, members of Select Savers Club were eligible to join Quorum FCU.

However, Select Savers Club appears to be closely connected to Quorum FCU.

Three of Select Savers Club's Board members listed on its website either previously worked for Quorum or are currently employed by Quorum -- Heather Sulca, Marisa Conforti, and Danean Sheil. In addition, three other board members have the same last name as three officers of Quorum FCU -- Diane Slifstein, Kimberly Schade, and Tavis Briechle -- and are probably related to these Quorum officers.

In addition, there is no evidence that Select Savers Club is an active association. The last newsletter on its website is from August 2008 and the last announced membership meeting of the club is for the third quarter of 2008.

According to Guidestar, "[t]his organization has not appeared in IRS records for a number of months and may no longer exist."

So, although the club does not appear to be active or may no longer exist, it is still being used by Quorum to qualify people for memberhip in the credit union, who otherwise are not eligible for credit union membership.

As I have previously stated, the simultaneous signing up of an individual to an association in order to make them eligible for credit union membership contradicts congressional intent that there needs to be a genuine affiliation between credit union members in order for credit unions to fulfill their public mission. Membership in Select Savers Club or any other association needs to be more than the checking of a box on a credit union’s membership application.

Read ABA's letter to NCUA.

Quorum’s online membership application has the following option “I would like to join the Select Savers Club and become a member of Quorum.”

So, what do we know about Select Savers Club and its relationship to Quorum FCU?

Select Savers Club, Inc. was founded in 2006. To become a member of Select Saver Club, you paid a one-time lifetime fee of $5. Starting in November 2007, members of Select Savers Club were eligible to join Quorum FCU.

However, Select Savers Club appears to be closely connected to Quorum FCU.

Three of Select Savers Club's Board members listed on its website either previously worked for Quorum or are currently employed by Quorum -- Heather Sulca, Marisa Conforti, and Danean Sheil. In addition, three other board members have the same last name as three officers of Quorum FCU -- Diane Slifstein, Kimberly Schade, and Tavis Briechle -- and are probably related to these Quorum officers.

In addition, there is no evidence that Select Savers Club is an active association. The last newsletter on its website is from August 2008 and the last announced membership meeting of the club is for the third quarter of 2008.

According to Guidestar, "[t]his organization has not appeared in IRS records for a number of months and may no longer exist."

So, although the club does not appear to be active or may no longer exist, it is still being used by Quorum to qualify people for memberhip in the credit union, who otherwise are not eligible for credit union membership.

As I have previously stated, the simultaneous signing up of an individual to an association in order to make them eligible for credit union membership contradicts congressional intent that there needs to be a genuine affiliation between credit union members in order for credit unions to fulfill their public mission. Membership in Select Savers Club or any other association needs to be more than the checking of a box on a credit union’s membership application.

Read ABA's letter to NCUA.

Saturday, April 12, 2014

Navy FCU Sued Over Debt Collection Practices

Heidi Carroll filed a lawsuit March 12 in Raleigh Circuit Court against Navy Federal Credit Union, citing violations of Consumer Credit and Protection Act, Computer Crime and Abuse Act and Telephone Harassment Statute, as well as infliction of emotional distress and invasion of privacy.

Read the story.

Read the story.

Friday, April 11, 2014

Banks Boast the Highest Deposit Interest Rates

While credit unions on average provide the highest interest rates for all deposit account types, banks boast the highest individual interest rates available today, according to GoBankingRates.

Read more.

Read more.

Thursday, April 10, 2014

NCUA Clarifies Comment on Supplemental Capital and Risk-Based Capital

NCUA's General Counsel Mike McKenna sent a letter on April 9 to House Financial Services Committee Chairman Hensarling (R-TX0 and Ranking Member Waters (D-CA) clarifying the agency's position on supplemental capital as it relates to its risk-based capital proposal.

During the hearing, Rep. Sherman (D-CA) asked NCUA General Counsel Mike McKenna a series of questions regarding the NCUA's risk-based capital proposal, including one about supplemental capital as it relates to the proposed risk-based capital rule. McKenna stated that NCUA might allow credit unions greater access to supplemental capital as it finalizes the proposed rule.

In the letter, McKenna notes that NCUA has very little authority to establish supplemental or secondary capital for credit unions unless Congress changes the definition of net worth. McKenna states that with the exception of low-income credit unions net worth is limited to retained earnings as defined by generally accepted accounting principles.

McKenna wrote that NCUA will allow low-income credit unions to count supplemental capital as net worth for the purpose of calculating the credit union's risk-based capital ratio.

Below is the letter.

During the hearing, Rep. Sherman (D-CA) asked NCUA General Counsel Mike McKenna a series of questions regarding the NCUA's risk-based capital proposal, including one about supplemental capital as it relates to the proposed risk-based capital rule. McKenna stated that NCUA might allow credit unions greater access to supplemental capital as it finalizes the proposed rule.

In the letter, McKenna notes that NCUA has very little authority to establish supplemental or secondary capital for credit unions unless Congress changes the definition of net worth. McKenna states that with the exception of low-income credit unions net worth is limited to retained earnings as defined by generally accepted accounting principles.

McKenna wrote that NCUA will allow low-income credit unions to count supplemental capital as net worth for the purpose of calculating the credit union's risk-based capital ratio.

Below is the letter.

Wednesday, April 9, 2014

IRS UBIT Guidance

The Internal Revenue Service (IRS) issued guidance to Exempt Organization examiners stating that certain products offered by state-chartered credit unions will now be exempt from unrelated business income tax (UBIT).

The guidance arose from two district court decisions that held that activities the IRS has previously regarded as subject to UBIT should not be subject to UBIT. The government decided against appealing the decisions.

The following products will not be subject to UBIT.

Finally, the IRS states: "Unless there is a royalty arrangement (rather than payments for a credit union’s services), treat all other insurance products including accidental death and dismemberment insurance as generally subject to UBIT.

The guidance arose from two district court decisions that held that activities the IRS has previously regarded as subject to UBIT should not be subject to UBIT. The government decided against appealing the decisions.

The following products will not be subject to UBIT.

- Sale of checks/fees from a check printing company

- Debit card program’s interchange fees

- Credit card program’s interchange fees

- Interest from credit card loans

- Sale of collateral protection insurance

- Automobile warranties

- Dental insurance

- Cancer insurance

- Accidental death and dismemberment insurance

- Life insurance

- Health insurance

- ATM “per-transaction” fees from nonmembers

Finally, the IRS states: "Unless there is a royalty arrangement (rather than payments for a credit union’s services), treat all other insurance products including accidental death and dismemberment insurance as generally subject to UBIT.

Buying Banks

In the last couple of years, four banks have been bought by credit unions and a fifth transaction is in process.

Mike Bell, a lawyer that represented at least one credit union that acquired a bank, has written two columns on the subject for Credit Union Executive Society.

The first column, Buying a Bank, looked at a three part litmus test that any credit union needs to address before buying a bank -- safety and soundness, impermissible assets, and field of membership issues.

The second column, Why Aren't You Buying a Bank?, points out that regulators are becoming more comfortable with these transactions. He points out such a transaction would add positive cash flow to a credit union's bottomline from day one, would potentially expand its geographic footprint, and would provide an opportunity to acquire talent, especially in the business lending area.

As I have stated previously, I have no objection to credit unions buying banks; but it should be a two way street. Banks should be able to buy credit unions.

However, I believe the leadership at NCUA has a problem with a bank buying a credit union. In the past, NCUA leadership has openly stated that the best charter for consumers is a credit union charter. Such comments pre-judge the process and raise regulatory hurdles to such transactions.

One last point I would like to make -- if Mike Bell's premise is correct that more credit unions will buy banks, this should cause policymakers to revisit the credit union tax exemption, as the tax exempt sector acquires more taxpaying entities.

Mike Bell, a lawyer that represented at least one credit union that acquired a bank, has written two columns on the subject for Credit Union Executive Society.

The first column, Buying a Bank, looked at a three part litmus test that any credit union needs to address before buying a bank -- safety and soundness, impermissible assets, and field of membership issues.

The second column, Why Aren't You Buying a Bank?, points out that regulators are becoming more comfortable with these transactions. He points out such a transaction would add positive cash flow to a credit union's bottomline from day one, would potentially expand its geographic footprint, and would provide an opportunity to acquire talent, especially in the business lending area.

As I have stated previously, I have no objection to credit unions buying banks; but it should be a two way street. Banks should be able to buy credit unions.

However, I believe the leadership at NCUA has a problem with a bank buying a credit union. In the past, NCUA leadership has openly stated that the best charter for consumers is a credit union charter. Such comments pre-judge the process and raise regulatory hurdles to such transactions.

One last point I would like to make -- if Mike Bell's premise is correct that more credit unions will buy banks, this should cause policymakers to revisit the credit union tax exemption, as the tax exempt sector acquires more taxpaying entities.

Tuesday, April 8, 2014

NCUA Can Immediately Take Action on Charter Choice and Disclosure

ABA submitted a Statement for the Record for an April 8, 2014 hearing before the House Financial Services Committee.

While the majority of ABA's Statement for the Record addresses a number of regulatory issues ranging from bank examinations to the new mortgage rules, it also focused on two issues that the National Credit Union Administration could immediately address -- charter choice and disclosure.

On the issue of charter choice, ABA wrote:

With regard to transparency, ABA wrote:

Read the full Statement for the Record.

While the majority of ABA's Statement for the Record addresses a number of regulatory issues ranging from bank examinations to the new mortgage rules, it also focused on two issues that the National Credit Union Administration could immediately address -- charter choice and disclosure.

On the issue of charter choice, ABA wrote:

Many credit unions today have determined to mirror everything a bank does and the National Credit Union Administration (NCUA) seems anxious to accommodate those desires rather than protecting the expansion of the credit union subsidy paid by taxpayers and ensuring it is appropriately directed. If credit unions want to act like banks, there should be a simple, fair and workable path to convert to a mutual bank charter—a process that NCUA has thwarted at every turn. The process must be straightforward and predictable, without NCUA’s patronizing proposition that credit union members do not understand their ownership rights and interests in a conversion—and if they did, would never vote for a conversion. This is NCUA protecting its turf and not protecting taxpayers.

With regard to transparency, ABA wrote:

Most tax-exempt organizations, including universities and hospitals, must disclose the compensation of senior officials to the Internal Revenue Service in the Form 990—a form that has become an important tool for determining the transparency and accountability of tax-exempt organizations. By publicly disclosing this information, the Form 990 fosters good corporate governance as it attempts to ensure that the tax expenditure is being appropriately employed.

Federal credit unions should be required to file Form 990 information return or its equivalent just like state-chartered credit unions and most other tax-exempt institutions. These are actions that can and should be done by NCUA today. Expanding the public’s opportunities to review executive salaries would promote improved corporate governance and greater credit union accountability. It would inform Congress, taxpayers, and credit union members about whether this valuable tax subsidy is going towards the credit union mission or is subsidizing credit union management.

Read the full Statement for the Record.

Monday, April 7, 2014

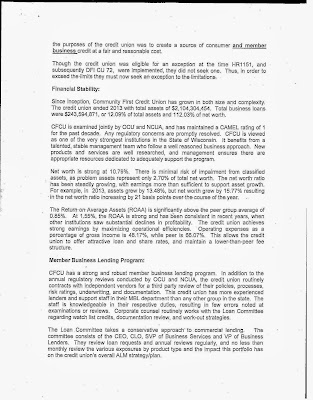

Community First CU's MBL Exception

On February 26, 2014, the Wisconsin Office of Credit Unions (OCU) approved an exception to the aggregate member business loan (MBL) limit for Community First CU in Appleton, Wisconsin. OCU will now permit Community First CU to make member business loans up to 18 percent of the credit union's assets, instead of 12.25 percent of assets.

According to Wisconsin's Credit Union Regulations, credit unions can be granted an exception to the aggregate member business loan cap for three reasons.

(1) Credit unions that have a low-income designation.

(2) Credit unions that participate in the Community Development Financial Institutions program.

(3) Credit unions that are chartered for the purpose of making member business loans, as supported by documentary evidence.

Examples of supporting documentary evidence include the credit union's charter, bylaws, business plan, field of membership, board minutes and loan portfolio.

However, the field examiner cited a fourth rationale for granting an exception -- credit unions that have a history of granting member business loans -- although this is not explicitly part of the code.

The analysis by the OCU notes that the original bylaws did not include references to business loans. It was not until 2012 did the membership vote to amend its bylaws to state that the purpose of the credit union was to create a source of consumer and business credit. But amending its bylaws in 2012 should not retroactively apply to the credit unions origins in 1975.

The analyst looking at the credit union's history cites that the credit union opened its first business savings account in 1975, followed by a loan to a sole proprietor. But the analysis also notes that business lending was not an important part of the credit unions strategy until the early 1990s. However, the conclusion that business lending was an important part of the credit union's strategy seems like a stretch. Call report data from 1989 to 1998 show that member business loans ranged between a low of 2.62 percent of assets and a high of 5.33 percent of assets.

The analyst further states that the credit union was eligible for the exception at the time the Credit Union Membership Access Act (H.R. 1151) was enacted and when the state implemented its business lending regulations; but the credit union did not seek the exception.

In my personal opinion, I do not believe there is sufficient documentary evidence to to claim that Community First was eligible for an exception when HR 1151 was enacted.

Below is the analysis by the OCU along with the approval letter.

According to Wisconsin's Credit Union Regulations, credit unions can be granted an exception to the aggregate member business loan cap for three reasons.

(1) Credit unions that have a low-income designation.

(2) Credit unions that participate in the Community Development Financial Institutions program.

(3) Credit unions that are chartered for the purpose of making member business loans, as supported by documentary evidence.

Examples of supporting documentary evidence include the credit union's charter, bylaws, business plan, field of membership, board minutes and loan portfolio.

However, the field examiner cited a fourth rationale for granting an exception -- credit unions that have a history of granting member business loans -- although this is not explicitly part of the code.

The analysis by the OCU notes that the original bylaws did not include references to business loans. It was not until 2012 did the membership vote to amend its bylaws to state that the purpose of the credit union was to create a source of consumer and business credit. But amending its bylaws in 2012 should not retroactively apply to the credit unions origins in 1975.

The analyst looking at the credit union's history cites that the credit union opened its first business savings account in 1975, followed by a loan to a sole proprietor. But the analysis also notes that business lending was not an important part of the credit unions strategy until the early 1990s. However, the conclusion that business lending was an important part of the credit union's strategy seems like a stretch. Call report data from 1989 to 1998 show that member business loans ranged between a low of 2.62 percent of assets and a high of 5.33 percent of assets.

The analyst further states that the credit union was eligible for the exception at the time the Credit Union Membership Access Act (H.R. 1151) was enacted and when the state implemented its business lending regulations; but the credit union did not seek the exception.

In my personal opinion, I do not believe there is sufficient documentary evidence to to claim that Community First was eligible for an exception when HR 1151 was enacted.

Below is the analysis by the OCU along with the approval letter.

Friday, April 4, 2014

CU Borrowings from Fed's Discount Window, Q1 2012

The Federal Reserve released information on institutions accessing its discount window during the first quarter of 2012.

The following table provides information on credit unions that borrowed from the discount window. Information in the table includes the date of the loan, when the loan matured, the name of the borrower, how much was borrowed, type of credit, and the interest rate on the borrowing.

All institutions, except one, accessed the primary credit program. Primary credit is a lending program available to depository institutions that are in generally sound financial condition. An institution using the secondary credit program is not eligible to borrow from the primary credit program.

The following table provides information on credit unions that borrowed from the discount window. Information in the table includes the date of the loan, when the loan matured, the name of the borrower, how much was borrowed, type of credit, and the interest rate on the borrowing.

All institutions, except one, accessed the primary credit program. Primary credit is a lending program available to depository institutions that are in generally sound financial condition. An institution using the secondary credit program is not eligible to borrow from the primary credit program.

Thursday, April 3, 2014

Weokie's Troubling Car Loan Ad

I received the following ad about financing or refinancing a car loan through Weokie Credit Union in Oklahoma City (see ad below).

This ad is misleading, if not deceptive.

The ad states that you can defer making a payment for 90 days on this loan. It goes on to say in bold, large font that the 90 days no payment savings is $1,357.62.

However, a person, who choses to defer for 90 days making a payment on this loan, does not save $1,357.62 unless the credit union is making the first three payments on the loan, which I doubt. The member still has to make that payment -- it was just delayed.

Moreover, in the ad's fine print, Weokie states that if you chose to defer payment for 90 days, interest will continue to accrue during this time period. In other words, you even owe more in interest.

In addition, Weokie's ad is making a farce out of the membership requirement. Weokie will pay to open an account for you.

The ad says:

I checked Weokie's website and the minimum deposit to open an account for membership in the credit union is $5. Don't you think that the person can at least deposit $5 into a savings account to become a member.

This ad is misleading, if not deceptive.

The ad states that you can defer making a payment for 90 days on this loan. It goes on to say in bold, large font that the 90 days no payment savings is $1,357.62.

However, a person, who choses to defer for 90 days making a payment on this loan, does not save $1,357.62 unless the credit union is making the first three payments on the loan, which I doubt. The member still has to make that payment -- it was just delayed.

Moreover, in the ad's fine print, Weokie states that if you chose to defer payment for 90 days, interest will continue to accrue during this time period. In other words, you even owe more in interest.

In addition, Weokie's ad is making a farce out of the membership requirement. Weokie will pay to open an account for you.

The ad says:

"Don't have an account? Don't worry...

WEOKIE WILL MAKE YOUR FIRST DEPOSIT INTO A NEW ACCOUNT."

I checked Weokie's website and the minimum deposit to open an account for membership in the credit union is $5. Don't you think that the person can at least deposit $5 into a savings account to become a member.

Wednesday, April 2, 2014

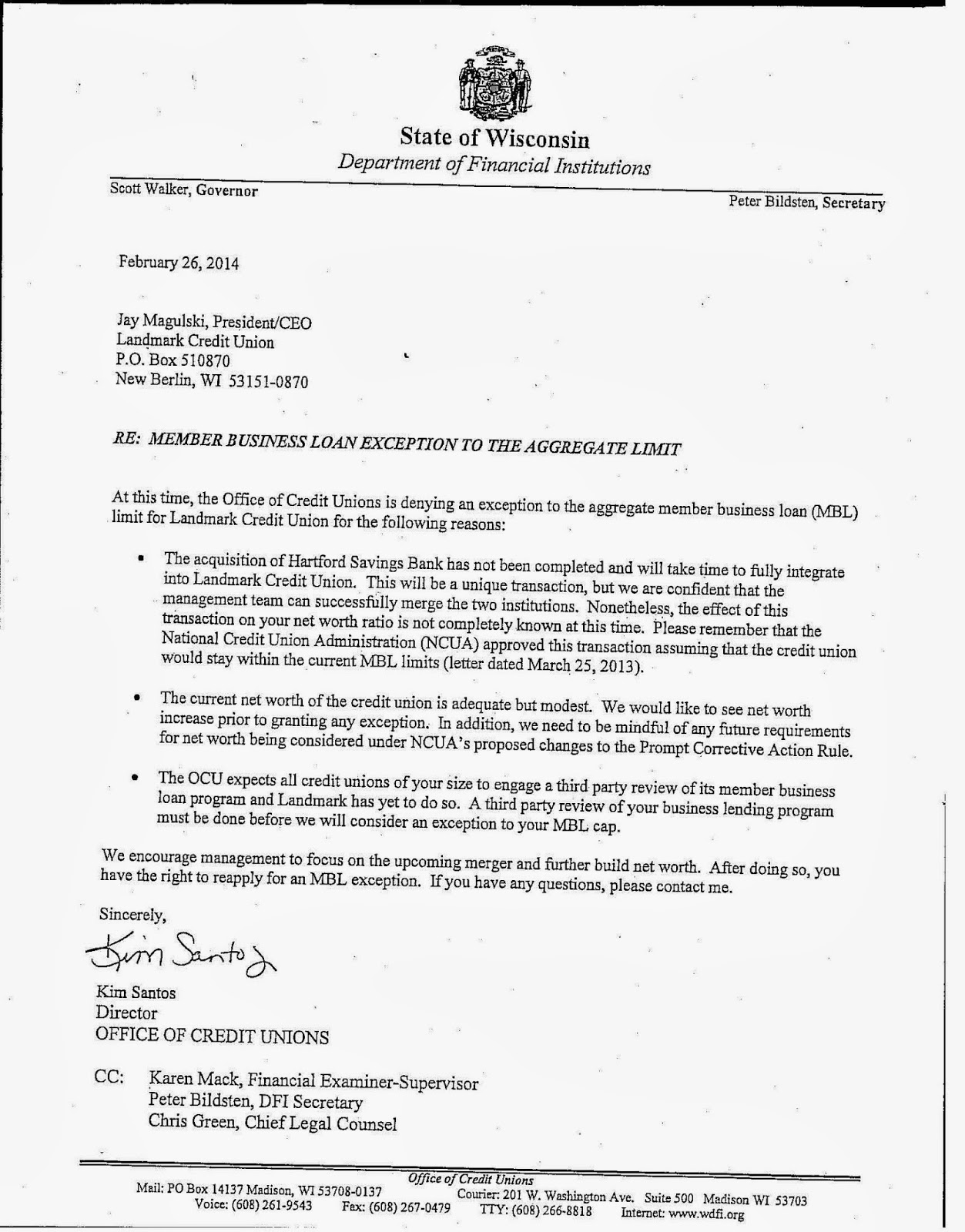

Denial of Landmark MBL Exception Request

Through an Open Records Request with the Wisconsin Office of Credit Unions (OCU), I obtained a copy of the February 26, 2014 letter denying Landmark Credit Union's request for an exception to the aggregate member business loan limit of 12.25 percent of assets.

The OCU cited three reasons for denying the request.

First, the credit union had not completed its acquisition of Hartford Savings Bank. The state regulator noted that it will take time for Hartford Savings Bank to be integrated into Landmark, given the uniqueness of this transaction. Moreover, it was not clear at this time what impact this transaction would have on the credit union's net worth ratio. Furthermore, the OCU pointed out that the National Credit Union Administration approved this acquisition assuming the credit union would stay within its current member business loan limits.

Second, the OCU noted that the credit union's net worth ratio was adequate, but modest. The OCU wanted an increase in net worth before granting an exception to the business loan cap.

Third, OCU wanted a third party review of the credit union's member business loan program and Landmark has not done so. It is an expectation of the OCU that credit unions of Landmark's size engage in a third party review of its business lending program.

The OCU told Landmark to focus on the merger and to build its net worth. The credit union can reapply after doing so.

The OCU cited three reasons for denying the request.

First, the credit union had not completed its acquisition of Hartford Savings Bank. The state regulator noted that it will take time for Hartford Savings Bank to be integrated into Landmark, given the uniqueness of this transaction. Moreover, it was not clear at this time what impact this transaction would have on the credit union's net worth ratio. Furthermore, the OCU pointed out that the National Credit Union Administration approved this acquisition assuming the credit union would stay within its current member business loan limits.

Second, the OCU noted that the credit union's net worth ratio was adequate, but modest. The OCU wanted an increase in net worth before granting an exception to the business loan cap.

Third, OCU wanted a third party review of the credit union's member business loan program and Landmark has not done so. It is an expectation of the OCU that credit unions of Landmark's size engage in a third party review of its business lending program.

The OCU told Landmark to focus on the merger and to build its net worth. The credit union can reapply after doing so.

Tuesday, April 1, 2014

Mayfair FCU Closed, Deposits and Members Assumed by Freedom CU

The National Credit Union Administration (NCUA) liquidated Mayfair Federal Credit Union of Philadelphia. Freedom Credit Union of Warminster, Pa., immediately assumed Mayfair’s members and deposits as well as a portion of the loan portfolio and other assets.

NCUA placed Mayfair into conservatorship on November 1, 2013. NCUA made the subsequent decision to liquidate and discontinue operations after determining the Mayfair was insolvent with no prospect for restoring viable operations.

At the end of 2013, the credit union reported a delinquent loan ratio of 24.80 percent.

At the time of liquidation and subsequent purchase and assumption by Freedom Credit Union, Mayfair served 1,519 members and had assets of $14.3 million, according to the credit union’s most recent Call Report. Chartered in 1936, Mayfair served a low-income community in Philadelphia.

Mayfair Federal Credit Union is the fourth federally insured credit union liquidation in 2014. The last Pennsylvania credit union to fail was People for People CDCU in 2012.

Read the press release.

NCUA placed Mayfair into conservatorship on November 1, 2013. NCUA made the subsequent decision to liquidate and discontinue operations after determining the Mayfair was insolvent with no prospect for restoring viable operations.

At the end of 2013, the credit union reported a delinquent loan ratio of 24.80 percent.

At the time of liquidation and subsequent purchase and assumption by Freedom Credit Union, Mayfair served 1,519 members and had assets of $14.3 million, according to the credit union’s most recent Call Report. Chartered in 1936, Mayfair served a low-income community in Philadelphia.

Mayfair Federal Credit Union is the fourth federally insured credit union liquidation in 2014. The last Pennsylvania credit union to fail was People for People CDCU in 2012.

Read the press release.

Study Questions the Continuation of CU Tax Exemption

A study by PolEcon for the New Hampshire Bankers Association and the Community Bankers Association of New Hampshire found that New Hampshire banks demonstrate a stronger commitment to New Hampshire’s underserved markets than credit unions.

The study noted that New Hampshire (NH) banks are required to pay both Federal income taxes and the NH Business Profits Tax, and also participate in the Community Reinvestment Act (CRA), while credit unions are exempt from all corporate income taxes and do not participate in CRA.

The study found that 44 percent of community bank branches in the state (68 branches) serve New Hampshire’s least wealthy counties, while only 15 percent of credit union branches (14 branches) serve similar areas.

In addition, the study noted that only 25 percent of the credit union tax subsidy is passed-on to depositors and borrowers, and another one-quarter of the tax subsidy is absorbed in higher (than New Hampshire community banks) non-interest expenses of credit unions. The remainder of the subsidy is used to fund credit union expansion.

The corporate income tax exemption provided to credit unions was originally justified as an incentive for credit unions to provide banking services to lower income areas and individuals. However, the study's findings suggest that the original justifications for exempting credit unions from the corporate income tax are no longer appropriate.

Other key findings of the study are:

The study noted that New Hampshire (NH) banks are required to pay both Federal income taxes and the NH Business Profits Tax, and also participate in the Community Reinvestment Act (CRA), while credit unions are exempt from all corporate income taxes and do not participate in CRA.

The study found that 44 percent of community bank branches in the state (68 branches) serve New Hampshire’s least wealthy counties, while only 15 percent of credit union branches (14 branches) serve similar areas.

In addition, the study noted that only 25 percent of the credit union tax subsidy is passed-on to depositors and borrowers, and another one-quarter of the tax subsidy is absorbed in higher (than New Hampshire community banks) non-interest expenses of credit unions. The remainder of the subsidy is used to fund credit union expansion.

The corporate income tax exemption provided to credit unions was originally justified as an incentive for credit unions to provide banking services to lower income areas and individuals. However, the study's findings suggest that the original justifications for exempting credit unions from the corporate income tax are no longer appropriate.

Other key findings of the study are:

- Credit unions are now the largest depository institutions headquartered in the State of New Hampshire and deposits at credit unions are increasingly consolidated in a small number of New Hampshire credit unions.

- New Hampshire credit unions have generally been more profitable than New Hampshire community banks over the past decade, despite having higher expense ratios.

- New Hampshire credit unions are increasingly relying on fee-based income for profitability. Fee-based income at New Hampshire credit unions has risen faster than has fee-based income at New Hampshire community banks.

Subscribe to:

Posts (Atom)