The Credit Union National Association (CUNA) is requesting that Congress permit federal credit unions to reimburse credit union board volunteers for wages they otherwise forfeit by participating in credit union affairs.

CUNA stated that permitting "credit unions to reimburse directors for lost wages resulting from carrying out their board duties would help encourage interest and involvement in credit union boards of directors. Whether or not a volunteer attends a meeting or training session is sometimes determined by whether or not the director will have to miss work and not be paid."

Reimbursing board members for lost wages is the same as paying board members. Once paid, they would no longer be volunteers.

According to my American Heritage College Dictionary, "to volunteer" means to do helpful work without pay.

Monday, April 29, 2013

Thursday, April 25, 2013

CU Discount Window Borrowings , Q1 2011

Fourteen credit unions borrowed from the Federal Reserve's discount window during the first quarter of 2011. The following tables has information on the date of the loan, when the loan matured, the amount borrowed, the amount of collateral and the type of collateral.

Wednesday, April 24, 2013

Navy's 100% LTV Mortgage -- Phenomenal or Ridiculous Product?

The business press is beginning to scrutinize Navy FCU's mortgage practice of providing 100 percent financing without private mortgage insurance.

The latest iteration is an article in the Washington Business Journal (paid subscription).

Katie Miller, VP of mortgage products, says "this product is phenomenal for homebuyers," but Jerry Hanweck, a professor of finance at George Mason University, said "that's ridiculous" and the product "defies the basic rules of good real estate lending."

According to the article, Navy originated $740 million of these 100 percent LTV mortgages in 2012 and two-third of the borrowers were first time home buyers.

The latest iteration is an article in the Washington Business Journal (paid subscription).

"Looking for signs of a housing bubble? Check this out: Vienna-based Navy Federal Credit Union is marketing 100 percent financing, no-money-down mortgages."

Katie Miller, VP of mortgage products, says "this product is phenomenal for homebuyers," but Jerry Hanweck, a professor of finance at George Mason University, said "that's ridiculous" and the product "defies the basic rules of good real estate lending."

According to the article, Navy originated $740 million of these 100 percent LTV mortgages in 2012 and two-third of the borrowers were first time home buyers.

Tuesday, April 23, 2013

Large CUs with the Highest Fee Income

While credit unions have a reputation of charging lower fees, some large credit unions are aggressively relying on fee income for their profits.

According to NCUA's Call Report instructions, fee income is defined as fees charged for services (i.e., overdraft fees, ATM fees, credit card fees, etc.).

At the end of 2012, One Nevada Credit Union reported the highest level of fee income as percent of its average assets at 3.72 percent for credit unions with at least $500 million in assets. Two other credit unions, Denali Alaskan and TwinStar, have fee income as a percent of average assets in excess of 3 percent.

In comparison, for all credit unions with at least $500 million in assets, the median fee income as a percent of average assets was 0.69 percent. Twenty-five percent of all large credit unions have fee income in excess of 0.99 percent of average assets.

The following table ranks the top 50 credit unions in fee income as a percent of average assets. Also, reported in the table is the fee income and the return on average asset for 2012.

According to NCUA's Call Report instructions, fee income is defined as fees charged for services (i.e., overdraft fees, ATM fees, credit card fees, etc.).

At the end of 2012, One Nevada Credit Union reported the highest level of fee income as percent of its average assets at 3.72 percent for credit unions with at least $500 million in assets. Two other credit unions, Denali Alaskan and TwinStar, have fee income as a percent of average assets in excess of 3 percent.

In comparison, for all credit unions with at least $500 million in assets, the median fee income as a percent of average assets was 0.69 percent. Twenty-five percent of all large credit unions have fee income in excess of 0.99 percent of average assets.

The following table ranks the top 50 credit unions in fee income as a percent of average assets. Also, reported in the table is the fee income and the return on average asset for 2012.

Monday, April 22, 2013

HarborOne CU Conversion Update

HarborOne Credit Union today announced that the NCUA Office of Consumer Protection has notified HarborOne that it complied with the procedural requirements of the NCUA’s conversion regulations. HarborOne also received notification from the Massachusetts Division of Banks that it finds no reason to disapprove of the methods by which the membership vote was taken and that the vote is approved. Additionally, HarborOne received notification from the FDIC that its application was officially accepted for processing. HarborOne must wait for approval for FDIC insurance before completing its conversion to a Massachusetts co-operative bank.

Friday, April 19, 2013

Bill Would Exempt Business Loans in Disaster Area from Cap

Representative Maloney (D - NY) introduced legislation that would permit credit unions to make unlimited member business loans in areas impacted by natural disasters.

The Small Business Disaster Relief and Recovery Act (H.R. 1646) will exempt credit union 'member business loans' from the member business loan cap of 12.25 percent of assets for a period of up to five years after a federal natural disaster declaration.

Other sponsors of the legislation are Representatives Grimm (R - NY) and McCarthy (D - NY).

The Small Business Disaster Relief and Recovery Act (H.R. 1646) will exempt credit union 'member business loans' from the member business loan cap of 12.25 percent of assets for a period of up to five years after a federal natural disaster declaration.

Other sponsors of the legislation are Representatives Grimm (R - NY) and McCarthy (D - NY).

Thursday, April 18, 2013

Number of Problem CUs Fell in Q1

The National Credit Union Administration reported that the number of problem credit unions fell by 30 during the first quarter of 2013 to 339.

A problem credit union is defined as having a CAMEL rating of 4 or 5.

According to NCUA, shares (deposits) in problem credit unions were $15 billion as of March 31, 2013. This was down from $16.9 billion, as of the end of 2012. The percent of the industry's insured shares in problem credit unions fell by 23 basis points to 1.79 percent.

Total assets in problem credit unions fell by $2.2 billion to $16.8 billion during the first quarter of 2013.

The following table shows the number of problem credit unions by asset size as of December 31, 2012 and March 31, 2013. (click on image to enlarge)

Wednesday, April 17, 2013

Cybersecurity

Bank and credit union trade groups wrote the House of Representatives yesterday supporting three cybersecurity bills.

The letter concluded by stating:

Read the letter below (click on image to enlarge)

The letter concluded by stating:

"Our nation’s cybersecurity requires the active participation of the government, business and every consumer. We believe these bills encourage the participation of all, while providing the tools to defend against cyber threats by funding research and development activities. The financial services industry is committed to this effort and will remain a willing partner with the Congress and the Administration to secure our nation’s cyber infrastructure."

Read the letter below (click on image to enlarge)

More on Membership Dues

The decision by Arizona FCU to charge a $3 per month membership fee has attracted a lot of attention.

The latest discussion on this topic appears at The Financial Brand, which poses the question should credit unions charge membership dues.

Read The Financial Brand.

The latest discussion on this topic appears at The Financial Brand, which poses the question should credit unions charge membership dues.

Read The Financial Brand.

Tuesday, April 16, 2013

GE Asks for Its Name Back

General Electric has notified three credit unions that include General Electric in their names that they can no longer do so.

According to GoErie.com, attorneys at General Electric asked the credit unions to strip the words "General Electric" from their names.

The three credit unions are: Erie General Electric FCU (Erie, PA), General Electric CU (Cincinnati, OH) and General Electric Employees FCU (Milford, CT).

Erie General Electric Federal Credit Union plans to unveil its new corporate name on Friday, April 19.

Read the story.

According to GoErie.com, attorneys at General Electric asked the credit unions to strip the words "General Electric" from their names.

The three credit unions are: Erie General Electric FCU (Erie, PA), General Electric CU (Cincinnati, OH) and General Electric Employees FCU (Milford, CT).

Erie General Electric Federal Credit Union plans to unveil its new corporate name on Friday, April 19.

Read the story.

Monday, April 15, 2013

CUNA's Whacky Idea

During a hearing on April 10, CUNA floated in its testimony a proposal to raise the de minimus threshold for a business loan to $500,000 and to index it to inflation going forward.

Currently, the de minimus threshold is $50,000. That means the total of all such extensions of credit to a borrower or an associated member less than $50,000 does not count against the member business loan cap of 12.25 percent of assets.

An increase in the de minimus threshold from $50,000 to $500,000 would represent a substantial expansion in the credit union business lending authority. This would significantly free up credit unions to make large commercial loans; because loans under $500,000 would no longer count against the cap. This would further move credit unions away from their mission of meeting the credit needs of consumers, especially those of modest means.

Moreover, raising the threshold would pose a significant safety and soundness risk to the National Credit Union Share Insurance Fund (NCUSIF). These loans would no longer be subject to the National Credit Union Administration's Member Business Loan regulation, because they would no longer be defined as member business loans.

While most people would agree that business loans under $50,000 don't pose a material risk to the NCUSIF, the same cannot be said for loans of $500,000.

Rather than raising the threshold, Congress should eliminate the de minimus member business loan threshold. All business loans made by credit unions should count against the member business loan cap.

Currently, the de minimus threshold is $50,000. That means the total of all such extensions of credit to a borrower or an associated member less than $50,000 does not count against the member business loan cap of 12.25 percent of assets.

An increase in the de minimus threshold from $50,000 to $500,000 would represent a substantial expansion in the credit union business lending authority. This would significantly free up credit unions to make large commercial loans; because loans under $500,000 would no longer count against the cap. This would further move credit unions away from their mission of meeting the credit needs of consumers, especially those of modest means.

Moreover, raising the threshold would pose a significant safety and soundness risk to the National Credit Union Share Insurance Fund (NCUSIF). These loans would no longer be subject to the National Credit Union Administration's Member Business Loan regulation, because they would no longer be defined as member business loans.

While most people would agree that business loans under $50,000 don't pose a material risk to the NCUSIF, the same cannot be said for loans of $500,000.

Rather than raising the threshold, Congress should eliminate the de minimus member business loan threshold. All business loans made by credit unions should count against the member business loan cap.

Saturday, April 13, 2013

Shiloh of Alexandria Federal Credit Union Liquidated

The National Credit Union Administration (NCUA) liquidated Shiloh of Alexandria Federal Credit Union of Alexandria, Va.

NCUA made the decision to liquidate Shiloh of Alexandria Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operations.

The credit union's call report for December 2012 indicated that the credit union was well-capitalized with a net worth ratio of 16.52 percent and profitable. It also reported holding $1.5 million in nonmember deposits.

Shiloh of Alexandria Federal Credit Union served 624 members and had assets of approximately $2.4 million, according to the credit union’s most recent Call Report. Chartered in 1993, Shiloh of Alexandria Federal Credit Union served the members and employees of Shiloh Baptist Church, their immediate family members, and an underserved area within the City of Alexandria, Va.

This is the fifth credit union to be closed by NCUA this year.

Read the press release.

NCUA made the decision to liquidate Shiloh of Alexandria Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operations.

The credit union's call report for December 2012 indicated that the credit union was well-capitalized with a net worth ratio of 16.52 percent and profitable. It also reported holding $1.5 million in nonmember deposits.

Shiloh of Alexandria Federal Credit Union served 624 members and had assets of approximately $2.4 million, according to the credit union’s most recent Call Report. Chartered in 1993, Shiloh of Alexandria Federal Credit Union served the members and employees of Shiloh Baptist Church, their immediate family members, and an underserved area within the City of Alexandria, Va.

This is the fifth credit union to be closed by NCUA this year.

Read the press release.

Thursday, April 11, 2013

Most Profitable Large Credit Unions for 2012

The following tables list the fifty most profitable credit unions with at least $500 million in assets.

Arrowhead Central Credit Union was the most profitable credit union with a return to average assets (ROAA) of 3.66 percent. The next most profitable credit union was Arizona FCU with an ROAA of 3.37 percent (see recent post on the credit union charging a $3 per month membership fee). Rounding out the top five are Rogue FCU, Progressive CU, and Lake Michigan CU. All five credit unions had an ROAA in excess of 3 percent for 2012.

Arrowhead Central Credit Union was the most profitable credit union with a return to average assets (ROAA) of 3.66 percent. The next most profitable credit union was Arizona FCU with an ROAA of 3.37 percent (see recent post on the credit union charging a $3 per month membership fee). Rounding out the top five are Rogue FCU, Progressive CU, and Lake Michigan CU. All five credit unions had an ROAA in excess of 3 percent for 2012.

Wednesday, April 10, 2013

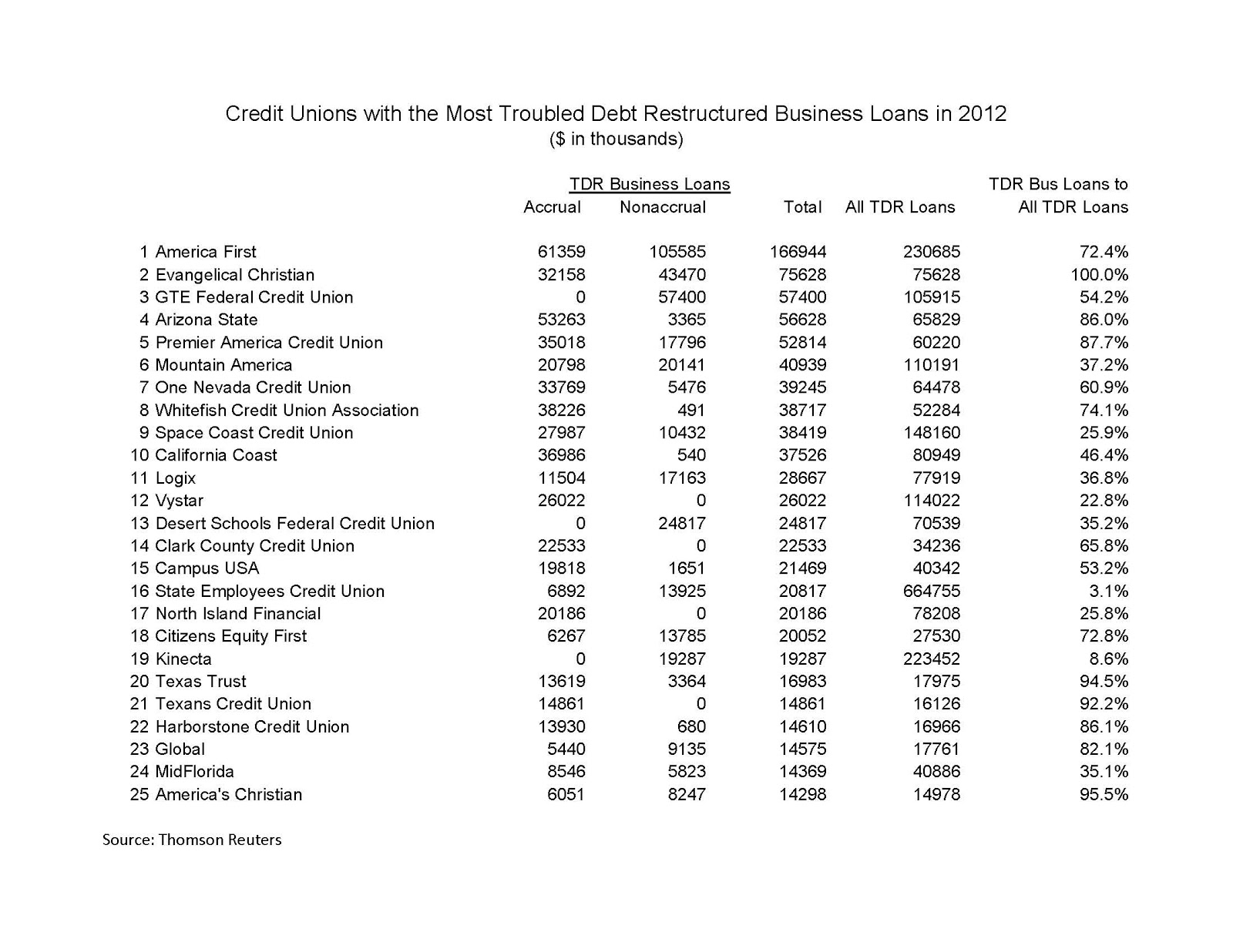

Business Loans -- Troubled Debt Restructuring

Credit unions reported holding $1.8 billion in troubled debt restructured (TDR) business loans at the end of 2012.

Slightly more than $582 million of these troubled debt restructured loans were in nonaccrual status, while almost $1.23 billion of these restructured business loans were in accrual status.

America First Credit Union in Utah had the most TDR business loans at almost $167 million. TDR business loans accounted for 72.4 percent of all TDR loans at the credit union.

In fact, America Fist Credit Union held 9.2 percent of the industry's outstanding TDR business loans; but accounted for slightly more than 18 percent of all nonaccrual TDR business loans.

The five credit unions with the most TDR business loans accounted for 22.6 percent of all TDR business loans; but held 39.1 percent of all TDR business loans in nonaccrual status.

The following table contains information on the 25 credit unions with the most TDR business loans (click on image to enlarge).

Slightly more than $582 million of these troubled debt restructured loans were in nonaccrual status, while almost $1.23 billion of these restructured business loans were in accrual status.

America First Credit Union in Utah had the most TDR business loans at almost $167 million. TDR business loans accounted for 72.4 percent of all TDR loans at the credit union.

In fact, America Fist Credit Union held 9.2 percent of the industry's outstanding TDR business loans; but accounted for slightly more than 18 percent of all nonaccrual TDR business loans.

The five credit unions with the most TDR business loans accounted for 22.6 percent of all TDR business loans; but held 39.1 percent of all TDR business loans in nonaccrual status.

The following table contains information on the 25 credit unions with the most TDR business loans (click on image to enlarge).

Monday, April 8, 2013

Cross-Collateralization Means Proceed with Caution

Fox Business Bankruptcy Adviser wrote "don't fear banks when you file bankruptcy, but you and other readers should know that you need to proceed cautiously with credit unions."

The issue is cross-collateralization clauses, which means all your credit union debt and savings are connected. So if you are late in paying your loan at a credit union, a credit union can take funds out of your checking or savings account.

Read more.

The issue is cross-collateralization clauses, which means all your credit union debt and savings are connected. So if you are late in paying your loan at a credit union, a credit union can take funds out of your checking or savings account.

Read more.

Thursday, April 4, 2013

MECU to Acquire Advance Bank

Municipal Employees Credit Union of Baltimore, Inc. (MECU), and Advance Bank (Advance) signed a definitive Purchase and Assumption agreement under which MECU will acquire substantially all of the assets and assume substantially all of the liabilities of Advance.

Under the terms of the Agreement, MECU will purchase all loans, investments, real estate, accrued interest receivables, and other banking-related assets of Advance and will assume all deposits, Federal Home Loan Bank advances, and accrued interest payable. Advance will be retaining certain assets that will be used to fund certain liabilities that will not be acquired by MECU in the transaction.

MECU represents over 100,000 members, with assets approximately $1.2 billion, and operates nine locations. Advance has total assets of approximately $61 million at December 31, 2012, and operates two locations. Both institutions are mutuals.

This is the fourth transaction involving a credit union acquiring a bank in the last two years.

Read the press release.

Under the terms of the Agreement, MECU will purchase all loans, investments, real estate, accrued interest receivables, and other banking-related assets of Advance and will assume all deposits, Federal Home Loan Bank advances, and accrued interest payable. Advance will be retaining certain assets that will be used to fund certain liabilities that will not be acquired by MECU in the transaction.

MECU represents over 100,000 members, with assets approximately $1.2 billion, and operates nine locations. Advance has total assets of approximately $61 million at December 31, 2012, and operates two locations. Both institutions are mutuals.

This is the fourth transaction involving a credit union acquiring a bank in the last two years.

Read the press release.

Arizona FCU Charging a $3 Monthly Membership Fee

DepositAccount.com is reporting that Arizona FCU is charging members a $3 per month membership fee.

The fee started in January of this year; but is waived for members under age 18 and for Representative Payee accounts. In other words, almost all adult members pay this fee.

I wonder what the Move Your Money crowd thinks about this fee.

The fee started in January of this year; but is waived for members under age 18 and for Representative Payee accounts. In other words, almost all adult members pay this fee.

I wonder what the Move Your Money crowd thinks about this fee.

Wednesday, April 3, 2013

Why So Long?

According to the Material Loss Review (MLR) on Telesis Community Credit Union, the credit union was first identified as a problem institution in September 2007. At that time, its CAMEL composite rating was downgraded to "4". A credit union with a CAMEL 4 rating is designated as a problem institution.

In December 2006, Telesis Community Credit Union had a CAMEL composite rating of "2".

According to a colleague who was a former bank regulator, you usually don't see a two notch downgrade. So, the CAMEL "2" rating was probably a dirty two or alternatively there was a material decline in the credit union's performance.

However, it was not until June 2010 that Telesis Community was subject to a Letter of Understanding and Agreement.

This period of more than 2 1/2 years between first receiving a CAMEL 4 rating and the formal enforcement action seems like a long time.

So, why did it take so long to issue a Letter of Understanding and Agreement to Telesis Community Credit Union?

That is the question that credit union officials, policymakers and the media should be asking credit union regulators.

In December 2006, Telesis Community Credit Union had a CAMEL composite rating of "2".

According to a colleague who was a former bank regulator, you usually don't see a two notch downgrade. So, the CAMEL "2" rating was probably a dirty two or alternatively there was a material decline in the credit union's performance.

However, it was not until June 2010 that Telesis Community was subject to a Letter of Understanding and Agreement.

This period of more than 2 1/2 years between first receiving a CAMEL 4 rating and the formal enforcement action seems like a long time.

So, why did it take so long to issue a Letter of Understanding and Agreement to Telesis Community Credit Union?

That is the question that credit union officials, policymakers and the media should be asking credit union regulators.

Tuesday, April 2, 2013

NCUA Announces Settlement with Bank of America

The National Credit Union Administration (NCUA) announced a settlement with Bank of America and certain of its subsidiaries for $165 million for losses related to purchases of residential mortgage-backed securities by failed corporate credit unions. As part of the settlement, Bank of America did not admit fault.

The settlement with Bank of America follows three similar agreements with Citigroup, Deutsche Bank Securities and HSBC totaling $170.75 million. In total, NCUA has obtained more than $335 million in legal settlements.

Twenty-five percent of the settlement is being paid to the two law firms representing the agency in these legal proceedings.

Read the press release.

The settlement with Bank of America follows three similar agreements with Citigroup, Deutsche Bank Securities and HSBC totaling $170.75 million. In total, NCUA has obtained more than $335 million in legal settlements.

Twenty-five percent of the settlement is being paid to the two law firms representing the agency in these legal proceedings.

Read the press release.

Oregon CUs Can Accept Public Funds In Excess of Deposit Insurance Limit

Yesterday, qualified Oregon credit unions could start accepting public deposits in excess of the federal deposit insurance limit through the Oregon Credit Union Public Funds Collateralization Program.

Legislation passed in 2010 and clarified in 2011 authorized the State Treasury to establish a collateralization program to protect public deposits at credit unions.

Participating institutions protect public deposits above the insured threshold by posting securities as collateral against the uninsured balances.

Ten credit unions will initially participate in the program. The credit unions are Unitus, Pacific Crest, OSU Federal Credit Union, OnPoint, Advantis, MAPS Credit Union, Northwest Community, Old West, Wauna Federal Credit Union, and Oregon Community.

The cities of Portland, Beaverton, Corvallis, Independence, and Klamath Falls have signed letters pledging to deposit funds in excess of $250,000 in one or more of the participating credit unions.

Read the announcement.

Legislation passed in 2010 and clarified in 2011 authorized the State Treasury to establish a collateralization program to protect public deposits at credit unions.

Participating institutions protect public deposits above the insured threshold by posting securities as collateral against the uninsured balances.

Ten credit unions will initially participate in the program. The credit unions are Unitus, Pacific Crest, OSU Federal Credit Union, OnPoint, Advantis, MAPS Credit Union, Northwest Community, Old West, Wauna Federal Credit Union, and Oregon Community.

The cities of Portland, Beaverton, Corvallis, Independence, and Klamath Falls have signed letters pledging to deposit funds in excess of $250,000 in one or more of the participating credit unions.

Read the announcement.

Monday, April 1, 2013

NCUA Explains How to Cook the Net Worth Ratio

The transcript from NCUA's February 20, 2013 webinar has a NCUA staffer telling credit unions how to cook their books to inflate their net worth ratio for Prompt Corrective Action purposes.

The transcript quotes Dominic Carullo, who is an Economic Development Specialist with the Office of Small Credit Union Initiatives, saying:

This is crazy.

It is one thing for NCUA to inform credit unions that they have four options available to them for calculating the denominator of the net worth ratio. It is another thing for NCUA to tell credit unions to use whatever method that puts their net worth ratio in the best light.

In addition, if a credit union can change the method it uses for calculating its net worth ratio every quarter, then it is more difficult to evaluate the capital adequacy of a credit union over time. Consistency in reporting is needed for comparability.

The transcript quotes Dominic Carullo, who is an Economic Development Specialist with the Office of Small Credit Union Initiatives, saying:

"Okay, there are four basic methods available to federally insured credit unions for computing your assets on your quarterly call reports. The first one is using quarter end assets, which is the actual assets at the end of that quarter. There are also three other options. There is the average daily assets over the quarter. There is the average of the three month end balances over the quarter. There is the average of the past four quarter ends."Dominic Carullo goes on to say:

"The credit union has the option of using any one of the four methods and can use whichever denominator gives it the best net worth ratio. You do not need to be consistent from one quarter to the next. The credit union can change the method is [sic] uses for computing the new worth ratio every quarter. If you get a result that does not please you, you can try the other three methods to see if it can give you a better ratio."

This is crazy.

It is one thing for NCUA to inform credit unions that they have four options available to them for calculating the denominator of the net worth ratio. It is another thing for NCUA to tell credit unions to use whatever method that puts their net worth ratio in the best light.

In addition, if a credit union can change the method it uses for calculating its net worth ratio every quarter, then it is more difficult to evaluate the capital adequacy of a credit union over time. Consistency in reporting is needed for comparability.

Subscribe to:

Posts (Atom)