The National Credit Union Administration today liquidated First Hawaiian Homes Federal Credit Union of Hoolehua, Hawaii.

Molokai Community Federal Credit Union of Kaunakakai, Hawaii, immediately assumed First Hawaiian Homes’ assets, member shares and most loans.

NCUA made the decision to liquidate First Hawaiian Homes Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operations.

According to the credit union's third quarter call report (most recent available), the credit union was well-capitalized, reported no problem loans, and was making a small profit.

At the time of liquidation and subsequent assumption by Molokai Community, First Hawaiian Homes served 1,379 members and had assets of nearly $3.2 million, according to the credit union’s most recent Call Report.

First Hawaiian Homes Federal Credit Union is the eleventh federally insured credit union liquidation in 2015.

Read the press release.

Wednesday, December 30, 2015

Large Georgia CU to Defect from Federal Charter

Warner Robins-based Robins Federal Credit Union will change to a state charter on New Year's Day, becoming Robins Financial Credit Union.

The credit union cited that the state charter would give it greater flexibility to expand.

Robins has almost $2.1 billion in assets.

Read the story.

The credit union cited that the state charter would give it greater flexibility to expand.

Robins has almost $2.1 billion in assets.

Read the story.

Tuesday, December 29, 2015

$2 Million Gift Gives USU Credit Union Prime Advertising Space at Utah State University's Stadium

The USU Credit Union, a division of Goldenwest Credit Union, received prime advertising space at Utah State University's stadium for donation.

The credit union has committed $2 million to the football stadium renovation.

As part of the agreement, the south and west concourses of the stadium will carry the USU Credit Union name.

Read more.

The credit union has committed $2 million to the football stadium renovation.

As part of the agreement, the south and west concourses of the stadium will carry the USU Credit Union name.

Read more.

Wednesday, December 23, 2015

Paying CU Directors -- More Acceptable; But Controversial

While credit unions paying their directors is becoming more acceptable, the controversy of paying credit union directors persists, according to a December 23 story in The American Banker.

While federal credit unions cannot pay their directors, state chartered credit unions in a dozen states have the authority to pay their directors and that number should grow over time.

Ben Rogers, research director at Filene Research Institute in Madison, Wisconsin and author of the study on compensating credit union directors, told the American Banker: "I think if we had done the study 10 years ago people would have said compensating directors was absolutely against the ethos of credit unions, but today it is much more acceptable."

According to research by the Filene Research Institute (Filene), 145 credit unions in 12 states pay their board members with directors earning between $60 and $37,597 per year. The study said that in 2012 large credit unions paid four times more than smaller credit unions.

Click on this link to view average director pay by state.

The Filene study pointed out that there is a growing evidence of credit unions using compensation to attract and retain qualified board members given the heighten demands on credit union directors.

However, the article noted that paying directors may have policy implications with regard to the credit union industry's preferential tax treatment, as paying directors further erode the distinction between banks and credit unions.

Read the story (subscription required).

While federal credit unions cannot pay their directors, state chartered credit unions in a dozen states have the authority to pay their directors and that number should grow over time.

Ben Rogers, research director at Filene Research Institute in Madison, Wisconsin and author of the study on compensating credit union directors, told the American Banker: "I think if we had done the study 10 years ago people would have said compensating directors was absolutely against the ethos of credit unions, but today it is much more acceptable."

According to research by the Filene Research Institute (Filene), 145 credit unions in 12 states pay their board members with directors earning between $60 and $37,597 per year. The study said that in 2012 large credit unions paid four times more than smaller credit unions.

Click on this link to view average director pay by state.

The Filene study pointed out that there is a growing evidence of credit unions using compensation to attract and retain qualified board members given the heighten demands on credit union directors.

However, the article noted that paying directors may have policy implications with regard to the credit union industry's preferential tax treatment, as paying directors further erode the distinction between banks and credit unions.

Read the story (subscription required).

Tuesday, December 22, 2015

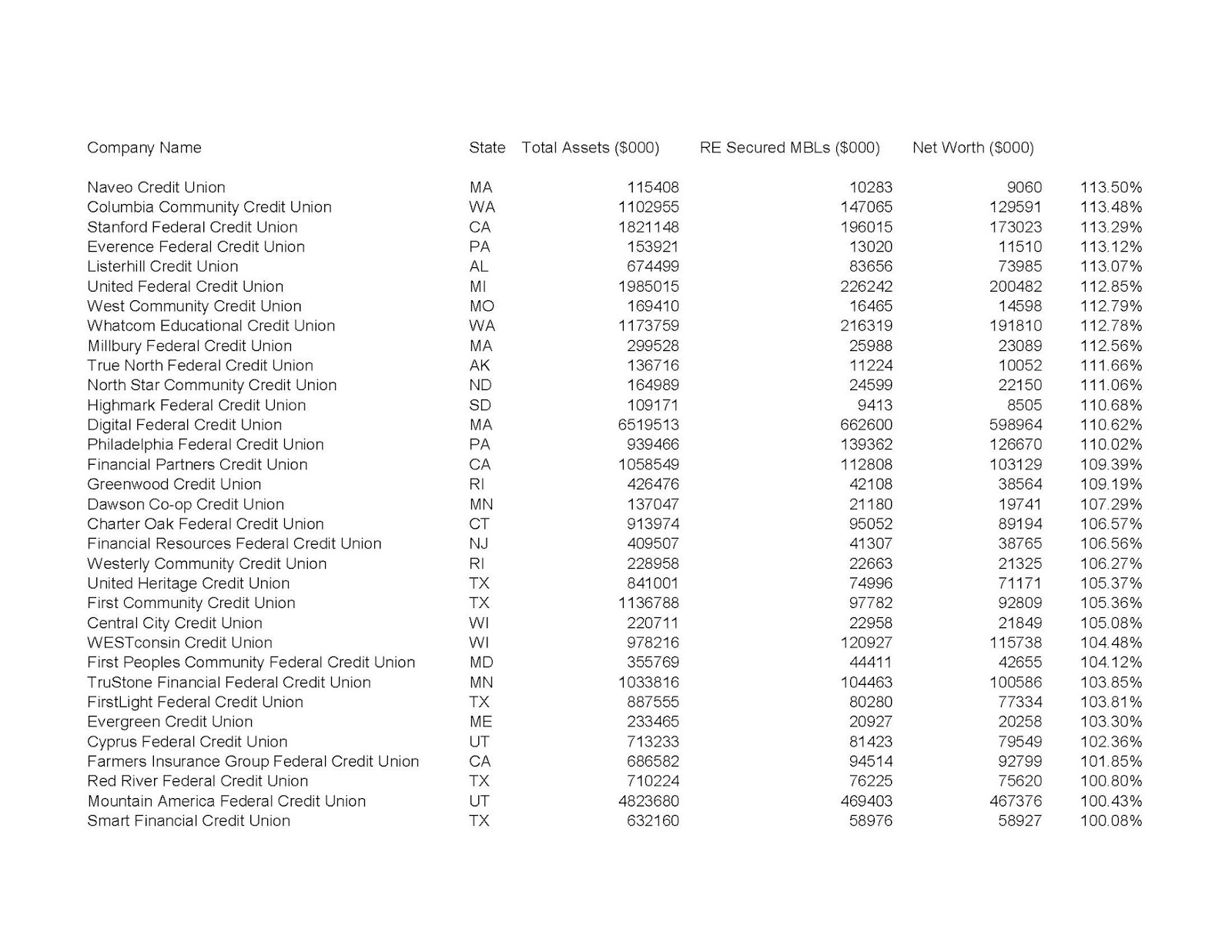

Large CUs' Real Estate Secured Business Loan Exposures

On December 18, the federal banking agencies -- the Federal Deposit Insurance Corporation, the Federal Reserve, and the Office of the Comptroller of the Currency -- issued a statement warning about eased commercial real estate (CRE) loan underwriting and CRE risk management practices that cause “concern.” The federal banking regulators added that supervisors will “continue to pay special attention” to CRE lending in exams in 2016 and reiterated existing interagency guidance on CRE concentration risk.

The National Credit Union Administration did not sign on to this statement; but NCUA may want to sign on to the interagency guidance on CRE concentration risk as real estate secured business loans continue to expand.

There are 105 credit unions with assets of at least $100 million that have an aggregate exposure to real estate secured business loans that exceeds their net worth at the end of the third quarter.

[Editorial note: I know the 105 credit unions include credit unions that have exposure to farmland loans; but the recent weakness in farm commodity prices will likely have a negative impact on farmland values. So, those credit unions making farmland loans also warrant careful monitoring.]

Thirteen credit unions have a real estate secured business loan to net worth ratio above 200 percent and 5 credit unions -- all state charters -- have a real estate secured business loan to net worth ratio in excess of 300 percent.

The two credit unions with the greatest net worth exposure to real estate secured business loans are involved in church financing. Evangelical Christian Credit Union (Brea, CA) has the greatest percentage of its net worth exposed to real estate secured business loans at 907.24 percent. America's Christian Credit Union (Glendora, CA) has the next largest exposure at 532.4 percent.

The following tables provides info on credit unions with real estate secured business loan exposures of at least 100 percent of net worth.

Read the statement.

The National Credit Union Administration did not sign on to this statement; but NCUA may want to sign on to the interagency guidance on CRE concentration risk as real estate secured business loans continue to expand.

There are 105 credit unions with assets of at least $100 million that have an aggregate exposure to real estate secured business loans that exceeds their net worth at the end of the third quarter.

[Editorial note: I know the 105 credit unions include credit unions that have exposure to farmland loans; but the recent weakness in farm commodity prices will likely have a negative impact on farmland values. So, those credit unions making farmland loans also warrant careful monitoring.]

Thirteen credit unions have a real estate secured business loan to net worth ratio above 200 percent and 5 credit unions -- all state charters -- have a real estate secured business loan to net worth ratio in excess of 300 percent.

The two credit unions with the greatest net worth exposure to real estate secured business loans are involved in church financing. Evangelical Christian Credit Union (Brea, CA) has the greatest percentage of its net worth exposed to real estate secured business loans at 907.24 percent. America's Christian Credit Union (Glendora, CA) has the next largest exposure at 532.4 percent.

The following tables provides info on credit unions with real estate secured business loan exposures of at least 100 percent of net worth.

Read the statement.

Friday, December 18, 2015

Bethex FCU Liquidated

The National Credit Union Administration today liquidated Bethex Federal Credit Union of Bronx, New York.

USAlliance Federal Credit Union of Rye, New York, immediately assumed Bethex Federal Credit Union’s assets, member shares and most loans. USAlliance is a federally chartered credit union with a low-income credit union designation that has 83,102 members and assets of $1.07 billion, according to the credit union’s most recent Call Report.

NCUA placed Bethex Federal Credit Union into conservatorship on September 18, 2015. NCUA made the decision to liquidate Bethex and discontinue its operations after determining the credit union was insolvent with no prospect for restoring viable operations on its own.

The credit union reported a loss of $851,367 for the first three quarters of 2015. As of September 30, 13.53 percent of the credit union's loans were 60 days or more past due. On November 18, 2015, the credit union repurchased $502,000 it owed in subordinated debt from the TARP Community Development Capital Initiative.

At the time of liquidation and subsequent purchase by USAlliance, Bethex served 5,824 members and had assets of $12.2 million, according to the credit union’s most recent Call Report.

Bethex Federal Credit Union is the tenth federally insured credit union liquidation in 2015.

Read the press release.

USAlliance Federal Credit Union of Rye, New York, immediately assumed Bethex Federal Credit Union’s assets, member shares and most loans. USAlliance is a federally chartered credit union with a low-income credit union designation that has 83,102 members and assets of $1.07 billion, according to the credit union’s most recent Call Report.

NCUA placed Bethex Federal Credit Union into conservatorship on September 18, 2015. NCUA made the decision to liquidate Bethex and discontinue its operations after determining the credit union was insolvent with no prospect for restoring viable operations on its own.

The credit union reported a loss of $851,367 for the first three quarters of 2015. As of September 30, 13.53 percent of the credit union's loans were 60 days or more past due. On November 18, 2015, the credit union repurchased $502,000 it owed in subordinated debt from the TARP Community Development Capital Initiative.

At the time of liquidation and subsequent purchase by USAlliance, Bethex served 5,824 members and had assets of $12.2 million, according to the credit union’s most recent Call Report.

Bethex Federal Credit Union is the tenth federally insured credit union liquidation in 2015.

Read the press release.

A.E.A. FCU Returned to Its Members

Five years after placing A.E.A. Federal Credit Union of Yuma, Arizona into conservatorship, the National Credit Union Administration returned control of A.E.A. Federal Credit Union to its members.

According to its September 2015 call report, credit union was counting $12.8 million in subordinated debt as net worth, which is highly likely Section 208 assistance from the National Credit Union Share Insurance Fund. Without this section 208 assistance the credit union would be critically undercapitalized.

A.E.A. FCU is the second credit union to emerge from conservatorship this year. The other credit union was Keys FCU (Key West, FL).

Read the story.

According to its September 2015 call report, credit union was counting $12.8 million in subordinated debt as net worth, which is highly likely Section 208 assistance from the National Credit Union Share Insurance Fund. Without this section 208 assistance the credit union would be critically undercapitalized.

A.E.A. FCU is the second credit union to emerge from conservatorship this year. The other credit union was Keys FCU (Key West, FL).

Read the story.

Monterey CU Withdraws Application to Become a Mutual Savings Bank

Silicon Valley Business Journal is reporting that Monterey Credit Union has withdrawn its application to switch to a mutual savings bank charter.

According to Silicon Valley Business Journal, the credit union pulled its application on November 19. This action came 16 months after the credit union's members voted to switch to a bank charter.

The story did not elaborate on why the credit union pulled its application.

Read the story.

According to Silicon Valley Business Journal, the credit union pulled its application on November 19. This action came 16 months after the credit union's members voted to switch to a bank charter.

The story did not elaborate on why the credit union pulled its application.

Read the story.

Wednesday, December 16, 2015

Proposal Would Allow 19.3 Million Vets to Join CUs Serving the Armed Forces

The National Credit Union Administration (NCUA) Board is proposing to include within a credit union’s common bond the honorably discharged veterans of any branch of the United States Armed Forces that is listed in a credit union's charter.

This provision would allow veterans to be eligible for credit union membership beyond their active duty status.

So, this means 19.3 million veterans will have continued access to credit unions that serve various branches of the military.

In justifying its position, the NCUA Board wrote that "[a]ctive duty and discharged military personnel and their families share a similar affinity, typically maintaining a close relationship with their active duty branch of service, largely through Armed Forces associations, publications and continued access to military bases, such as Veterans Administration facilities, base commissaries, post exchanges, and morale, welfare and recreation sponsored programs."

It appears that Navy Federal Credit Union and Pentagon Federal Credit Union wrote this provision, as they will be the beneficiaries of this proposed change to NCUA's field of membership rule.

This provision would allow veterans to be eligible for credit union membership beyond their active duty status.

So, this means 19.3 million veterans will have continued access to credit unions that serve various branches of the military.

In justifying its position, the NCUA Board wrote that "[a]ctive duty and discharged military personnel and their families share a similar affinity, typically maintaining a close relationship with their active duty branch of service, largely through Armed Forces associations, publications and continued access to military bases, such as Veterans Administration facilities, base commissaries, post exchanges, and morale, welfare and recreation sponsored programs."

It appears that Navy Federal Credit Union and Pentagon Federal Credit Union wrote this provision, as they will be the beneficiaries of this proposed change to NCUA's field of membership rule.

Tuesday, December 15, 2015

Credit Union Journal: NCUA Had One 'Whopper Year' On Regulatory Front in 2015

Credit Union Journal wrote that 2015 was a noteworthy year on the regulatory front for the National Credit Union Administration (NCUA).

With the exception of NCUA' controversial risk-based capital rule, which the credit union industry opposed, the agency was active in easing the regulatory burden on credit unions.

NCUA provided regulatory relief to a number of credit unions by doubling the asset threshold size for a small credit union designation to $100 million.

Also, NCUA eliminated its fixed asset rule.

Furthermore, NCUA proposed sweeping changes to its member business lending rule and field of membership regulation, which the agency will likely finalize in 2016.

As I told Credit Union Journal, "Debbie Matz said she was going to [provide relief], and she delivered."

Read the story (subscription required).

With the exception of NCUA' controversial risk-based capital rule, which the credit union industry opposed, the agency was active in easing the regulatory burden on credit unions.

NCUA provided regulatory relief to a number of credit unions by doubling the asset threshold size for a small credit union designation to $100 million.

Also, NCUA eliminated its fixed asset rule.

Furthermore, NCUA proposed sweeping changes to its member business lending rule and field of membership regulation, which the agency will likely finalize in 2016.

As I told Credit Union Journal, "Debbie Matz said she was going to [provide relief], and she delivered."

Read the story (subscription required).

Monday, December 14, 2015

A Majority of CUs Have Fewer Members Compared to a Year Ago

While overall credit union membership continued to grow, more than half of all credit unions have fewer members as of September 30, 2015 compared to a year ago, according to the National Credit Union Administration (NCUA).

Fifty-two percent of federally insured credit unions experienced a year-over-year decline in membership as of the end of the third quarter 2015.

The median rate of growth for credit unions was negative 0.2 percent.

Twenty-three states reported negative median membership growth rate for federally insured credit unions. Federally insured credit unions in Pennsylvania had the lowest median membership growth rate at -2.2 percent.

NCUA noted that membership growth is concentrated in the larger credit unions.

On the other hand, credit unions with falling membership tend to be small. Approximately 75 percent of the credit unions with negative membership growth had less than $50 million in assets.

Read the press release.

Fifty-two percent of federally insured credit unions experienced a year-over-year decline in membership as of the end of the third quarter 2015.

The median rate of growth for credit unions was negative 0.2 percent.

Twenty-three states reported negative median membership growth rate for federally insured credit unions. Federally insured credit unions in Pennsylvania had the lowest median membership growth rate at -2.2 percent.

NCUA noted that membership growth is concentrated in the larger credit unions.

On the other hand, credit unions with falling membership tend to be small. Approximately 75 percent of the credit unions with negative membership growth had less than $50 million in assets.

Read the press release.

Friday, December 11, 2015

Self-Help CU Funds $18 Million Construction Loan for Miami Charter School

The Sports Leadership and Management Academy charter school obtained a $17.97 million construction loan from a North Carolina-based credit union to build its complex in Miami’s Little Havana.

Self-Help Credit Union granted the mortgage to Miami School Group for an 80,552-square-foot school.

The school was co-founded by Christian Perez, also known as recording artist Pitbull.

However, how can a credit union based in Durham, N.C. provide a $18 million construction loan for school in Miami, Florida co-founded by Pitbull?

What is the common bond?

The best guess is a $5 one-time donation to the Center for Community Self Help.

Read the story.

Self-Help Credit Union granted the mortgage to Miami School Group for an 80,552-square-foot school.

The school was co-founded by Christian Perez, also known as recording artist Pitbull.

However, how can a credit union based in Durham, N.C. provide a $18 million construction loan for school in Miami, Florida co-founded by Pitbull?

What is the common bond?

The best guess is a $5 one-time donation to the Center for Community Self Help.

Read the story.

Thursday, December 10, 2015

Morgan Stanley Settles Lawsuit with NCUA over Failed Corporate CUs

The National Credit Union Administration (NCUA) announced a settlement with Morgan Stanley for $225 million to resolve claims arising from losses related to corporate credit unions’ purchases of faulty residential mortgage-backed securities.

The settlement covers claims asserted in 2013 by the NCUA Board on behalf of U.S. Central Federal Credit Union, Western Corporate Federal Credit Union, Members United Corporate Federal Credit Union and Southwest Corporate Federal Credit Union.

NCUA will dismiss pending lawsuits against Morgan Stanley in federal district courts in New York and Kansas. Morgan Stanley does not admit fault in the settlement.

Read the press release.

The settlement covers claims asserted in 2013 by the NCUA Board on behalf of U.S. Central Federal Credit Union, Western Corporate Federal Credit Union, Members United Corporate Federal Credit Union and Southwest Corporate Federal Credit Union.

NCUA will dismiss pending lawsuits against Morgan Stanley in federal district courts in New York and Kansas. Morgan Stanley does not admit fault in the settlement.

Read the press release.

NCUA: Community Charter Can Be a Combined Statistical Area

The National Credit Union Administration (NCUA) Board is proposing to allow a Combined Statistical Area with a population limit of 2.5 million to be treated as a de facto well-defined local community.

According to the Office of Management and Budget (OMB), there are currently 169 Combined Statistical Areas. These Combined Statistical Areas are comprised of 524 Core-based Statistical Areas. A Core-based Statistical Area is either a Metropolitan or Micropolitan Statistical Area.

According to 2013 Census Bureau estimates, only 20 Combined Statistical Areas exceeded the population threshold of 2.5 million.

OMB introduced the concept of Combined Statistical Area in 2000. OMB stated that Combined Statistical Areas can be characterized as representing larger regions that reflect broader social and economic interactions, such as wholesaling, commodity distribution, and weekend recreation activities.

However, two Federal Courts ruled against NCUA in Utah and Pennsylvania, when the agency approved community charters comprised of multiple core-based statistical areas. The Federal Courts wrote that the areas did not meet the requirement of being well-defined local community.

So, how can a larger region represented by a Combined Statistical Area meet the requirement of being a local community?

NCUA is clearly trying to accomplish through the regulatory process what it has not been able to do legislatively.

According to the Office of Management and Budget (OMB), there are currently 169 Combined Statistical Areas. These Combined Statistical Areas are comprised of 524 Core-based Statistical Areas. A Core-based Statistical Area is either a Metropolitan or Micropolitan Statistical Area.

According to 2013 Census Bureau estimates, only 20 Combined Statistical Areas exceeded the population threshold of 2.5 million.

OMB introduced the concept of Combined Statistical Area in 2000. OMB stated that Combined Statistical Areas can be characterized as representing larger regions that reflect broader social and economic interactions, such as wholesaling, commodity distribution, and weekend recreation activities.

However, two Federal Courts ruled against NCUA in Utah and Pennsylvania, when the agency approved community charters comprised of multiple core-based statistical areas. The Federal Courts wrote that the areas did not meet the requirement of being well-defined local community.

So, how can a larger region represented by a Combined Statistical Area meet the requirement of being a local community?

NCUA is clearly trying to accomplish through the regulatory process what it has not been able to do legislatively.

Wednesday, December 9, 2015

San Francisco FCU Unveils 100 Percent LTV Jumbo Mortgages

Citing skyrocketing housing costs, San Francisco Federal Credit Union announced a new loan program that will allow San Francisco-area borrowers to finance up to 100 percent of their mortgage – with no requirement for private mortgage insurance – on loans up to $2 million.

The new loan program is called POPPYLOAN, which stands for Proud Ownership Purchase Program for You.

According to the credit union, POPPYLOAN is available to anyone who works in San Francisco or San Mateo Counties and can be used to purchase a home in the nine Bay Area Counties: San Francisco, San Mateo, Marin, Napa, Sonoma, Santa Clara, Alameda, Contra Costa, or Solano.

To qualify for POPPYLOAN, borrowers must be 18 years or older and purchasing a single family home, townhouse, condominium, or 2-to-4 unit multi-family dwelling as their primary residence. Eligibility for the loan also depends on a number of additional factors, such as credit scores, income, employment status, and property value.

POPPYLOAN is structured as a 5/5 adjustable rate, 30-year mortgage. The interest rate on the mortgage cannot increase by more than 2 percent every five years and no more than 6 percent over the life of the loan.

However, the loan is not available to refinance an existing mortgage.

Read the article.

The new loan program is called POPPYLOAN, which stands for Proud Ownership Purchase Program for You.

According to the credit union, POPPYLOAN is available to anyone who works in San Francisco or San Mateo Counties and can be used to purchase a home in the nine Bay Area Counties: San Francisco, San Mateo, Marin, Napa, Sonoma, Santa Clara, Alameda, Contra Costa, or Solano.

To qualify for POPPYLOAN, borrowers must be 18 years or older and purchasing a single family home, townhouse, condominium, or 2-to-4 unit multi-family dwelling as their primary residence. Eligibility for the loan also depends on a number of additional factors, such as credit scores, income, employment status, and property value.

POPPYLOAN is structured as a 5/5 adjustable rate, 30-year mortgage. The interest rate on the mortgage cannot increase by more than 2 percent every five years and no more than 6 percent over the life of the loan.

However, the loan is not available to refinance an existing mortgage.

Read the article.

Tuesday, December 8, 2015

CUs Received More Than $120 Billion in Emergency Liquidity and Guarantees During Financial Crisis

Testifying before the House Financial Services Committee on December 8, National Credit Union Administration (NCUA) Chairman Debbie Matz provided information about the extraordinary measures that were taken by NCUA to support the credit union system during the financial crisis and Great Recession.

Chairman Matz noted consumer-oriented, member-owned credit union system suffered sizable losses, as a result of the financial crisis. Ninety retail credit unions failed because they were not holding sufficient capital to cover their risks.

Chairman Matz went on to state that the failure of five corporate credit unions had near-catastrophic consequences for all surviving credit unions, causing Congress to create the Temporary Corporate Credit Union Stabilization Fund.

Furthermore, she stated NCUA injected more than $120 billion of emergency liquidity and guarantees to stabilize the credit union system - more than $20 billion in liquidity assistance through the Central Liquidity Facility and over $100 billion in guarantees.

She also pointed out that NCUA borrowed $5 billion from the U.S. Treasury to support the credit union system.

Read the testimony.

Chairman Matz noted consumer-oriented, member-owned credit union system suffered sizable losses, as a result of the financial crisis. Ninety retail credit unions failed because they were not holding sufficient capital to cover their risks.

Chairman Matz went on to state that the failure of five corporate credit unions had near-catastrophic consequences for all surviving credit unions, causing Congress to create the Temporary Corporate Credit Union Stabilization Fund.

Furthermore, she stated NCUA injected more than $120 billion of emergency liquidity and guarantees to stabilize the credit union system - more than $20 billion in liquidity assistance through the Central Liquidity Facility and over $100 billion in guarantees.

She also pointed out that NCUA borrowed $5 billion from the U.S. Treasury to support the credit union system.

Read the testimony.

Monday, December 7, 2015

U.S. Eagle FCU Secures Signage Rights to New Mexico's Tallest Building

The Albuquerque Journal is reporting that U.S. Eagle Federal Credit Union has secured signage rights to New Mexico’s tallest building, the 22-story Albuquerque Plaza in Downtown Albuquerque.

The credit union will also open a branch on the first floor of the building.

The credit union has $855 million in assets as of the end of the third quarter.

The price and terms for the signage rights were not disclosed.

Read the story.

The credit union will also open a branch on the first floor of the building.

The credit union has $855 million in assets as of the end of the third quarter.

The price and terms for the signage rights were not disclosed.

Read the story.

Redlining Minority and Low-Income Communities?

One provision in the National Credit Union Administration (NCUA) Board proposal to amend its field of membership rules could result in the redlining of low-income, minority, and underserved communities.

The NCUA Board is proposing to repeal the "core area" requirement when a federal credit union (FCU) applies for a community charter consisting of a portion of a Core Based Statistical Area.

A Core Based Statistical Area is either a metropolitan statistical area or a micropolitan statistical area.

As background, NCUA's FOM regulation since 20101 requires that when a FCU applies to serve a community consisting of a portion of a Core Based Statistical Area, that portion must include the Core Based Statistical Area’s “core area.” NCUA defines a "core area" as the most populated county or named municipality in the Core Based Statistical Area.

NCUA noted that the primary purpose of this requirement was to acknowledge the core area of a Core Based Statistical Area as the typical focal point for common interests and interaction among residents. An additional purpose was to extend FCU services to low-income persons and underserved areas, both typically located in the "core area" of a Core Based Statistical Area.

NCUA is proposing to repeal this "core area" requirement; because the agency's review of FCU’s business and marketing plans over the last five years show FCUs are adequately serving low-income persons and underserved areas. In place of the "core area" requirement, NCUA proposes to annually review for three years a FCU's progress in implementing its marketing and business plan.

Unfortunately, the repeal of the "core area" requirement could allow FCUs to design community charters that resemble donuts by serving wealthier suburban counties and excluding markets containing low-income and minority communities that reside in the core area.

NCUA should ensure that community charters do not redline low-income, minority, and underserved communities.

The NCUA Board is proposing to repeal the "core area" requirement when a federal credit union (FCU) applies for a community charter consisting of a portion of a Core Based Statistical Area.

A Core Based Statistical Area is either a metropolitan statistical area or a micropolitan statistical area.

As background, NCUA's FOM regulation since 20101 requires that when a FCU applies to serve a community consisting of a portion of a Core Based Statistical Area, that portion must include the Core Based Statistical Area’s “core area.” NCUA defines a "core area" as the most populated county or named municipality in the Core Based Statistical Area.

NCUA noted that the primary purpose of this requirement was to acknowledge the core area of a Core Based Statistical Area as the typical focal point for common interests and interaction among residents. An additional purpose was to extend FCU services to low-income persons and underserved areas, both typically located in the "core area" of a Core Based Statistical Area.

NCUA is proposing to repeal this "core area" requirement; because the agency's review of FCU’s business and marketing plans over the last five years show FCUs are adequately serving low-income persons and underserved areas. In place of the "core area" requirement, NCUA proposes to annually review for three years a FCU's progress in implementing its marketing and business plan.

Unfortunately, the repeal of the "core area" requirement could allow FCUs to design community charters that resemble donuts by serving wealthier suburban counties and excluding markets containing low-income and minority communities that reside in the core area.

NCUA should ensure that community charters do not redline low-income, minority, and underserved communities.

Sunday, December 6, 2015

Privately Insured CUs Can Become Members of FHLBs

Privately insured credit unions can now become members of the Federal Home Loan Banks (FHLBs).

President Obama on December 4 signed into law the Highway Bill (H.R. 22).

Section 82001 of the bill allows privately insured credit unions to join the Federal Home Loan Banks "only if the appropriate supervisor of the State in which the credit union is chartered has determined that the credit union meets all the eligibility requirements for Federal deposit insurance as of the date of the application for membership."

Also, the bill protects FHLB advances from loss by giving FHLBs priority to collateral backing FHLB advances.

This section of the bill also authorizes the GAO to conduct an audit on the adequacy of insurance reserves held by a private

deposit insurer and on the level of compliance with Federal regulations relating to the disclosure of a lack of Federal deposit insurance.

American Share Insurance is the only private insurer of credit unions.

Read the bill.

President Obama on December 4 signed into law the Highway Bill (H.R. 22).

Section 82001 of the bill allows privately insured credit unions to join the Federal Home Loan Banks "only if the appropriate supervisor of the State in which the credit union is chartered has determined that the credit union meets all the eligibility requirements for Federal deposit insurance as of the date of the application for membership."

Also, the bill protects FHLB advances from loss by giving FHLBs priority to collateral backing FHLB advances.

This section of the bill also authorizes the GAO to conduct an audit on the adequacy of insurance reserves held by a private

deposit insurer and on the level of compliance with Federal regulations relating to the disclosure of a lack of Federal deposit insurance.

American Share Insurance is the only private insurer of credit unions.

Read the bill.

Bank and CU Trade Groups File Brief regarding Recent FCC Order

The American Bankers Association, the Credit Union National Association, and the Independent Community Bankers Association filed a friend of the court brief on Wednesday in an appeal of a recent order by the Federal Communications Commission (FCC) regarding the Telephone Consumer Protection Act (FCC).

In that order, the FCC granted four exemptions from the TCPA for data breach and fraud-related calls. However, the FCC also interpreted certain provisions in the TCPA in ways that will make it more difficult for banks and credit unions to send other valuable communications to their customers.

The brief argues that the order “severely restricts the ability of financial institutions and other callers to engage in useful, and often urgent, communications with their customers and members.”

The brief supported the petitions filed by nine industry members seeking a review of the FCC’s order by the D.C. Circuit Court of Appeals.

The brief described the types of messages financial institutions send to their customers and how the FCC’s order will prevent many of these communications from occurring.

Read the brief.

In that order, the FCC granted four exemptions from the TCPA for data breach and fraud-related calls. However, the FCC also interpreted certain provisions in the TCPA in ways that will make it more difficult for banks and credit unions to send other valuable communications to their customers.

The brief argues that the order “severely restricts the ability of financial institutions and other callers to engage in useful, and often urgent, communications with their customers and members.”

The brief supported the petitions filed by nine industry members seeking a review of the FCC’s order by the D.C. Circuit Court of Appeals.

The brief described the types of messages financial institutions send to their customers and how the FCC’s order will prevent many of these communications from occurring.

Read the brief.

Saturday, December 5, 2015

Hiway Federal Credit Union Renews Sponsorship of NHL Team

Hiway Federal Credit Union (St. Paul, MN) has renewed its sponsorship of National Hockey League's Minnesota Wild for two more years.

Hiway Federal Credit Union will be the hockey team's official credit union through the Wild's 2016-2017 season, the St. Paul-based lender said.

The deal, which started last season, includes advertising at St. Paul's Xcel Energy Center, ATMs in the arena, team-branded accounts and cards, and prize drawings and discounts at Hockey Lodge retail locations.

The price of the deal was not disclosed.

Read the story.

Hiway Federal Credit Union will be the hockey team's official credit union through the Wild's 2016-2017 season, the St. Paul-based lender said.

The deal, which started last season, includes advertising at St. Paul's Xcel Energy Center, ATMs in the arena, team-branded accounts and cards, and prize drawings and discounts at Hockey Lodge retail locations.

The price of the deal was not disclosed.

Read the story.

Friday, December 4, 2015

Credit Unions Post Strong Loan Growthn Q3, Delinquencies Up for Second Consecutive Quarter

The National Credit Union Administration (NCUA) is reporting that federally insured credit unions posted strong loan growth during the third quarter.

Total loans at federally insured credit unions reached $769.5 billion in the third quarter of 2015, an increase of 3.3 percent from the previous quarter and 10.7 percent from a year earlier. All major loan categories posted growth during the third quarter -- non-federally guaranteed student loans grew by 5.1 percent; new auto loans were up 4.4 percent; used auto loans rose by 3.7 percent; first mortgage loans and member business loans increased by 3 percent.

The NCUA reported a surge in indirect lending at federally insured credit unions. Indirect loans were $131.5 billion at the end of the third quarter of 2015 and represented 17.09 percent of total industry loans. This is up from approximately $108 billion a year earlier, which accounted for 15.53 percent of all credit union loans.

Overall, share and deposit accounts at federally insured credit unions increased $5.6 billion from the second quarter 2015 and $53.3 billion from the end of the third quarter of 2014 to $992.5 billion.

Because loans grew at a faster rate than shares and deposits, the loan-to-share ratio rose from 75.52 percent at the end of the second quarter to 77.53 percent as of September 30, 2015.

Credit Unions Earned $2.3 Billion in Q3

Federally insured credit unions continued to report positive net income in the third quarter, $2.3 billion, a decline of $82 million, or 3.5 percent, from the third quarter of 2014. As a whole, federally insured credit unions have recorded positive net income for 23 straight quarters.

Year-to-date federally-insured credit union profits were almost $6.9 billion -- up from slightly below $6.8 billion for the same time period of 2014.

Federally insured credit unions’ year-to-date return on average assets ratio stood at an annualized 80 basis points at the end of the third quarter, slightly below the level in the third quarter of 2014. Overall, 78 percent of federally insured credit unions reported positive returns on average assets for the first three quarters of 2015, compared to 76 percent in the first three quarters of 2014.

98 Percent of Credit Unions Were Well-Capitalized

The credit union industry continued to build its net worth during the quarter. The credit union industry's net worth ratio increased by 7 basis points during the third quarter to 10.99 percent.

The percentage of federally insured credit unions that were well-capitalized rose in the third quarter, with 98.0 percent reporting a net worth ratio at or above the statutorily required 7.0 percent. A year earlier, 97.5 percent of credit unions were well-capitalized. As of September 30, 2015, 34 federally insured credit unions were undercapitalized.

Delinquencies Rose for Second Consecutive Quarter

It appears that the credit cycle is turning. Delinquent loans are up for the second consecutive quarter. Loans 60 days or more past due rose by approximately $450 million during the quarter to almost $6 billion and is up by more than $1 billion since March 31, 2015.

In addition, early delinquencies were $6.1 billion at the end of the third quarter, an increase of $456 million from the end of the second quarter.

According to NCUA, delinquency rates edged higher during the quarter, while net charge-off rates unchanged. The delinquency rate at federally insured credit unions rose in the third quarter to 78 basis points, up from 74 basis points the previous quarter, but still below the 85 basis-point level in the third quarter of 2014. The net charge-off ratio was an annualized 46 basis points year-to-date -- the same as in the second quarter of 2015 and down from 48 basis points through the end of the third quarter of 2014.

Read the press release.

Total loans at federally insured credit unions reached $769.5 billion in the third quarter of 2015, an increase of 3.3 percent from the previous quarter and 10.7 percent from a year earlier. All major loan categories posted growth during the third quarter -- non-federally guaranteed student loans grew by 5.1 percent; new auto loans were up 4.4 percent; used auto loans rose by 3.7 percent; first mortgage loans and member business loans increased by 3 percent.

The NCUA reported a surge in indirect lending at federally insured credit unions. Indirect loans were $131.5 billion at the end of the third quarter of 2015 and represented 17.09 percent of total industry loans. This is up from approximately $108 billion a year earlier, which accounted for 15.53 percent of all credit union loans.

Overall, share and deposit accounts at federally insured credit unions increased $5.6 billion from the second quarter 2015 and $53.3 billion from the end of the third quarter of 2014 to $992.5 billion.

Because loans grew at a faster rate than shares and deposits, the loan-to-share ratio rose from 75.52 percent at the end of the second quarter to 77.53 percent as of September 30, 2015.

Credit Unions Earned $2.3 Billion in Q3

Federally insured credit unions continued to report positive net income in the third quarter, $2.3 billion, a decline of $82 million, or 3.5 percent, from the third quarter of 2014. As a whole, federally insured credit unions have recorded positive net income for 23 straight quarters.

Year-to-date federally-insured credit union profits were almost $6.9 billion -- up from slightly below $6.8 billion for the same time period of 2014.

Federally insured credit unions’ year-to-date return on average assets ratio stood at an annualized 80 basis points at the end of the third quarter, slightly below the level in the third quarter of 2014. Overall, 78 percent of federally insured credit unions reported positive returns on average assets for the first three quarters of 2015, compared to 76 percent in the first three quarters of 2014.

98 Percent of Credit Unions Were Well-Capitalized

The credit union industry continued to build its net worth during the quarter. The credit union industry's net worth ratio increased by 7 basis points during the third quarter to 10.99 percent.

The percentage of federally insured credit unions that were well-capitalized rose in the third quarter, with 98.0 percent reporting a net worth ratio at or above the statutorily required 7.0 percent. A year earlier, 97.5 percent of credit unions were well-capitalized. As of September 30, 2015, 34 federally insured credit unions were undercapitalized.

Delinquencies Rose for Second Consecutive Quarter

It appears that the credit cycle is turning. Delinquent loans are up for the second consecutive quarter. Loans 60 days or more past due rose by approximately $450 million during the quarter to almost $6 billion and is up by more than $1 billion since March 31, 2015.

In addition, early delinquencies were $6.1 billion at the end of the third quarter, an increase of $456 million from the end of the second quarter.

According to NCUA, delinquency rates edged higher during the quarter, while net charge-off rates unchanged. The delinquency rate at federally insured credit unions rose in the third quarter to 78 basis points, up from 74 basis points the previous quarter, but still below the 85 basis-point level in the third quarter of 2014. The net charge-off ratio was an annualized 46 basis points year-to-date -- the same as in the second quarter of 2015 and down from 48 basis points through the end of the third quarter of 2014.

Read the press release.

Thursday, December 3, 2015

Alaska USA Adds Underserved Area in Arizona

The National Credit Union Administration (NCUA) in October approved Alaska USA Federal Credit Union's addition of 413 underserved census tracts in Maricopa County, Arizona.

This underserved area expansion will allow Alaska USA to serve almost 1.7 million residents in Maricopa County -- further growing the credit union's presence in Arizona.

Alaska USA currently operates in four Western states -- Alaska, Arizona, California, and Washington.

This underserved area expansion will allow Alaska USA to serve almost 1.7 million residents in Maricopa County -- further growing the credit union's presence in Arizona.

Alaska USA currently operates in four Western states -- Alaska, Arizona, California, and Washington.

Wednesday, December 2, 2015

California Coast CU Forging Sponsorship Deal with City of San Diego

The San Diego Union Tribune is reporting that California Coast Credit Union is forging a deal with the City of San Diego to become a city sponsor.

The deal is valued at approximately $3 million over 5 years and awaits final approval by full city council.

The deal with California Coast would provide $650,000 cash over the next five years plus services for employees and the community with an estimated valued of nearly $2.5 million.

In exchange, California Coast would become the official financial partner of the city, get exclusive rights to market its services to city employees and retirees, and be included in publicity for city-sponsored community programs.

The five-year deal would allow the city or the $1.9 billion credit union to opt out after three years.

Read the story.

The deal is valued at approximately $3 million over 5 years and awaits final approval by full city council.

The deal with California Coast would provide $650,000 cash over the next five years plus services for employees and the community with an estimated valued of nearly $2.5 million.

In exchange, California Coast would become the official financial partner of the city, get exclusive rights to market its services to city employees and retirees, and be included in publicity for city-sponsored community programs.

The five-year deal would allow the city or the $1.9 billion credit union to opt out after three years.

Read the story.

MidFlorida CU Is Sued over Misleading Overdraft Practices

Reuters is reporting that MidFlorida Credit Union (Lakeland, FL) was hit with a proposed class action lawsuit accusing the credit union of violating federal law by charging customers overdraft fees when members had enough money in their checking accounts to cover any debits.

Filed last week, the lawsuit said MidFlorida Credit Union used an artificial "available balance" to decide whether to charge an overdraft, instead of the actual balance in a customer's account.

Read the story.

Filed last week, the lawsuit said MidFlorida Credit Union used an artificial "available balance" to decide whether to charge an overdraft, instead of the actual balance in a customer's account.

Read the story.

Tuesday, December 1, 2015

Greater Abyssinia Federal Credit Union Closed

The National Credit Union Administration (NCUA) closed Greater Abyssinia Federal Credit Union of Cleveland, Ohio.

NCUA made the decision to liquidate Greater Abyssinia Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operation.

The credit union reported that 28.46 percent of its loans and 10.76 percent of its assets were 60 days or more past due. The credit union also reported a 2015 year-to-date loss of almost $20 thousand and a full year loss for 2014 of almost $34 thousand.

Greater Abyssinia Federal Credit Union served 425 members and had assets of $412,775, according to the credit union’s most recent Call Report.

Greater Abyssinia Federal Credit Union is the ninth federally insured credit union liquidation in 2015.

Read the press release.

NCUA made the decision to liquidate Greater Abyssinia Federal Credit Union and discontinue operations after determining the credit union was insolvent and had no prospect for restoring viable operation.

The credit union reported that 28.46 percent of its loans and 10.76 percent of its assets were 60 days or more past due. The credit union also reported a 2015 year-to-date loss of almost $20 thousand and a full year loss for 2014 of almost $34 thousand.

Greater Abyssinia Federal Credit Union served 425 members and had assets of $412,775, according to the credit union’s most recent Call Report.

Greater Abyssinia Federal Credit Union is the ninth federally insured credit union liquidation in 2015.

Read the press release.

Small Business Data Collection on Bureau's Rulemaking Agenda

On the Consumer Financial Protection Bureau's regulatory agenda for the next year is the collection of information on financial institutions' lending to women-owned, minority-owned, and small businesses.

This data collection is mandated by the Section 1071 of Dodd-Frank Act.

According to the Dodd-Frank Act, the purpose of this data collection is to facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority- owned, and small businesses.

According to the Dodd-Frank Act, the following information will be collected by the Consumer Financial Protection Bureau (Bureau):

(A) the number of the application and the date on which the application was received;

(B) the type and purpose of the loan or other credit being applied for;

(C) the amount of the credit or credit limit applied for, and the amount of the credit transaction or the credit limit approved for such applicant;

(D) the type of action taken with respect to such application, and the date of such action;

(E) the census tract in which is located the principal place of business of the women-owned, minority-owned, or small business loan applicant;

(F) the gross annual revenue of the business in the last fiscal year of the women-owned, minority-owned, or small business loan applicant preceding the date of the application; ‘‘(G) the race, sex, and ethnicity of the principal owners of the business; and

(H) any additional data that the Bureau determines would aid in fulfilling the purposes of this section.

The Bureau indicated that its data collection efforts will build off a similar rule it finalized regarding the collection of home mortgage lending data.

This data collection mandate will impose a new regulatory burden on banks and credit unions.

Read the Bureau's Fall Rulemaking Agenda.

This data collection is mandated by the Section 1071 of Dodd-Frank Act.

According to the Dodd-Frank Act, the purpose of this data collection is to facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority- owned, and small businesses.

According to the Dodd-Frank Act, the following information will be collected by the Consumer Financial Protection Bureau (Bureau):

(A) the number of the application and the date on which the application was received;

(B) the type and purpose of the loan or other credit being applied for;

(C) the amount of the credit or credit limit applied for, and the amount of the credit transaction or the credit limit approved for such applicant;

(D) the type of action taken with respect to such application, and the date of such action;

(E) the census tract in which is located the principal place of business of the women-owned, minority-owned, or small business loan applicant;

(F) the gross annual revenue of the business in the last fiscal year of the women-owned, minority-owned, or small business loan applicant preceding the date of the application; ‘‘(G) the race, sex, and ethnicity of the principal owners of the business; and

(H) any additional data that the Bureau determines would aid in fulfilling the purposes of this section.

The Bureau indicated that its data collection efforts will build off a similar rule it finalized regarding the collection of home mortgage lending data.

This data collection mandate will impose a new regulatory burden on banks and credit unions.

Read the Bureau's Fall Rulemaking Agenda.

Subscribe to:

Posts (Atom)

{kind=link}