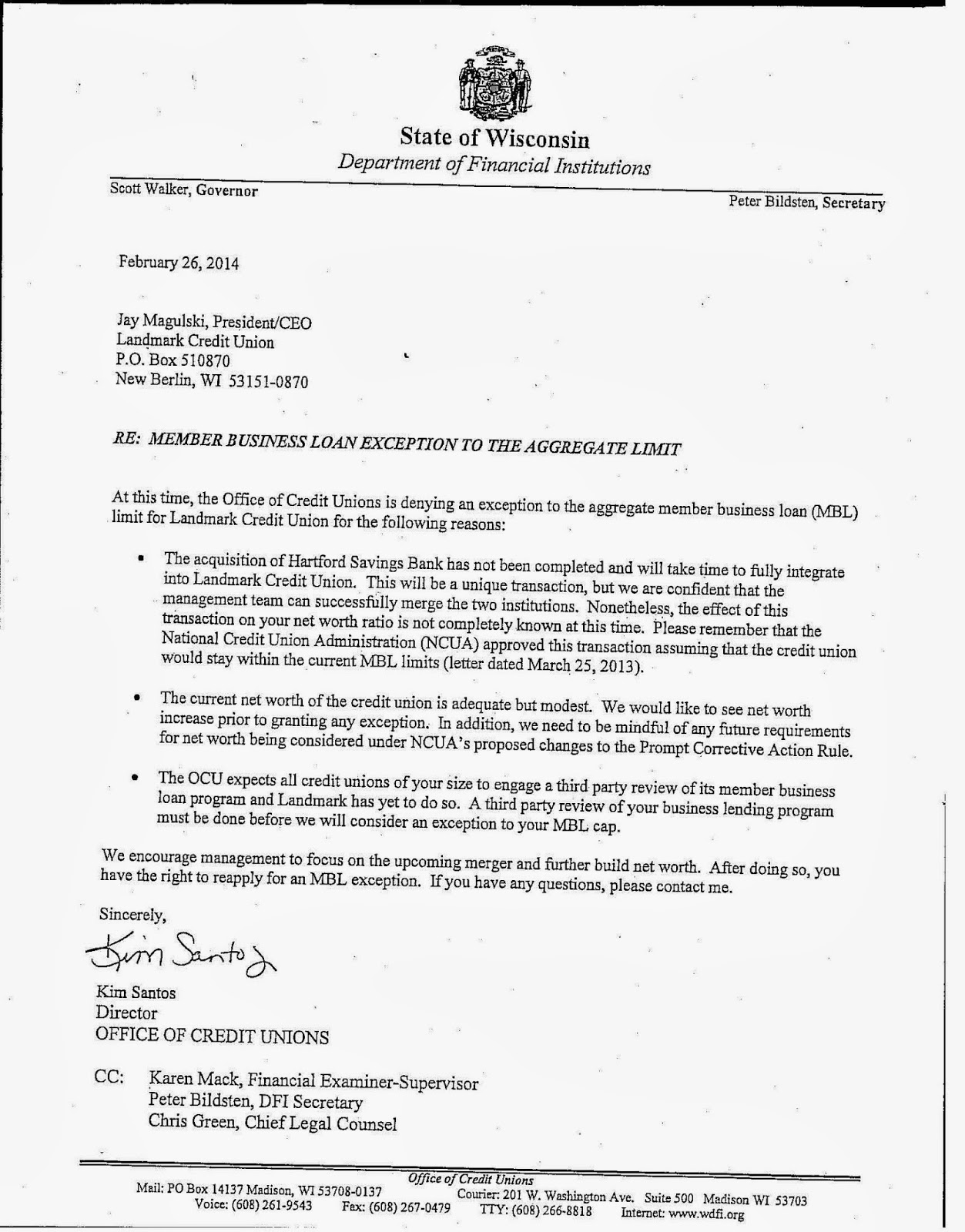

The OCU cited three reasons for denying the request.

First, the credit union had not completed its acquisition of Hartford Savings Bank. The state regulator noted that it will take time for Hartford Savings Bank to be integrated into Landmark, given the uniqueness of this transaction. Moreover, it was not clear at this time what impact this transaction would have on the credit union's net worth ratio. Furthermore, the OCU pointed out that the National Credit Union Administration approved this acquisition assuming the credit union would stay within its current member business loan limits.

Second, the OCU noted that the credit union's net worth ratio was adequate, but modest. The OCU wanted an increase in net worth before granting an exception to the business loan cap.

Third, OCU wanted a third party review of the credit union's member business loan program and Landmark has not done so. It is an expectation of the OCU that credit unions of Landmark's size engage in a third party review of its business lending program.

The OCU told Landmark to focus on the merger and to build its net worth. The credit union can reapply after doing so.

No comments:

Post a Comment