The National Credit Union Administration (NCUA) liquidated C B S Employees Federal Credit Union (Studio City, CA).

University Credit Union (Los Angeles, CA) immediately assumed C B S Employees’ assets, loans, and all member shares.

NCUA made the decision to liquidate C B S Employees because the credit union was insolvent and had no prospect of becoming viable.

According to a press release from U.S. Attorney's Office of Central District of California, a long-time manager of the credit union, who is in federal custody, is alleged to have embezzled $40 million over two decades and spent the money on gambling, expensive cars and watches, and travel by private jets.

At the time of liquidation and subsequent purchase and assumption by University Credit Union, C B S Employees served 2,798 members and had assets of $21,037,558, according to the credit union’s most recent Call Report.

This is the first credit union failure of 2019.

Read the press release.

Friday, March 29, 2019

House Committee Advances SAFE Banking Act

By a vote of 45 to 15, the House Financial Services Committee yesterday advanced the Secure and Fair Enforcement (SAFE) Banking Act, which would address the issue of providing financial services to cannabis-related businesses.

The SAFE Banking Act specifies that proceeds from “cannabis-related legitimate businesses” would not be considered unlawful under federal money laundering rules or other laws. It would also direct the Financial Crimes Enforcement Network and federal banking regulators to issue guidance and exam procedures for banks and credit unions that serve cannabis-related legitimate businesses.

Earlier this week, the American Bankers Association and the Credit Union National Association wrote a joint letter to members of the House Financial Services Committee in support of the SAFE Banking Act

The SAFE Banking Act specifies that proceeds from “cannabis-related legitimate businesses” would not be considered unlawful under federal money laundering rules or other laws. It would also direct the Financial Crimes Enforcement Network and federal banking regulators to issue guidance and exam procedures for banks and credit unions that serve cannabis-related legitimate businesses.

Earlier this week, the American Bankers Association and the Credit Union National Association wrote a joint letter to members of the House Financial Services Committee in support of the SAFE Banking Act

Thursday, March 28, 2019

Power Financial CU to Buy TransCapital Bank

Power Financial Credit Union (Pembroke Pines, FL) has signed a definitive agreement to purchase TransCapital Bank (Sunrise, FL).

Power Financial CU has almost $655 million in assets, according to its most recent call report. TransCapital Bank has $204 million in assets at the end of 2018.

The transaction is expected to close during the third quarter of 2019, subject to customary closing conditions and shareholder and regulatory approvals.

The price of the deal was not disclosed.

This is the fourth announced purchase of a Florida bank by a Florida credit union this year.

Read the press release.

Power Financial CU has almost $655 million in assets, according to its most recent call report. TransCapital Bank has $204 million in assets at the end of 2018.

The transaction is expected to close during the third quarter of 2019, subject to customary closing conditions and shareholder and regulatory approvals.

The price of the deal was not disclosed.

This is the fourth announced purchase of a Florida bank by a Florida credit union this year.

Read the press release.

NCUSIF Assisted Mergers Lack Transparency

The National Credit Union Administration's response to questions about charges to the National Credit Union Share Insurance Fund (NCUSIF) associated with assisted mergers in the fourth quarter lacked illumination.

One slide in the NCUSIF presentation at the March National Credit Union Administration (NCUA) Board meeting showed charges for assisted mergers of $39.5 million during the fourth quarter.

The following are questions to a NCUA spokesperson and the spokesperson's response.

One slide in the NCUSIF presentation at the March National Credit Union Administration (NCUA) Board meeting showed charges for assisted mergers of $39.5 million during the fourth quarter.

The following are questions to a NCUA spokesperson and the spokesperson's response.

Q: What type of assistance did NCUA offer during the fourth quarter?We will have to wait for the semi-annual report to Congress from the agency's Inspector General to see whether a material loss review is being conducted with respect to the NCUSIF assisted merger of Bay Ridge Federal Credit Union. The Brooklyn, New York-based credit union had significant exposure to taxi medallion loans.

Q: Was the charge associated with the merger of Bay Ridge FCU into Island FCU?

A: Slide five of the Q4 2018 Share Insurance Fund report shows the aggregate charges for assisted mergers was $39.6 million for the year and $39.5 million for the fourth quarter. The NCUA posts assisted mergers on its Conservatorships and Liquidations page, but the agency does not make public details of the type or level of assistance in an individual merger.

Q: Will the Office of the Inspector General do an audit on this assisted merger?

A: “The Dodd-Frank Wall Street Reform and Consumer Protection Act obligates the NCUA OIG to conduct material loss reviews (MLRs) of credit unions that incurred a loss of $25 million or more to the National Credit Union Share Insurance Fund. In addition, Dodd-Frank requires the OIG to review all losses under the $25 million threshold to assess whether an in-depth review is warranted due to unusual circumstances.”

Wednesday, March 27, 2019

Minneapolis City Council to Provide Up to $500,000 to New Minority CU

The Ways and Means Committee of the Minneapolis City Council will provide up to $500,000 in funding for a new credit union serving minority residents in north Minneapolis.

The contract is with the Association for Black Economic Power, which is a community-led nonprofit organization. The organization is seeking to establish Minnesota's only black-led financial institution, the Village Financial Cooperative (VFC).

VFC has obtained approval to form a credit union from the state in late 2018 and is in the late stages of its application for insurance/authorization from the National Credit Union Administration.

The city will provide up to $400,000 in a 10-year, interest-free forgivable loan. The loan can be used for occupancy, leasehold improvements and equipment expenses for retail space located in North Minneapolis.

The loan will be forgiven if the following conditions are met:

The credit union expects to open in June 2019.

Read more.

The contract is with the Association for Black Economic Power, which is a community-led nonprofit organization. The organization is seeking to establish Minnesota's only black-led financial institution, the Village Financial Cooperative (VFC).

VFC has obtained approval to form a credit union from the state in late 2018 and is in the late stages of its application for insurance/authorization from the National Credit Union Administration.

The city will provide up to $400,000 in a 10-year, interest-free forgivable loan. The loan can be used for occupancy, leasehold improvements and equipment expenses for retail space located in North Minneapolis.

The loan will be forgiven if the following conditions are met:

- VFC will open a brick and mortar store in North Minneapolis in 2019.

- VFC will provide a financial literacy program for the residents of the City of Minneapolis, with at least 30 classes (300 attendees) in 2019.

- VFC will enroll at least 500 members in checking or savings accounts in 2019.VFC will hold at least six major community outreach events to promote VFC and recruit members.

The credit union expects to open in June 2019.

Read more.

Tuesday, March 26, 2019

Sound CU Completes Acquisition of Bank

Sound Credit Union (Tacoma, WA) on March 26 finalized its acquisition of The Bank of Washington (Lynnwood, WA).

This is the first credit union to acquire a bank in the State of Washington.

The Bank of Washington had $206.3 million in assets at the end of 2018. Sound Credit Union had $1.5 billion in assets, as of December 2018.

Sound CU received the final regulatory approval from the National Credit Union Administration earlier in March 2019.

https://www.cuinsight.com/press-release/sound-credit-union-finalizes-acquisition-of-the-bank-of-washington

This is the first credit union to acquire a bank in the State of Washington.

The Bank of Washington had $206.3 million in assets at the end of 2018. Sound Credit Union had $1.5 billion in assets, as of December 2018.

Sound CU received the final regulatory approval from the National Credit Union Administration earlier in March 2019.

https://www.cuinsight.com/press-release/sound-credit-union-finalizes-acquisition-of-the-bank-of-washington

Joint Trade Group Letter Urges Support of Cannabis Banking Bill

The American Bankers Association (ABA) and the Credit Union National Association (CUNA) sent a joint letter to members of the Committee on Financial Services on March 25 in support of the Secure and Fair Enforcement Banking Act (H.R. 1595).

The bill is being marked up on March 26 in the House Financial Services Committee.

“Although we do not take a position on the legalization of marijuana, our members are committed to serving the financial needs of their communities—including those that have voted to legalize cannabis,” wrote ABA President and CEO Rob Nichols and CUNA President and CEO Jim Nussle.

Read the letter.

The bill is being marked up on March 26 in the House Financial Services Committee.

“Although we do not take a position on the legalization of marijuana, our members are committed to serving the financial needs of their communities—including those that have voted to legalize cannabis,” wrote ABA President and CEO Rob Nichols and CUNA President and CEO Jim Nussle.

Read the letter.

Fewer Enforcement Orders Issued by NCUA in 2018

Fewer enforcement orders were issued by the National Credit Union Administration (NCUA) during 2018.

The number of Preliminary Warning Letters (PWLs) issued during 2018 fell by 10 to 46.

Letters of Understanding and Agreement (LUAs) issued in 2018 declined to 96 from 105 in 2017. All LUAs issued in 2018 were unpublished.

There were zero Cease and Desist Orders (CDOs) issued in 2018, down from 2 in 2017.

The information was obtained from NCUA by a Freedom of Information Act request.

The following chart shows the number of orders issued by NCUA from 2013 to 2018.

The number of Preliminary Warning Letters (PWLs) issued during 2018 fell by 10 to 46.

Letters of Understanding and Agreement (LUAs) issued in 2018 declined to 96 from 105 in 2017. All LUAs issued in 2018 were unpublished.

There were zero Cease and Desist Orders (CDOs) issued in 2018, down from 2 in 2017.

The information was obtained from NCUA by a Freedom of Information Act request.

The following chart shows the number of orders issued by NCUA from 2013 to 2018.

Friday, March 22, 2019

Study: CUs Did Little to Help Members Obtain HELOCs during the Financial Crisis

A paper published in Applied Economics Letters concluded that credit unions did not provide consumers with liquidity during the recent financial crisis.

The paper, Credit Unions during the Crisis: Did They Provide Liquidity?, examined whether credit unions provided liquidity to individuals in the form of home equity line of credit (HELOC) during financial crisis of 2008 in areas experiencing decline in home prices.

The study justified using HELOCs as a measure of consumer liquidity, because HELOCs can be used for any purpose. The paper did not examine credit card loans, which can be used for the same purpose; because credit unions are fringe players in the credit card marketplace.

The authors, Pankaj Maskara & Florence Neymotin, employed data from the Consumer Finance Monthly survey and limited their analysis to the time period between April 12, 2007 and March 13, 2013.

The paper controlled for selection bias. In other words, the decision regarding a HELOC could have been the choice of a credit union member, not the action of a credit union.

The authors found that after controlling for selection bias credit unions during the financial crisis did not extend HELOCs any more than other depository institutions in areas experiencing housing price declines.

However, the results from the paper are limited to HELOCs offered by credit unions.

Click here to go to Applied Economics Letters (there is a charge to download the paper).

The paper, Credit Unions during the Crisis: Did They Provide Liquidity?, examined whether credit unions provided liquidity to individuals in the form of home equity line of credit (HELOC) during financial crisis of 2008 in areas experiencing decline in home prices.

The study justified using HELOCs as a measure of consumer liquidity, because HELOCs can be used for any purpose. The paper did not examine credit card loans, which can be used for the same purpose; because credit unions are fringe players in the credit card marketplace.

The authors, Pankaj Maskara & Florence Neymotin, employed data from the Consumer Finance Monthly survey and limited their analysis to the time period between April 12, 2007 and March 13, 2013.

The paper controlled for selection bias. In other words, the decision regarding a HELOC could have been the choice of a credit union member, not the action of a credit union.

The authors found that after controlling for selection bias credit unions during the financial crisis did not extend HELOCs any more than other depository institutions in areas experiencing housing price declines.

However, the results from the paper are limited to HELOCs offered by credit unions.

Click here to go to Applied Economics Letters (there is a charge to download the paper).

Wednesday, March 20, 2019

Median CU Membership Growth Was Negative in 15 States for 2018

At least half of credit unions in 15 states, including the District of Columbia, saw declining membership for 2018.

The states with the lowest median membership growth rate for 20018 were the District of Columbia at minus 1.7 percent, Pennsylvania at negative 1.5 percent, Illinois at minus 1.4 percent, and New Jersey at negative 1.0 percent.

The other states with negative membership growth were Mississippi (-0.8 percent), Connecticut (-0.5 percent), Delaware (-0.5 percent), North Dakota (-0.5 percent), Louisiana (-0.3 percent), Ohio (-0.3 percent), Massachusetts (-0.2 percent), Nebraska (-0.2 percent), Oklahoma (-0.2 percent), Hawaii (-0.1 percent), and Texas (-0.1 percent).

The National Credit Union Administration noted that credit unions with declining membership tend to be small, as about 75 percent of credit unions has assets below $50 million.

In addition, three states with negative median year-over-year membership growth rate for 2018 had negative year-over-year median asset and share growth rates. The three states were Delaware, New Jersey, and Louisiana. The median year-over-year asset and shares growth rates for Delaware were minus 1.2 percent and minus 0.3 percent, for New Jersey were minus 0.3 percent and minus 0.7 percent, and for Louisiana were minus 0.1 percent and minus 0.7 percent.

The states with the lowest median membership growth rate for 20018 were the District of Columbia at minus 1.7 percent, Pennsylvania at negative 1.5 percent, Illinois at minus 1.4 percent, and New Jersey at negative 1.0 percent.

The other states with negative membership growth were Mississippi (-0.8 percent), Connecticut (-0.5 percent), Delaware (-0.5 percent), North Dakota (-0.5 percent), Louisiana (-0.3 percent), Ohio (-0.3 percent), Massachusetts (-0.2 percent), Nebraska (-0.2 percent), Oklahoma (-0.2 percent), Hawaii (-0.1 percent), and Texas (-0.1 percent).

The National Credit Union Administration noted that credit unions with declining membership tend to be small, as about 75 percent of credit unions has assets below $50 million.

In addition, three states with negative median year-over-year membership growth rate for 2018 had negative year-over-year median asset and share growth rates. The three states were Delaware, New Jersey, and Louisiana. The median year-over-year asset and shares growth rates for Delaware were minus 1.2 percent and minus 0.3 percent, for New Jersey were minus 0.3 percent and minus 0.7 percent, and for Louisiana were minus 0.1 percent and minus 0.7 percent.

Tuesday, March 19, 2019

CU Tax Expenditure Exceeds $24 Billion for Fiscal Years 2019 - 2028

The Office of Management and Budget estimated that the tax expenditure associated with exempting credit union income from corporate income taxes is $24.017 billion over the next ten fiscal years.

The following graph shows the annual tax expenditure for exempting credit union income from corporate income taxes for fiscal years 2019 thru 2028.

The following graph shows the annual tax expenditure for exempting credit union income from corporate income taxes for fiscal years 2019 thru 2028.

Monday, March 18, 2019

Fewer Outstanding Enforcement Actions at the End of 2018

The number of outstanding enforcement actions for federally insured credit unions decreased from 296 at the end of 2017 to 278 at the end of 2018, according to the 2018 Annual Report of the National Credit Union Administration (NCUA).

Enforcement actions include Preliminary Warning Letters (PWLs), Letters of Understanding and Agreement (LUAs), Cease-and-Desist Orders (CDOs), and Conservatorships.

The following table shows the number of outstanding enforcement actions by type for both state chartered and federal credit unions between 2014 and 2018 (click on image to enlarge).

Enforcement actions include Preliminary Warning Letters (PWLs), Letters of Understanding and Agreement (LUAs), Cease-and-Desist Orders (CDOs), and Conservatorships.

The following table shows the number of outstanding enforcement actions by type for both state chartered and federal credit unions between 2014 and 2018 (click on image to enlarge).

Sunday, March 17, 2019

ESL FCU Sued over Assessing Insufficient Funds Fees

A federal class-action lawsuit accuses ESL Federal Credit Union (Rochester, NY) of assessing multiple insufficient funds fees on a single transaction.

The class-action lawsuit was filed on February 15, 2019 in the U.S. District Court Western District of New York.

The complaint alleges that ESL FCU sometimes charges returned item fees in violation of its contract and New York consumer protection law.

Read more.

The class-action lawsuit was filed on February 15, 2019 in the U.S. District Court Western District of New York.

The complaint alleges that ESL FCU sometimes charges returned item fees in violation of its contract and New York consumer protection law.

Read more.

Saturday, March 16, 2019

Centris FCU to Start Construction on $30 Million HQ Building

Centris Federal Credit Union (Omaha, NE) will start this spring construction on $30 million corporate headquarters building in the Sterling Park office park.

The facility will be a four-story, 115,000-square-foot building.

The new building will include an outdoor patio and community meeting room.

Centris expects to lease a portion of the building to other tenants. Since federal credit unions are exempt from unrelated business income taxation, income from leasing this excess space will not be taxed.

Read more.

The facility will be a four-story, 115,000-square-foot building.

The new building will include an outdoor patio and community meeting room.

Centris expects to lease a portion of the building to other tenants. Since federal credit unions are exempt from unrelated business income taxation, income from leasing this excess space will not be taxed.

Read more.

Friday, March 15, 2019

Senate Confirms Harper and Hood to Serve on NCUA Board

The United States Senate on March 14 confirmed Rodney Hood and Todd Harper to serve on the National Credit Union Administration (NCUA) Board.

This is the second time for Rodney Hood to serve on he NCUA Board. He had previously served on the Board from 2005 to 2010.

Todd Harper had served as director of Public and Congressional Affairs for NCUA and as chief policy advisor to NCUA Chairman Debbie Matz.

Hood's term will expire in August 2023 and Harper's term will expire in April 2021.

This is the first time, since April 2016, that the NCUA Board has had three members.

This is the second time for Rodney Hood to serve on he NCUA Board. He had previously served on the Board from 2005 to 2010.

Todd Harper had served as director of Public and Congressional Affairs for NCUA and as chief policy advisor to NCUA Chairman Debbie Matz.

Hood's term will expire in August 2023 and Harper's term will expire in April 2021.

This is the first time, since April 2016, that the NCUA Board has had three members.

Bill Won't Require CUs to Comply with CRA and Will Allow All FCUs to Add Underserved Areas

Legislation introduced in the House and Senate on March 13, the American Housing and Economic Mobility Act, will exclude credit unions from complying with the Community Reinvestment Act.

Section 203 of the bill, which will be known as The "Community Reinvestment Reform Act of 2019," would strengthen obligations under the Community Reinvestment Act (CRA) to provide credit to low- and moderate-income communities by extending the law to cover more non-bank mortgage companies, promote investment in activities that help poor and moderate-income communities, and strengthen sanctions against institutions that fail to follow the rules.

Jim Nussle, President and CEO of the Credit Union National Association, wrote that the bill "properly recognizes the distinctions that exist between credit unions and banks when meeting community needs."

An earlier version of this bill introduced in the last Congress would have applied CRA to credit unions that did not have a ,ow-income designation.

Section 204 of the bill will allow a federal credit union regardless of common bond type to add underserved areas. Currently, only multiple common-bond credit unions can add underserved areas. The bill would also add reporting requirements for a federal credit union adding an underserved area and require the National Credit Union Administration to annually publish certain information.

The legislation was introduced in the Senate by Senators Elizabeth Warren (D-MA), Kirsten Gillibrand (D-N.Y.), and Edward Markey (D-MA). In the House of Representatives, the bill sponsors were Representatives Cedric Richmond (D-LA), Barbara Lee (D-CA), Gwen Moore (D-WI), Elijah Cummings (D-MD), Mark Pocan (D-WI), Ayanna Pressley (D-MA), Rashida Tlaib (D-MI), Susan Wild (D-PA), Eleanor Holmes Norton (D-D.C.), Steve Cohen (D-TN), Jamie Raskin (D-MD), Ro Khanna (D-CA), Joe Kennedy III (D-MA), and Suzanne Bonamici (D-OR).

Read the text of the bill.

Section 203 of the bill, which will be known as The "Community Reinvestment Reform Act of 2019," would strengthen obligations under the Community Reinvestment Act (CRA) to provide credit to low- and moderate-income communities by extending the law to cover more non-bank mortgage companies, promote investment in activities that help poor and moderate-income communities, and strengthen sanctions against institutions that fail to follow the rules.

Jim Nussle, President and CEO of the Credit Union National Association, wrote that the bill "properly recognizes the distinctions that exist between credit unions and banks when meeting community needs."

An earlier version of this bill introduced in the last Congress would have applied CRA to credit unions that did not have a ,ow-income designation.

Section 204 of the bill will allow a federal credit union regardless of common bond type to add underserved areas. Currently, only multiple common-bond credit unions can add underserved areas. The bill would also add reporting requirements for a federal credit union adding an underserved area and require the National Credit Union Administration to annually publish certain information.

The legislation was introduced in the Senate by Senators Elizabeth Warren (D-MA), Kirsten Gillibrand (D-N.Y.), and Edward Markey (D-MA). In the House of Representatives, the bill sponsors were Representatives Cedric Richmond (D-LA), Barbara Lee (D-CA), Gwen Moore (D-WI), Elijah Cummings (D-MD), Mark Pocan (D-WI), Ayanna Pressley (D-MA), Rashida Tlaib (D-MI), Susan Wild (D-PA), Eleanor Holmes Norton (D-D.C.), Steve Cohen (D-TN), Jamie Raskin (D-MD), Ro Khanna (D-CA), Joe Kennedy III (D-MA), and Suzanne Bonamici (D-OR).

Read the text of the bill.

Thursday, March 14, 2019

Number of Problem CUs Fell in Q4, But Assets and Shares Increased in Problem CUs

The number of problem credit unions fell during the fourth quarter of 2018, according to the National Credit Union Administration (NCUA).

At the end of the fourth quarter of 2018, there were 193 problem credit unions. In comparison, there were 203 problem credit unions at the end of the third quarter of 2018.

A problem credit union has a composite CAMEL rating of 4 or 5.

Total assets and shares (deposits) in problem credit unions rose during the fourth quarter. Assets in problem credit unions were $11.8 billion at the end of 2018 compared to $11.5 billion at the end of the third quarter of 2018. Shares in problem credit unions were $10.6 billion as of December 2018 versus $10.4 billion as of September 30, 2018.

The number of problem credit unions with less than $100 million fell by 14 to 165 during the fourth quarter. But the number of problem credit unions with between $100 million in assets and $500 million in assets increased by 4 to 25 during the quarter.

NCUA reported that 85.5 percent of problem credit unions have less than $100 million in assets, while slightly more than 2 percent of problem credit unions have more than $500 million in assets.

At the end of the fourth quarter, 0.93 percent of total insured shares were in problem credit unions. This was up 2 basis points from September 2018.

In related note, for all of 2018 charges for liquidations and assisted mergers were $752.9 million and $39.6 million, respectively. NCUA recorded a charge of $39.5 million associated with assisted mergers in the fourth quarter. This is probably associated with the merger of Bay Ridge FCU (Brooklyn, NY) into Island Federal Credit Union (Hauppauge, NY).

At the end of the fourth quarter of 2018, there were 193 problem credit unions. In comparison, there were 203 problem credit unions at the end of the third quarter of 2018.

A problem credit union has a composite CAMEL rating of 4 or 5.

Total assets and shares (deposits) in problem credit unions rose during the fourth quarter. Assets in problem credit unions were $11.8 billion at the end of 2018 compared to $11.5 billion at the end of the third quarter of 2018. Shares in problem credit unions were $10.6 billion as of December 2018 versus $10.4 billion as of September 30, 2018.

The number of problem credit unions with less than $100 million fell by 14 to 165 during the fourth quarter. But the number of problem credit unions with between $100 million in assets and $500 million in assets increased by 4 to 25 during the quarter.

NCUA reported that 85.5 percent of problem credit unions have less than $100 million in assets, while slightly more than 2 percent of problem credit unions have more than $500 million in assets.

At the end of the fourth quarter, 0.93 percent of total insured shares were in problem credit unions. This was up 2 basis points from September 2018.

In related note, for all of 2018 charges for liquidations and assisted mergers were $752.9 million and $39.6 million, respectively. NCUA recorded a charge of $39.5 million associated with assisted mergers in the fourth quarter. This is probably associated with the merger of Bay Ridge FCU (Brooklyn, NY) into Island Federal Credit Union (Hauppauge, NY).

Tuesday, March 12, 2019

GAO: Congress Should Address Fragmentation and Overlap of Financial Regulation

The Government Accountability Office (GAO) on March 6 issued a report recommending Congress may want to consider options to address inefficiencies that hamper the financial regulatory system.

The report is part of GAO's High Risk Series.

In February 2016, GAO reported that fragmentation and overlap in the financial regulatory structure have created inefficiencies in regulatory processes and inconsistencies in how regulators oversee similar types of institutions.

GAO in its March 2019 report stated that Congressional action is needed to address this fragmentation and overlap in the regulatory structure.

GAO wrote:

For example, GAO suggested these objectives could be achieved by consolidating the number of federal agencies involved in overseeing the safety and soundness of depository institutions.

The report is part of GAO's High Risk Series.

In February 2016, GAO reported that fragmentation and overlap in the financial regulatory structure have created inefficiencies in regulatory processes and inconsistencies in how regulators oversee similar types of institutions.

GAO in its March 2019 report stated that Congressional action is needed to address this fragmentation and overlap in the regulatory structure.

GAO wrote:

"Congress should consider whether additional changes to the financial regulatory structure are needed to reduce or better manage fragmentation and overlap in the oversight of financial institutions and activities to improve (1) the efficiency and effectiveness of oversight; (2) the consistency of consumer and investor protections; and (3) the consistency of financial oversight for similar institutions, products, risks, and services."

For example, GAO suggested these objectives could be achieved by consolidating the number of federal agencies involved in overseeing the safety and soundness of depository institutions.

Monday, March 11, 2019

Bill Would Allow CUs to Accept Public Funds

Legislation (SB257) has been introduced in Arkansas Senate that would allow credit unions insured by the National Credit Union Administration to serve as depositories of public funds.

The Arkansas Bankers Association is opposed to the bill.

In an op-ed appearing in Arkansas Business, Lorrie Trogden, president and CEO of the Arkansas Bankers Association, wrote: "Allowing credit unions to take public deposits would only work against the state by reducing the state’s tax base as well as leaving less capital in community banks for lending to small businesses and consumers."

She further wrote: "If credit unions want to stray from their mission and act like banks, they should be taxed like banks."

Read the op-ed.

The Arkansas Bankers Association is opposed to the bill.

In an op-ed appearing in Arkansas Business, Lorrie Trogden, president and CEO of the Arkansas Bankers Association, wrote: "Allowing credit unions to take public deposits would only work against the state by reducing the state’s tax base as well as leaving less capital in community banks for lending to small businesses and consumers."

She further wrote: "If credit unions want to stray from their mission and act like banks, they should be taxed like banks."

Read the op-ed.

Sunday, March 10, 2019

NCUA at the Crossroads

Drew Johnson, senior fellow at the National Center for Public Policy Research, recently wrote that decisions by the National Credit Union Administration (NCUA) have favored large credit unions at the expense of "a wilting number of small neighborhood credit unions committed to serving less-affluent Americans in underserved areas."

Johnson cited examples of how these large credit unions are straying from the mission of credit unions.

For example, he mentioned these large credit unions are buying commercial banks and the naming rights to arenas.

In addition, Johnson pointed out NCUA's proposal to give large complex credit unions subject to the agency's risk-based capital requirement the authority to raise capital from Wall Street investors. He argued this proposal will fuel the rapid growth of the largest credit unions and does nothing for small credit unions.

He also noted this proposal will change how these large credit unions operate. Johnson wrote: "Even if investors aren’t given board seats or a formal role in the management of the institution, a credit union’s CEO would be much more likely to listen to the concerns of hedge fund manager than those of a member with a personal checking account."

By kowtowing to the interest of the biggest credit unions, NCUA has fueled the consolidation of the credit union industry and reduced consumer choice.

Johnson stated the agency is at the crossroad. He called on NCUA to stop its questionable decisions, which favor these large credit unions.

The opinion piece appeared on Newsmax.com.

Read the op-ed.

Johnson cited examples of how these large credit unions are straying from the mission of credit unions.

For example, he mentioned these large credit unions are buying commercial banks and the naming rights to arenas.

In addition, Johnson pointed out NCUA's proposal to give large complex credit unions subject to the agency's risk-based capital requirement the authority to raise capital from Wall Street investors. He argued this proposal will fuel the rapid growth of the largest credit unions and does nothing for small credit unions.

He also noted this proposal will change how these large credit unions operate. Johnson wrote: "Even if investors aren’t given board seats or a formal role in the management of the institution, a credit union’s CEO would be much more likely to listen to the concerns of hedge fund manager than those of a member with a personal checking account."

By kowtowing to the interest of the biggest credit unions, NCUA has fueled the consolidation of the credit union industry and reduced consumer choice.

Johnson stated the agency is at the crossroad. He called on NCUA to stop its questionable decisions, which favor these large credit unions.

The opinion piece appeared on Newsmax.com.

Read the op-ed.

Saturday, March 9, 2019

Bill Would Give CUs Greater Flexibility in Setting Loan Maturities

Representatives Lee Zeldin (R-NY) and Vicente Gonzalez (D-TX) on March 8 introduced legislation (H.R. 1661) that would give the National Credit Union Administration greater flexibility in setting loan maturity limits under the Federal Credit Union Act.

The Federal Credit Union Act limits the maximum loan maturity on certain loans to 15-years.

The bill, if it becomes law, would give credit unions greater ability to grow.

At the time this blog was published, the bill's language was not available.

The Federal Credit Union Act limits the maximum loan maturity on certain loans to 15-years.

The bill, if it becomes law, would give credit unions greater ability to grow.

At the time this blog was published, the bill's language was not available.

Friday, March 8, 2019

FFIEC Issues Policy Statement on Examination Reports

As part of its ongoing exam modernization initiative, the Federal Financial Institutions Examination Council om March 6 issued a policy statement aimed at promoting clarity and consistency of examination reports. The policy statement, which is intended to reduce regulatory burden for community banks and credit unions, includes principles that “set forth minimum expectations of what should be included in all reports of examination.”

Among other things, the principles establish that all reports on examinations should present conclusions and issues in order of importance; document the condition and risk profile of the institution; discuss the adequacy of the institution’s risk management practices; and document issues of supervisory concern or warranting prompt corrective action.

Concurrently, the agencies are rescinding their 1993 Interagency Policy Statement on the Uniform Core Report of Examination.

Read the policy statement.

Among other things, the principles establish that all reports on examinations should present conclusions and issues in order of importance; document the condition and risk profile of the institution; discuss the adequacy of the institution’s risk management practices; and document issues of supervisory concern or warranting prompt corrective action.

Concurrently, the agencies are rescinding their 1993 Interagency Policy Statement on the Uniform Core Report of Examination.

Read the policy statement.

Thursday, March 7, 2019

Consumer Credit at CUs Grew by $1.8 Billion in January 2019

Outstanding consumer credit at credit union grew at a slower pace in January 2019.

Total outstanding consumer credit at credit unions was $476 billion in January 2019. In comparison, total consumer credit at credit unions were $474.2 billion and $471.4 billion in December 2018 and November 2018, respectively.

While revolving credit contracted in January, nonrevolving credit grew at a faster pace for the month.

Revolving credit at credit unions fell during January 2019 by approximately $500 million to $62.1 billion.

Nonrevolving credit grew by by almost $2.3 billion during January 2019 to $413.9 billion, after increasing by $1.5 billion in December 2018.

Total outstanding consumer credit at credit unions was $476 billion in January 2019. In comparison, total consumer credit at credit unions were $474.2 billion and $471.4 billion in December 2018 and November 2018, respectively.

While revolving credit contracted in January, nonrevolving credit grew at a faster pace for the month.

Revolving credit at credit unions fell during January 2019 by approximately $500 million to $62.1 billion.

Nonrevolving credit grew by by almost $2.3 billion during January 2019 to $413.9 billion, after increasing by $1.5 billion in December 2018.

NCUA Board Approves $160.1 Million Equity Distribution from NCUSIF

The National Credit Union Administration (NCUA) Board on March 7, 2019 approved a $160.1 million equity distribution from the National Credit Union Share Insurance Fund (NCUSIF).

This is the second largest distribution to credit unions in the history of the NCUSIF.

At the end of the fourth quarter of 2018, the NCUSIF equity ratio was 1.39 percent -- above the normal operating level of 1.38 percent set by the NCUA Board. To lower the equity ratio to the normal operating level, the NCUA Board made the decision to make an equity distribution from the NCUSIF.

Eligible credit unions will receive a payment in the second quarter of 2019.

A financial institution that filed a quarterly Call Report as a federally insured credit union for at least one reporting period in calendar year 2018 will be eligible for a pro rata distribution.

Read the press release.

This is the second largest distribution to credit unions in the history of the NCUSIF.

At the end of the fourth quarter of 2018, the NCUSIF equity ratio was 1.39 percent -- above the normal operating level of 1.38 percent set by the NCUA Board. To lower the equity ratio to the normal operating level, the NCUA Board made the decision to make an equity distribution from the NCUSIF.

Eligible credit unions will receive a payment in the second quarter of 2019.

A financial institution that filed a quarterly Call Report as a federally insured credit union for at least one reporting period in calendar year 2018 will be eligible for a pro rata distribution.

Read the press release.

Lawsuit Accuses Ent CU of Improper OD Fees

A class-action lawsuit alleges Ent Credit Union (Colorado Springs, CO) organized debit transactions in a way to charge its customers more overdraft (OD) fees.

The lawsuit claims that Ent Credit Union would approve debit transactions while funds were available in customers' accounts, but the credit union would not process the transactions until later causing some customers to be hit with excess fees because of "intervening transactions."

The complaint also states Ent's members would be charged multiple fees for the same transaction, which is allegedly contrary to the company's deposit agreement.

Frank D. Azar & Associates filed the complaint Monday in U.S. District Court in Denver on behalf of plaintiffs in Colorado and Texas.

Read the story.

The lawsuit claims that Ent Credit Union would approve debit transactions while funds were available in customers' accounts, but the credit union would not process the transactions until later causing some customers to be hit with excess fees because of "intervening transactions."

The complaint also states Ent's members would be charged multiple fees for the same transaction, which is allegedly contrary to the company's deposit agreement.

Frank D. Azar & Associates filed the complaint Monday in U.S. District Court in Denver on behalf of plaintiffs in Colorado and Texas.

Read the story.

Wednesday, March 6, 2019

CUs Report Record Net Income of $13 Billion for 2018

The National Credit Union Administration reported record net income for federally insured credit unions (FICUs) of $13 billion in 2018. This is up $2.7 billion from the same period a year ago.

For 2018, interest income rose by 13.8 percent and nonineterest income was up 9.3 percent. Interest expense jumped by 29.4 percent in 2018, while nonineterest expenses advanced by 8.8 percent.

Only 631 FICUs reported a loss for 2018.

FICUs reported a return on average assets (ROAA) of 92 basis points for 2018. In comparison, ROAA for 2017 was 78 basis points.

Factors helping to drive the improved profitability of FICUs during 2018 were higher net interest margin (+14 basis points), increase in fee and other income (+ 5 basis points), and a decline in provision for loan and lease losses (-2 basis points). Factors that reduced profitability were a 5 basis point increase in operating expenses and 1 basis point decrease in non-operating income.

The median ROAA was up 19 basis points from a year ago to 57 basis points at the end of 2018.

FICUs saw an increase in net worth in 2018.

Due to higher earnings, FICU net worth increased by 8.8 percent for 2018 to $164.3 billion. FICUs saw an 18.59 percent in secondary capital during 2018 to almost $265 million. Credit unions with a low-income designation can issue secondary capital. As of December 2018. 2,554 credit unions had a low-income designation.

The industry's net worth ratio increased from 10.95 percent at the end of 2017 to 11.30 percent as of December 31, 2018.

As of December 2018, 98.59 percent of FICUs have a net worth ratio of at least 7 percent, the minimum requirement to be well-capitalized. On the other hand, 3 credit unions had a net worth ratio below 2 percent.

FICUs reported an increase in assets, loans, shares, and members during 2018.

Year-over-year,

Outstanding indirect loans grew by 14.1 percent during 2018 to $222 billion. Approximately 21 percent of all loans were indirect loans.

Because loan growth outpaced the growth in shares and deposits, the loan-to-share ratio rose from 82.6 percent at the end of 2017 to 85.6 percent at the end of 2018.

To help finance the growth in loans, FICUs reduced their investments and holdings of cash and cash equivalents in 2018. As a result, cash plus short-term investments as a percentage of assets fell from 12.43 percent in 2017 to 11.36 percent in 2018.

FICUs saw a decline in delinquent loans during 2018.

Delinquent loans fell from $7.78 billion at the end of 2017 to $7.42 percent at the end of 2018. The delinquency rate was 71 basis points at the end of 2018 compared to 81 basis points from a year earlier.

However, net charge-offs increased by 5.9 percent during 2018 to $5.76 billion at the end of 2018. The net charge-off rate fell by 2 basis points during 2018 to 0.58 percent.

FICUs reported a 5.1 percent increase in allowance for loan and lease losses during 2018 to $9.26 billion. Due to the decline in delinquent loans and the increase in allowance for loan and lease losses, the industry's coverage ratio rose from 113.25 percent in 2017 to 124.73 percent in 2018.

Read NCUA's Quarterly Credit Union Data Summary.

Read NCUA's Financial Trends Report.

For 2018, interest income rose by 13.8 percent and nonineterest income was up 9.3 percent. Interest expense jumped by 29.4 percent in 2018, while nonineterest expenses advanced by 8.8 percent.

Only 631 FICUs reported a loss for 2018.

FICUs reported a return on average assets (ROAA) of 92 basis points for 2018. In comparison, ROAA for 2017 was 78 basis points.

Factors helping to drive the improved profitability of FICUs during 2018 were higher net interest margin (+14 basis points), increase in fee and other income (+ 5 basis points), and a decline in provision for loan and lease losses (-2 basis points). Factors that reduced profitability were a 5 basis point increase in operating expenses and 1 basis point decrease in non-operating income.

The median ROAA was up 19 basis points from a year ago to 57 basis points at the end of 2018.

FICUs saw an increase in net worth in 2018.

Due to higher earnings, FICU net worth increased by 8.8 percent for 2018 to $164.3 billion. FICUs saw an 18.59 percent in secondary capital during 2018 to almost $265 million. Credit unions with a low-income designation can issue secondary capital. As of December 2018. 2,554 credit unions had a low-income designation.

The industry's net worth ratio increased from 10.95 percent at the end of 2017 to 11.30 percent as of December 31, 2018.

As of December 2018, 98.59 percent of FICUs have a net worth ratio of at least 7 percent, the minimum requirement to be well-capitalized. On the other hand, 3 credit unions had a net worth ratio below 2 percent.

FICUs reported an increase in assets, loans, shares, and members during 2018.

Year-over-year,

- Assets increased by 5.4 percent to $1.45 trillion.

- Loans grew by 9 percent to over $1 trillion.

- Deposits and shares increased by 5.2 percent to $1.22 trillion.

- Membership grew by 4.4 percent to 116.2 million members.

Outstanding indirect loans grew by 14.1 percent during 2018 to $222 billion. Approximately 21 percent of all loans were indirect loans.

Because loan growth outpaced the growth in shares and deposits, the loan-to-share ratio rose from 82.6 percent at the end of 2017 to 85.6 percent at the end of 2018.

To help finance the growth in loans, FICUs reduced their investments and holdings of cash and cash equivalents in 2018. As a result, cash plus short-term investments as a percentage of assets fell from 12.43 percent in 2017 to 11.36 percent in 2018.

FICUs saw a decline in delinquent loans during 2018.

Delinquent loans fell from $7.78 billion at the end of 2017 to $7.42 percent at the end of 2018. The delinquency rate was 71 basis points at the end of 2018 compared to 81 basis points from a year earlier.

However, net charge-offs increased by 5.9 percent during 2018 to $5.76 billion at the end of 2018. The net charge-off rate fell by 2 basis points during 2018 to 0.58 percent.

FICUs reported a 5.1 percent increase in allowance for loan and lease losses during 2018 to $9.26 billion. Due to the decline in delinquent loans and the increase in allowance for loan and lease losses, the industry's coverage ratio rose from 113.25 percent in 2017 to 124.73 percent in 2018.

Read NCUA's Quarterly Credit Union Data Summary.

Read NCUA's Financial Trends Report.

Auto Finance by Lender Type

The following chart looks at auto lending by lender type.

The chart includes information on outstanding auto loans and the share of auto loans that are subprime by lender type. The chart appeared in the Federal Reserve Bank of New York's Liberty Street Economics.

Banks followed by credit unions had the largest amount of outstanding auto loans. Credit unions had the lowest share of subprime loans.

To read more of the Liberty Street Economics piece, click here.

The chart includes information on outstanding auto loans and the share of auto loans that are subprime by lender type. The chart appeared in the Federal Reserve Bank of New York's Liberty Street Economics.

Banks followed by credit unions had the largest amount of outstanding auto loans. Credit unions had the lowest share of subprime loans.

To read more of the Liberty Street Economics piece, click here.

Monday, March 4, 2019

Navy FCU Faces Class Action Lawsuit over NSF Practices

Navy Federal Credit Union (Vienna) is facing a class action lawsuit over its non sufficient fund (NSF) practices.

The lawsuit alleges that the credit union's NSF practices are predatory and deceptive.

The plaintiff claims that Navy Federal Credit Union’s fee schedule and account documents are counter-intuitive and deceptive.

In addition, the lawsuit states that Navy FCU charges multiple NSF fees on the same transaction.

The lawsuit alleges that Navy FCU purposefully reprocesses a transaction even though the credit union knew the account did not have sufficient funds to cover the transaction, so as to increase NSF revenues.

The lawsuit was filed January 28, 2019 in the U.S. District Court for the Eastern District of Virginia.

The lawsuit alleges that the credit union's NSF practices are predatory and deceptive.

The plaintiff claims that Navy Federal Credit Union’s fee schedule and account documents are counter-intuitive and deceptive.

In addition, the lawsuit states that Navy FCU charges multiple NSF fees on the same transaction.

The lawsuit alleges that Navy FCU purposefully reprocesses a transaction even though the credit union knew the account did not have sufficient funds to cover the transaction, so as to increase NSF revenues.

The lawsuit was filed January 28, 2019 in the U.S. District Court for the Eastern District of Virginia.

Saturday, March 2, 2019

Maine Savings FCU Buys Naming Rights to Performance Venue

Maine Savings Federal Credit Union (Hampden, ME) bought the naming rights to a performance venue in Westbrook.

The venue is expected to open this summer and has a seating capacity of 8,200.

The venue will be called Maine Savings Pavilion.

The terms of the deal was not disclosed.

Read the story.

The venue is expected to open this summer and has a seating capacity of 8,200.

The venue will be called Maine Savings Pavilion.

The terms of the deal was not disclosed.

Read the story.

Friday, March 1, 2019

Credit Union Tax Subsidy Going to the Wealthy

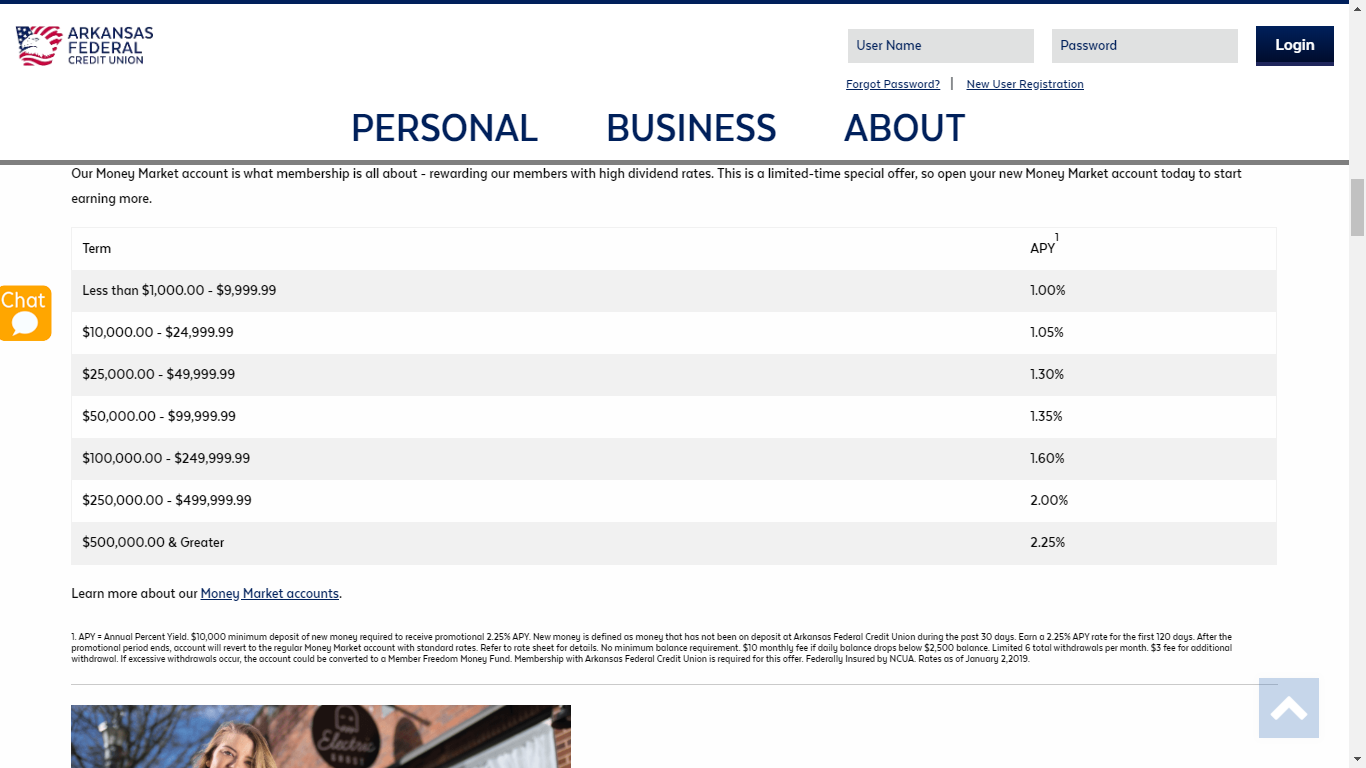

Arkansas Federal Credit Union (Jacksonville, AR) is rewarding large balance money market accounts (MMAs) with higher interest rates than accounts with lower balances.

The following table appeared in Arkansas FCU's January 2019 newsletter (click on image to enlarge). The credit union is paying an Annual Percent Yield (APY) of 2.25 percent on MMAs with balances of at least $500,000, while it pays an APY of 1 percent on accounts with balances between $1,000 and $9,999.99.

Part of this higher APY is to compensate depositors for risk with balances exceeding the insured deposit limit. But it also indicates that Arkansas FCU is targeting its tax subsidy at higher net worth individuals.

The following table appeared in Arkansas FCU's January 2019 newsletter (click on image to enlarge). The credit union is paying an Annual Percent Yield (APY) of 2.25 percent on MMAs with balances of at least $500,000, while it pays an APY of 1 percent on accounts with balances between $1,000 and $9,999.99.

Part of this higher APY is to compensate depositors for risk with balances exceeding the insured deposit limit. But it also indicates that Arkansas FCU is targeting its tax subsidy at higher net worth individuals.