The Salt Lake Tribune is reporting that the Coalition of Religious Communities, a social justice advocacy group, has charged eight Utah-based credit unions of offering predatory payday loan-type products to members and wants the credit unions to stop offering these products.

The group cites that the annual interest rates on these short-term loans range from the equivalent of 254 percent to 312 percent.

“This is not what I expect from my credit union,” Linda Hilton, a coalition spokeswoman, said, who noted that she is a member of America First Credit Union. (emphasis added)

The eight Utah credit unions offering these loans are Alliance, America First, Cyprus, Family First, Heritage West (which failed on December 31, 2009), Mountain America, Southwest and USU Charter.

But I do have a comment to Ms. Hilton -- if you do not like the behavior of America First, move your money.

Wednesday, June 30, 2010

Tuesday, June 29, 2010

Mediterranean CU Cruise

Thanks to a column by Stuart Perlitsh, CEO of Glendale Area Schools FCU, I was informed about a credit union education junket.

CU Conferences is hosting a 10-day Mediterranean Odyssey Credit Union Educational Cruise Conference aboard the Holland America ship ms Noordam from August 2, 2010 to August 12, 2010.

The educational cruise includes stops in Barcelona, Monte Carlo, Malta, Tunis, Florence, Naples, and Rome.

The cost per participant ranges from $2995 for an Inside Stateroom to $4695 for Deluxe Verandah Oceanview. Spouse or guest rate runs from $995 to $1495. These rates do not include taxes and fees of $377.40 per person.

Some within the credit union industry are questioning the wisdom of having such a cruise. Stuart Perlitsh wrote:

"Did Congress envision the savings credit unions realize from our federal tax-exempt status would be spent cavorting around the midnight buffet on Mediterranean cruises? Facing certain unknown NCUA assessments, is now the time to cruise the Mediterranean? The future of the credit union industry faces real threats; is now the time to cruise the Mediterranean?"

Saturday, June 26, 2010

Arrowhead CU Placed into Conservatorship

The National Credit Union Administration (NCUA) placed Arrowhead Central Credit Union of San Bernardino, California, into conservatorship.

Arrowhead Central Credit Union was placed into conservatorship due to declining financial condition. The Los Angeles Times (blog) reported that the NCUA had been unable to find a partner for Arrowhead.

The $876 million credit union was significantly undercapitalized as of March 2010.

Approximately $20.1 million in loans were 60 days or more past due and another $18.4 million in loans were between 30 days and 60 days past due. Arrowhead also reported holding $5.4 million in foreclosed or repossessed assets. However, its allowances for loan and lease losses were $49.5 million.

In recent months, Arrowhead Central has sold off its insurance agency and also sold branches for $7 million to Alaska USA FCU in an effort to stabilize its financial condition.

Executives were put on paid administrative leave and the credit union's board of directors and supervisory committee were dismissed.

The Federal Credit Union Act authorizes the NCUA Board to appoint itself conservator when necessary to conserve the assets of a federally insured credit union, protect members’ interests or protect the National Credit Union Share Insurance Fund.

Arrowhead Central Credit Union was placed into conservatorship due to declining financial condition. The Los Angeles Times (blog) reported that the NCUA had been unable to find a partner for Arrowhead.

The $876 million credit union was significantly undercapitalized as of March 2010.

Approximately $20.1 million in loans were 60 days or more past due and another $18.4 million in loans were between 30 days and 60 days past due. Arrowhead also reported holding $5.4 million in foreclosed or repossessed assets. However, its allowances for loan and lease losses were $49.5 million.

In recent months, Arrowhead Central has sold off its insurance agency and also sold branches for $7 million to Alaska USA FCU in an effort to stabilize its financial condition.

Executives were put on paid administrative leave and the credit union's board of directors and supervisory committee were dismissed.

The Federal Credit Union Act authorizes the NCUA Board to appoint itself conservator when necessary to conserve the assets of a federally insured credit union, protect members’ interests or protect the National Credit Union Share Insurance Fund.

Thursday, June 24, 2010

More on Air Force FCU

Earlier this year, I reported on NCUA slapping Air Force FCU with a letter of understanding and agreement for improperly adding individuals to the credit union’s membership rolls who were not in its field of membership.

In May, NCUA announced that it approved a change in Air Force FCU's field of membership going from a multiple common bond credit union to a single common bond credit union serving all military personnel in the states of Texas, Oklahoma, Mississippi, Louisiana and Arkansas. Credit Union Journal is reporting that the credit union will also serve civilian and federal government employees at military facilities in those 5 states.

I suspect that this field of membership change was done to limit the harm that may arise from a potential divestiture order from NCUA. If you caste the net wide enough, those previously illegally added members will now qualify as members under the new field of membership.

In May, NCUA announced that it approved a change in Air Force FCU's field of membership going from a multiple common bond credit union to a single common bond credit union serving all military personnel in the states of Texas, Oklahoma, Mississippi, Louisiana and Arkansas. Credit Union Journal is reporting that the credit union will also serve civilian and federal government employees at military facilities in those 5 states.

I suspect that this field of membership change was done to limit the harm that may arise from a potential divestiture order from NCUA. If you caste the net wide enough, those previously illegally added members will now qualify as members under the new field of membership.

Wednesday, June 23, 2010

House-Senate Conferees Extend TAG Program to CUs

In a previous post, I mentioned that NCUA had requested that credit unions should receive the same treatment as FDIC-insured banks with respect to a full guarantee of funds held in noninterest-bearing transaction accounts.

BNA is reporting that House-Senate conferees agreed to extend the FDIC’s Transaction Account Guarantee (TAG) program for two years beyond its current Dec. 31, 2010 expiration date. House conferees asked that this provision include federally-insured credit unions and the Senate agreed to the recommendation.

Unfortunately, I have not seen the legislative language.

BNA is reporting that House-Senate conferees agreed to extend the FDIC’s Transaction Account Guarantee (TAG) program for two years beyond its current Dec. 31, 2010 expiration date. House conferees asked that this provision include federally-insured credit unions and the Senate agreed to the recommendation.

Unfortunately, I have not seen the legislative language.

Monday, June 21, 2010

NCUA Request Parallel Insurance Treatment for Non-interest Bearing Transaction Accounts

In a June 17 letter to House Financial Services Committee Chairman Barney Frank (D – Mass.), NCUA Chairman Debbie Matz requested that federally-insured credit unions receive the same insurance treatment as FDIC-insured banks with regard to non-interest bearing transaction accounts.

As the House-Senate Conference Committee deliberate on the Wall Street Reform and Consumer Protection Act, House conferees recommended adding a new provision to the bill making permanent the FDIC’s Transaction Account Guarantee (TAG) program. The Senate conferees countered with extending the coverage for two years.

As background, the TAG program was created in October 2008, as part of FDIC's Temporary Liquidity Guarantee Program (TLGP) to address systemic risk. Under TAG, the FDIC guaranteed all funds held at participating insured depository institutions (beyond the standard maximum deposit insurance limit) in qualifying noninterest-bearing transaction accounts. The TAG program was initially scheduled to expire on December 31, 2009 and was subsequently extended to June 30, 2010. FDIC Board is meeting Tuesday, June 22 on whether to extend the TAG program for another 6 months.

NCUA Chairman Matz wrote Chairman Frank requesting parallel treatment noting that it is a “long-standing congressional practice ensuring that the policies of the NCUSIF are generally consistent with those of the FDIC.” (Below is the text of the letter and the proposed legislative language -- click on images to enlarge).

I would feel a lot more comfortable about the proposed legislative language if the amended Section 207(k)(1)(A)(iii)(I), which defines a non-interest bearing transaction account, included the word dividend along with interest and read as follows "with respect to which interest or dividend is neither accrued or paid." My concern is that a NCUA lawyer would make the determination that Federal credit unions pay dividends, not interest, and thus any transaction account paying dividends would receive a full guarantee from the NCUSIF.

As the House-Senate Conference Committee deliberate on the Wall Street Reform and Consumer Protection Act, House conferees recommended adding a new provision to the bill making permanent the FDIC’s Transaction Account Guarantee (TAG) program. The Senate conferees countered with extending the coverage for two years.

As background, the TAG program was created in October 2008, as part of FDIC's Temporary Liquidity Guarantee Program (TLGP) to address systemic risk. Under TAG, the FDIC guaranteed all funds held at participating insured depository institutions (beyond the standard maximum deposit insurance limit) in qualifying noninterest-bearing transaction accounts. The TAG program was initially scheduled to expire on December 31, 2009 and was subsequently extended to June 30, 2010. FDIC Board is meeting Tuesday, June 22 on whether to extend the TAG program for another 6 months.

NCUA Chairman Matz wrote Chairman Frank requesting parallel treatment noting that it is a “long-standing congressional practice ensuring that the policies of the NCUSIF are generally consistent with those of the FDIC.” (Below is the text of the letter and the proposed legislative language -- click on images to enlarge).

I would feel a lot more comfortable about the proposed legislative language if the amended Section 207(k)(1)(A)(iii)(I), which defines a non-interest bearing transaction account, included the word dividend along with interest and read as follows "with respect to which interest or dividend is neither accrued or paid." My concern is that a NCUA lawyer would make the determination that Federal credit unions pay dividends, not interest, and thus any transaction account paying dividends would receive a full guarantee from the NCUSIF.

Friday, June 18, 2010

Credit Unions to Pay $1 Billion Assessment for Corporate Credit Union Rescue

The National Credit Union Administration (NCUA) announced yesterday at its June 17th Board meeting federally-insured credit unions will be charged 13.4 basis points assessment to repay borrowed funds from the U.S. Treasury to stabilize the corporate credit union system. This assessment will raise approximately $1 billion and is based upon March 31, 2010 insured shares (deposits). All federally-insured credit unions will be invoiced in July with payment due in August.

In announcing the assessment, NCUA Chairman Debbie Matz said: “The decision to levy this assessment was not taken lightly. We considered numerous factors – including the liquidity needs of the Stabilization Fund, the additional pressure on natural-person credit union earnings, and the future consequences of foregoing the corporate assessment this year.”

NCUA estimates that this assessment will reduce the credit union industry’s ROA by 11 basis points and will lower the net worth ratio by not more than 13 basis points. Staff analysis notes that 552 credit unions that reported positive income as of March 2010 would experience negative core income for the year due to the Corporate CU Stabilization Fund assessment. Sixty three federally-insured credit unions would slip below being well capitalized (net worth ratio of at least 7 percent). An additional 27 credit unions would become undercapitalized and 2 credit unions would become critically undercapitalized as their net worth ratios fall below 2 percent.

An interesting fact raised in the Board Action memorandum that had not been previously disclosed was that the NCUA Board in May authorized the Corporate CU Stabilization Fund to borrow up to $2 billion. The borrowed funds will be placed into the corporate credit union system to enhance liquidity during the summer when share deposit levels at corporate credit unions are traditionally lower. Since the end of May, actual borrowings are $810 million, bringing the total outstanding borrowings of the Corporate CU Stabilization Fund to $1.5 billion.

In announcing the assessment, NCUA Chairman Debbie Matz said: “The decision to levy this assessment was not taken lightly. We considered numerous factors – including the liquidity needs of the Stabilization Fund, the additional pressure on natural-person credit union earnings, and the future consequences of foregoing the corporate assessment this year.”

NCUA estimates that this assessment will reduce the credit union industry’s ROA by 11 basis points and will lower the net worth ratio by not more than 13 basis points. Staff analysis notes that 552 credit unions that reported positive income as of March 2010 would experience negative core income for the year due to the Corporate CU Stabilization Fund assessment. Sixty three federally-insured credit unions would slip below being well capitalized (net worth ratio of at least 7 percent). An additional 27 credit unions would become undercapitalized and 2 credit unions would become critically undercapitalized as their net worth ratios fall below 2 percent.

An interesting fact raised in the Board Action memorandum that had not been previously disclosed was that the NCUA Board in May authorized the Corporate CU Stabilization Fund to borrow up to $2 billion. The borrowed funds will be placed into the corporate credit union system to enhance liquidity during the summer when share deposit levels at corporate credit unions are traditionally lower. Since the end of May, actual borrowings are $810 million, bringing the total outstanding borrowings of the Corporate CU Stabilization Fund to $1.5 billion.

Thursday, June 17, 2010

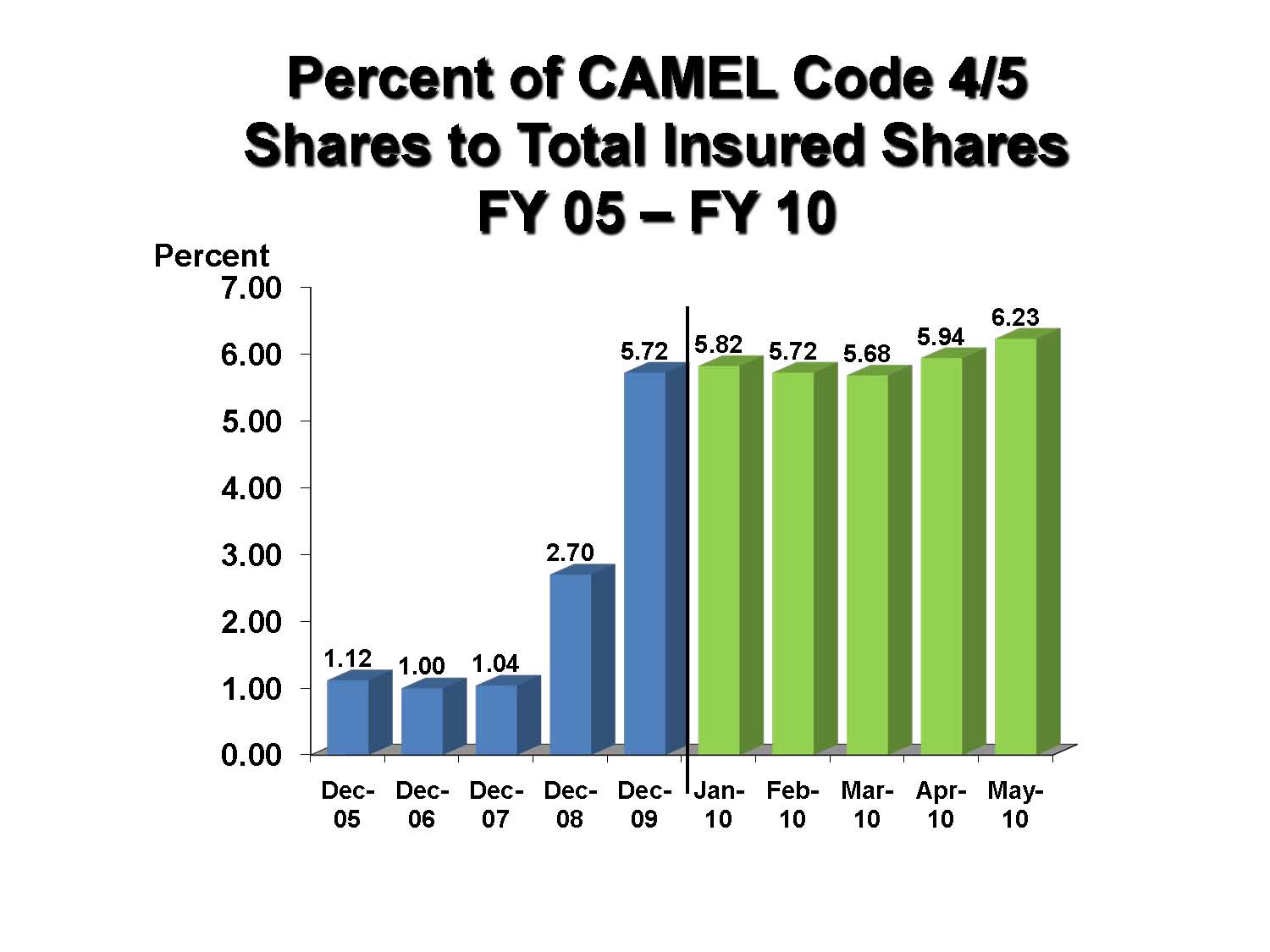

NCUA: Assets and Shares in Problem CUs Up in May

NCUA reported today that the number of problem credit unions fell in May by 6 to 351 credit unions. However, the percentage of insured shares (deposits) in problem credit unions rose by 29 basis points in April to 6.23 percent.

NCUA defines a problem credit union as a credit union with a CAMEL 4 or 5 rating.

NCUA reported that problem credit unions held $45.3 billion in shares (deposits) and assets of $51.6 billion -- an increase of $2.4 billion in May.

In its monthly NCUSIF report, NCUA noted that 15 credit unions with $1 billion or more in assets are on its problem list and hold $23.4 billion in shares. There is an additional 65 credit unions with between $100 million and $1 billion in assets on the problem list holding $17.6 billion in shares.

NCUA defines a problem credit union as a credit union with a CAMEL 4 or 5 rating.

NCUA reported that problem credit unions held $45.3 billion in shares (deposits) and assets of $51.6 billion -- an increase of $2.4 billion in May.

In its monthly NCUSIF report, NCUA noted that 15 credit unions with $1 billion or more in assets are on its problem list and hold $23.4 billion in shares. There is an additional 65 credit unions with between $100 million and $1 billion in assets on the problem list holding $17.6 billion in shares.

Tuesday, June 15, 2010

ABA's Comment on NCUA's Short-term, Small Amount Loan Proposal

The following is what ABA wrote to NCUA on its proposed short-term, small amount loan program.

Dear Ms. Rupp:

The National Credit Union Administration (NCUA) Board is proposing to amend its general lending rule to enable federal credit unions (FCUs) to offer short-term, small amount loans (STS loans) as a viable alternative to payday loans. The proposed amendment would permit FCUs to charge a higher interest rate for an STS loan than is permitted under the general lending rule, but the proposal will impose limitations on the permissible term, amount, and fees associated with an STS loan.

ABA believes this proposed rule points FCUs back toward their basic charter purpose, which many FCUs have largely abandoned. NCUA reported that only 532 FCUs offered micro consumer loans and only 279 FCUs (or 5.9 percent of all FCUs) offered payday loans at the end of 2009. Congress in 1934 created FCUs for the purpose of making “credit for provident and productive purposes more available to people of small means.” The intent of Congress when establishing FCUs was for FCUs to be an alternative to nontraditional financial services providers, such as payday lenders, for people of small means.

NCUA needs to have realistic expectations regarding its STS loan program. Banks that have participated in FDIC’s Small-Dollar Loan Pilot Program Guidelines have found such loans to be in general unprofitable. According to the FDIC, very few banks after the first year in its pilot program have achieved, or expect to achieve, short-term profitability from the small dollar loan program. Instead the program is viewed by some banks as a way to build a long-term relationship, while others viewed it as a vehicle to build community goodwill. Additionally, the delinquency rate for the small dollar loan program was typically higher than that for other consumer loans, at 7.3 percent of loans outstanding, and the charge-off rate was 3.4 percent of loans originated under the pilot. ABA recommends that the NCUA Board conduct consumer research to determine which features of the product are important to potential payday borrowers and survey FCUs that are currently offering payday loans to determine their experience with respect to STS loans.

In conclusion, ABA believes that NCUA’s proposed STS loan program would point FCUs back toward their basic charter purpose of serving people of small means. The Board should conduct consumer research to ensure that its sets realistic expectations regarding this STS Loan program.

Sincerely,

Keith Leggett

Vice President & Senior Economist

Dear Ms. Rupp:

The National Credit Union Administration (NCUA) Board is proposing to amend its general lending rule to enable federal credit unions (FCUs) to offer short-term, small amount loans (STS loans) as a viable alternative to payday loans. The proposed amendment would permit FCUs to charge a higher interest rate for an STS loan than is permitted under the general lending rule, but the proposal will impose limitations on the permissible term, amount, and fees associated with an STS loan.

ABA believes this proposed rule points FCUs back toward their basic charter purpose, which many FCUs have largely abandoned. NCUA reported that only 532 FCUs offered micro consumer loans and only 279 FCUs (or 5.9 percent of all FCUs) offered payday loans at the end of 2009. Congress in 1934 created FCUs for the purpose of making “credit for provident and productive purposes more available to people of small means.” The intent of Congress when establishing FCUs was for FCUs to be an alternative to nontraditional financial services providers, such as payday lenders, for people of small means.

NCUA needs to have realistic expectations regarding its STS loan program. Banks that have participated in FDIC’s Small-Dollar Loan Pilot Program Guidelines have found such loans to be in general unprofitable. According to the FDIC, very few banks after the first year in its pilot program have achieved, or expect to achieve, short-term profitability from the small dollar loan program. Instead the program is viewed by some banks as a way to build a long-term relationship, while others viewed it as a vehicle to build community goodwill. Additionally, the delinquency rate for the small dollar loan program was typically higher than that for other consumer loans, at 7.3 percent of loans outstanding, and the charge-off rate was 3.4 percent of loans originated under the pilot. ABA recommends that the NCUA Board conduct consumer research to determine which features of the product are important to potential payday borrowers and survey FCUs that are currently offering payday loans to determine their experience with respect to STS loans.

In conclusion, ABA believes that NCUA’s proposed STS loan program would point FCUs back toward their basic charter purpose of serving people of small means. The Board should conduct consumer research to ensure that its sets realistic expectations regarding this STS Loan program.

Sincerely,

Keith Leggett

Vice President & Senior Economist

Friday, June 11, 2010

Sperry Associates FCU Under Enforcement Action

The National Credit Union Administration (NCUA) has published a Letter of Understanding and Agreement (LUA) entered into with Sperry Associates Federal Credit Union, Garden City Park, New York on May 28, 2010. The LUA outlines corrective steps the credit union needs to take with regard to strategic risk, credit risk, interest rate risk, liquidity risk, transactions risk, and compliance risk.

Below are some of the actions required by the LUA.

The credit union was to charge-off $3.1 million in non-performing assets associated with CalState 9 loan participation pool and South Florida Properties participation loan. This resulted in the credit union becoming undercapitalized as of March 31, 2010.

The credit union will submit a net worth restoration plan. As part of its net worth restoration plan, the credit union must achieve a return on average assets of zero percent, .15 percent, and .25 percent by year-end 2010, 2011, and 2012, respectively. The credit union's return on average assets was -1.68 percent at the end of 2009.

The credit union will cease entering into loan participation agreements until such time it demonstates to NCUA that it has a satisfactory due diligence process. As of March 2010, slightly more than 11 percent of its outstanding loans were loan participations.

The credit union is holding 3 private label collaterialized mortgage obligations (CMOs) that have been downgraded below regulatory acceptable levels. NCUA is requiring the credit union to contract with a qualified third party to complete a portfolio analysis of the CMOs and will recognize any other than temporary impairment losses. At the end of the first, the credit union had $41.5 million in CMOs.

The credit union will also stop granting loan modifications until the board develops a loan modification policy and puts in place managerial procedures that meet NCUA's satisfaction. The credit union reported $1.5 million in modified loans at the end of the first quarter.

The credit union will perform a test of its disaster recovery/business continuity program and will contract with a third party to evaluate the security of its information security and technology program.

Below are some of the actions required by the LUA.

The credit union was to charge-off $3.1 million in non-performing assets associated with CalState 9 loan participation pool and South Florida Properties participation loan. This resulted in the credit union becoming undercapitalized as of March 31, 2010.

The credit union will submit a net worth restoration plan. As part of its net worth restoration plan, the credit union must achieve a return on average assets of zero percent, .15 percent, and .25 percent by year-end 2010, 2011, and 2012, respectively. The credit union's return on average assets was -1.68 percent at the end of 2009.

The credit union will cease entering into loan participation agreements until such time it demonstates to NCUA that it has a satisfactory due diligence process. As of March 2010, slightly more than 11 percent of its outstanding loans were loan participations.

The credit union is holding 3 private label collaterialized mortgage obligations (CMOs) that have been downgraded below regulatory acceptable levels. NCUA is requiring the credit union to contract with a qualified third party to complete a portfolio analysis of the CMOs and will recognize any other than temporary impairment losses. At the end of the first, the credit union had $41.5 million in CMOs.

The credit union will also stop granting loan modifications until the board develops a loan modification policy and puts in place managerial procedures that meet NCUA's satisfaction. The credit union reported $1.5 million in modified loans at the end of the first quarter.

The credit union will perform a test of its disaster recovery/business continuity program and will contract with a third party to evaluate the security of its information security and technology program.

Royal CU's Purchase of Deposits and Assets from Anchor Bank Receives Regulatory Approval

The National Credit Union Administration (NCUA) announced today that it has approved the Purchase and Assumption of certain assets, including eleven branch offices in Wisconsin, and deposits by Royal Credit Union from Anchor Bank. The Wisconsin Office of Credit Unions, Federal Deposit Insurance Corporation, and Office of Thrift Supervision have all approved the transaction. This transaction will result in approximately 20,000 Anchor Bank customers becoming members of Royal Credit Union.

Thursday, June 10, 2010

Royal CU Awaits NCUA Approval on Bank Branch Sale

Royal Credit Union (Eau Claire, WI) in November 2009 entered into an agreement to purchase 11 branches from AnchorBank along with deposits and loans. Here are the links to AnchorBanCorp Wisconsin's 8K filing and Press Release.

Royal Credit Union will assume approximately $177 million in deposits and receive a corresponding amount in loans, real estate and other assets. The branches involved in the transaction are located in the Northwestern Wisconsin communities of Amery, Balsam Lake, Centuria, Menomonie, Milltown, New Richmond, Osceola, River Falls, St. Croix Falls, Somerset and Star Prairie. The depositors at these branches will become members of Royal Credit Union when the transaction is completed.

This deal is still awaiting regulatory approval from NCUA.

In my opinion, this transaction is a no brainer and should be approved by NCUA. But I also believe that such transactions should be a two way street.

It would be hypocritical for the credit union industry or its regulator to permit a credit union to buy a bank or bank branches along with the deposits and loans; but to restrict the ability of banks to do the same.

I know that some within the credit union industry will argue that a bank buying a credit union or credit union branches is not the same as a credit union buying a bank or bank branches, because there is a need to protect the interest of the credit union members. But as I wrote in a January 22, 2010 post,

Maybe the regulatory hold up in approving this transaction is that NCUA fears that it is opening Pandora's Box.

But what's good for the goose is good for the gander.

Royal Credit Union will assume approximately $177 million in deposits and receive a corresponding amount in loans, real estate and other assets. The branches involved in the transaction are located in the Northwestern Wisconsin communities of Amery, Balsam Lake, Centuria, Menomonie, Milltown, New Richmond, Osceola, River Falls, St. Croix Falls, Somerset and Star Prairie. The depositors at these branches will become members of Royal Credit Union when the transaction is completed.

This deal is still awaiting regulatory approval from NCUA.

In my opinion, this transaction is a no brainer and should be approved by NCUA. But I also believe that such transactions should be a two way street.

It would be hypocritical for the credit union industry or its regulator to permit a credit union to buy a bank or bank branches along with the deposits and loans; but to restrict the ability of banks to do the same.

I know that some within the credit union industry will argue that a bank buying a credit union or credit union branches is not the same as a credit union buying a bank or bank branches, because there is a need to protect the interest of the credit union members. But as I wrote in a January 22, 2010 post,

There are ample protections for members, and members are more than capable of determining what is best for them financially.

Maybe the regulatory hold up in approving this transaction is that NCUA fears that it is opening Pandora's Box.

But what's good for the goose is good for the gander.

Wednesday, June 9, 2010

The 90 Million Myth

What is the true number of credit union members in the United States?

NCUA reported that federally-insured credit unions had 90 million members. This number is arrived at by aggregating the total number of members of each credit union.

However, this number appears to be an overestimate.

The Credit Union Journal on January 24, 2008 reported that Jerry Marsh, a credit union consultant, said the actual number of credit union members is closer to 30 million, because “the so-called memberships that credit unions count represent duplicates, people who have memberships in two or three or more credit unions.”

Jerry Marsh’s estimate may be at the lower end of the range; but could accurately reflect the number of individuals that identify a credit union as their primary financial institution.

Using data from a 2004 Filene Study, Who Uses Credit Unions?, that found that 36 percent of households use credit unions – 8 percent of households only use a credit union, 12 percent primarily use a credit union, and 16 percent use a credit union, but their primary relationship is with a bank – then this would equate to about 42 million households using a credit union.

I suspect that the average number of household members using a credit union is below 2, maybe something between 1.25 and 1.5 household members. But this is strictly a guess, as I have not seen such a statistic.

This would suggest that the true number of credit union members is more likely in the range between 50 million and 60 million, not the 90 million reported by NCUA.

NCUA reported that federally-insured credit unions had 90 million members. This number is arrived at by aggregating the total number of members of each credit union.

However, this number appears to be an overestimate.

The Credit Union Journal on January 24, 2008 reported that Jerry Marsh, a credit union consultant, said the actual number of credit union members is closer to 30 million, because “the so-called memberships that credit unions count represent duplicates, people who have memberships in two or three or more credit unions.”

Jerry Marsh’s estimate may be at the lower end of the range; but could accurately reflect the number of individuals that identify a credit union as their primary financial institution.

Using data from a 2004 Filene Study, Who Uses Credit Unions?, that found that 36 percent of households use credit unions – 8 percent of households only use a credit union, 12 percent primarily use a credit union, and 16 percent use a credit union, but their primary relationship is with a bank – then this would equate to about 42 million households using a credit union.

I suspect that the average number of household members using a credit union is below 2, maybe something between 1.25 and 1.5 household members. But this is strictly a guess, as I have not seen such a statistic.

This would suggest that the true number of credit union members is more likely in the range between 50 million and 60 million, not the 90 million reported by NCUA.

Monday, June 7, 2010

Silver State Schools Charging $5 Monthly Maintenance Fee

I was tipped off by a reader that financially-troubled Silver State Schools CU on May 10th started to charge a $5 per month maintainance fee on regular checking accounts.

The credit union advertises on its website that the fee can be avoided if:

You are 60 years of age or older;

You are younger than 18 years of age;

You maintain a minimum balance of $5,000 in your checking account at all times; or

You have aggregate deposit and loan balances totaling $20,000 or more.

You can also avoid the fee if you convert your checking account into an e-checking account. However, you would incur a monthly maintenance fee if you were write a paper check; perform certain checking functions in-branch or via the credit union's Call Center including inquiries, deposits, withdrawals, and cashing services; or revert to getting paper statements.

I was told that many members of Silver State Schools did not receive proper notice about the change and incurred the fee, as they either did not receive the mailing (or recall getting the mailing) or did not see the notice on the credit union's website about the fee.

After incurring the fee, this person stated that a branch manager refused to refund the fee and told this person: "You are under the assumption that credit unions are different than banks."(emphasis added)

The credit union advertises on its website that the fee can be avoided if:

You are 60 years of age or older;

You are younger than 18 years of age;

You maintain a minimum balance of $5,000 in your checking account at all times; or

You have aggregate deposit and loan balances totaling $20,000 or more.

You can also avoid the fee if you convert your checking account into an e-checking account. However, you would incur a monthly maintenance fee if you were write a paper check; perform certain checking functions in-branch or via the credit union's Call Center including inquiries, deposits, withdrawals, and cashing services; or revert to getting paper statements.

I was told that many members of Silver State Schools did not receive proper notice about the change and incurred the fee, as they either did not receive the mailing (or recall getting the mailing) or did not see the notice on the credit union's website about the fee.

After incurring the fee, this person stated that a branch manager refused to refund the fee and told this person: "You are under the assumption that credit unions are different than banks."(emphasis added)

Thursday, June 3, 2010

Q1 Financials: Shares and Assets Up, Loans Down

The National Credit Union Administration reported that credit union assets and shares (deposits) grew during the first quarter, while loans declined.

Commenting on credit union performance during the first quarter, NCUA Chairman Debbie Matz said: “Some of the short-term numbers are moving in the right direction. However, credit unions still have a long way to go before overcoming all of the residual issues from the economic downturn of the past two years.”

Shares Post Strong Growth, Loans Fell

Federally-insured credit unions reported assets increased at a rate of 1.5 percent during the quarter to $897.6 billion, while deposits grew by 2.7 percent to $773.2 billion. However, loans fell by 1.2 percent to almost $566 billion. As a result, credit unions’ loan-to-share ratio continues to recede, down to 73.16 percent as of March 31, 2010, from 76.06 percent at year-end 2009.

With the exception of 1st mortgages and other lines of credit, all other loan categories fell during the first quarter:

• Credit card loans were down 2.9 percent;

• Other unsecured credit contracted by 2.7 percent;

• New vehicle loans fell by 5.7 percent;

• Used vehicle loans declined by 0.3 percent;

• Other real estate loans slipped by 1.8 percent; and

• Lease receivables by 5.4 percent.

Additionally, faltering loan demand caused cash, cash equivalents and investments at credit unions to increase during the first quarter. At the end of the first quarter, credit unions reported $297.7 billion up from 278.3 billion at the end of 2009.

Credit Unions Post $1.1 Billion Profit

The credit union industry reported a profit of $1.1 billion in the first quarter, with a return on average assets ratio of 0.48 percent. In comparison, federally-insured credit unions earned slightly less than $1.6 billion for all of 2009 and reported a return on average assets of 0.18 percent.

Net interest income was up 21.9 percent from a year ago to $5.4 billion, as interest expense at credit unions fell more rapidly than interest income. Non-interest income was up 15 percent from a year ago to $2.67 billion, while non-interest expenses grew at a slower pace of 2.8 percent.

Net Worth Ratio Slipped 3 Basis Points

Credit unions continue to build capital during the first quarter. Total equity at credit unions increased 1.5 percent to almost $88 billion. However, the net worth ratio for credit unions edged lower to 3 basis points during the quarter to 9.87 percent as of March 31, 2010.

Delinquency and Charge-Off Rates Edged Lower

During the first quarter of 2010, delinquent loans (loans 60 days or more past due) fell by 5 percent to $9.94 billion; however, delinquent loans were still 20.6 percent above what was reported for a comparable period last year. The percentage of loans that were delinquent fell by 7 basis points to 1.76 percent.

Net charge-offs were almost $1.69 billion, as of the end of the first quarter of 2010 – up almost 8.2 percent from year ago levels. However, the net charge-off rate slipped by 2 basis points during the quarter from 1.21 percent of average loans to 1.19 percent.

Credit unions reported almost $8.5 billion in modified outstanding loans, of which nearly $6.8 billion were real estate loans and $1.6 billion were consumer loans. Modified business loans were $1.3 billion, of which an overwhelming majority was real estate loans. As of the end of the first quarter, 22.32 percent of all modified real estate loans were two months or more past due with modified commercial real estate loans reporting a higher delinquency rate of 29.49 percent.

Credit unions set aside $1.85 billion for loan losses during the first quarter. This was 12 percent below the provisioning for loan losses from a comparable period a year earlier. During the first quarter, credit unions reported that allowances for loan and lease losses increased by approximately $180 million to almost $9 billion.

Foreclosed and repossessed assets increased by 37.5 percent over the last year to $1.6 billion at the end of March 2010.

Commenting on credit union performance during the first quarter, NCUA Chairman Debbie Matz said: “Some of the short-term numbers are moving in the right direction. However, credit unions still have a long way to go before overcoming all of the residual issues from the economic downturn of the past two years.”

Shares Post Strong Growth, Loans Fell

Federally-insured credit unions reported assets increased at a rate of 1.5 percent during the quarter to $897.6 billion, while deposits grew by 2.7 percent to $773.2 billion. However, loans fell by 1.2 percent to almost $566 billion. As a result, credit unions’ loan-to-share ratio continues to recede, down to 73.16 percent as of March 31, 2010, from 76.06 percent at year-end 2009.

With the exception of 1st mortgages and other lines of credit, all other loan categories fell during the first quarter:

• Credit card loans were down 2.9 percent;

• Other unsecured credit contracted by 2.7 percent;

• New vehicle loans fell by 5.7 percent;

• Used vehicle loans declined by 0.3 percent;

• Other real estate loans slipped by 1.8 percent; and

• Lease receivables by 5.4 percent.

Additionally, faltering loan demand caused cash, cash equivalents and investments at credit unions to increase during the first quarter. At the end of the first quarter, credit unions reported $297.7 billion up from 278.3 billion at the end of 2009.

Credit Unions Post $1.1 Billion Profit

The credit union industry reported a profit of $1.1 billion in the first quarter, with a return on average assets ratio of 0.48 percent. In comparison, federally-insured credit unions earned slightly less than $1.6 billion for all of 2009 and reported a return on average assets of 0.18 percent.

Net interest income was up 21.9 percent from a year ago to $5.4 billion, as interest expense at credit unions fell more rapidly than interest income. Non-interest income was up 15 percent from a year ago to $2.67 billion, while non-interest expenses grew at a slower pace of 2.8 percent.

Net Worth Ratio Slipped 3 Basis Points

Credit unions continue to build capital during the first quarter. Total equity at credit unions increased 1.5 percent to almost $88 billion. However, the net worth ratio for credit unions edged lower to 3 basis points during the quarter to 9.87 percent as of March 31, 2010.

Delinquency and Charge-Off Rates Edged Lower

During the first quarter of 2010, delinquent loans (loans 60 days or more past due) fell by 5 percent to $9.94 billion; however, delinquent loans were still 20.6 percent above what was reported for a comparable period last year. The percentage of loans that were delinquent fell by 7 basis points to 1.76 percent.

Net charge-offs were almost $1.69 billion, as of the end of the first quarter of 2010 – up almost 8.2 percent from year ago levels. However, the net charge-off rate slipped by 2 basis points during the quarter from 1.21 percent of average loans to 1.19 percent.

Credit unions reported almost $8.5 billion in modified outstanding loans, of which nearly $6.8 billion were real estate loans and $1.6 billion were consumer loans. Modified business loans were $1.3 billion, of which an overwhelming majority was real estate loans. As of the end of the first quarter, 22.32 percent of all modified real estate loans were two months or more past due with modified commercial real estate loans reporting a higher delinquency rate of 29.49 percent.

Credit unions set aside $1.85 billion for loan losses during the first quarter. This was 12 percent below the provisioning for loan losses from a comparable period a year earlier. During the first quarter, credit unions reported that allowances for loan and lease losses increased by approximately $180 million to almost $9 billion.

Foreclosed and repossessed assets increased by 37.5 percent over the last year to $1.6 billion at the end of March 2010.

Wednesday, June 2, 2010

Another Mega-Merger Announced

Kinecta Federal Credit Union and NuVision Federal Credit Union announced that the Boards of each organization have signed a letter of intent to merge the two credit unions. Earlier this year, I reported that First Tech CU and Addison Avenue FCU had announced their intent to merge creating a $5 billion credit union.

The proposed merger would create a $4.7 billion credit union with 40 branches primarily throughout Los Angeles and Orange Counties in California.

This announcement should not come as a total surprise. Kinecta FCU was in the middle of a CEO search and had been hard hit by the recession reporting losses of $44.3 million in 2008 and $71.3 million in 2009. As of March 2010, Kinecta reported $136.2 million in delinquent loans, which equaled 58.25 percent of the credit union's net worth.

We should expect more of these mega-merger announcements in the coming months, as financially crippled credit unions seek merger partners. As of the end of April, NCUA is reporting that there were 14 credit unions with $1 billion or more in assets that were rated a CAMEL 4 or 5 and 16 billion-dollar plus credit unions with a CAMEL rating of 3.

The proposed merger would create a $4.7 billion credit union with 40 branches primarily throughout Los Angeles and Orange Counties in California.

This announcement should not come as a total surprise. Kinecta FCU was in the middle of a CEO search and had been hard hit by the recession reporting losses of $44.3 million in 2008 and $71.3 million in 2009. As of March 2010, Kinecta reported $136.2 million in delinquent loans, which equaled 58.25 percent of the credit union's net worth.

We should expect more of these mega-merger announcements in the coming months, as financially crippled credit unions seek merger partners. As of the end of April, NCUA is reporting that there were 14 credit unions with $1 billion or more in assets that were rated a CAMEL 4 or 5 and 16 billion-dollar plus credit unions with a CAMEL rating of 3.